Capital Markets Playbook | Q2 2022

2022 Q1 Summary

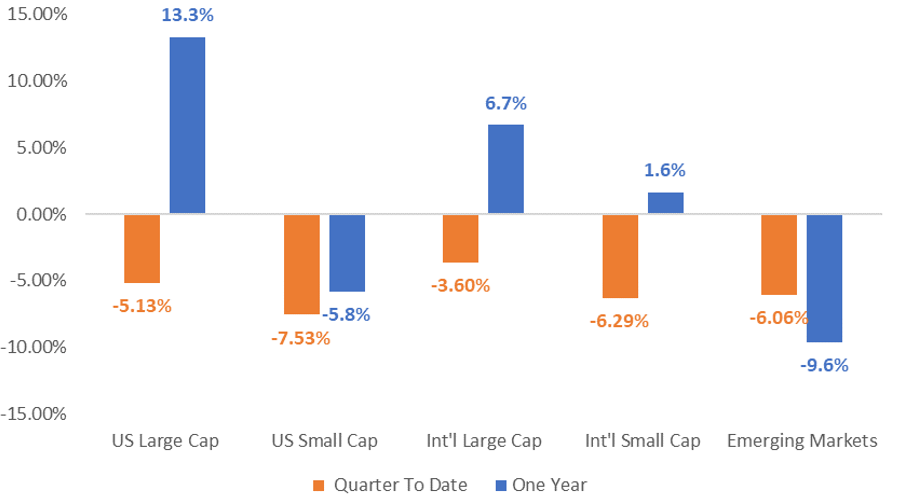

- Equities markets saw broad declines in the 1st quarter of 2022 as concerns over tighter monetary policy, inflation, and rising geopolitical risks sent markets solidly into negative territory to start the year.

- Growth-oriented, high-P/E stocks and small cap stocks underperformed in the quarter.

- Geopolitical uncertainty hit foreign markets early in the quarter, erasing what was modestly positive performance until that point.

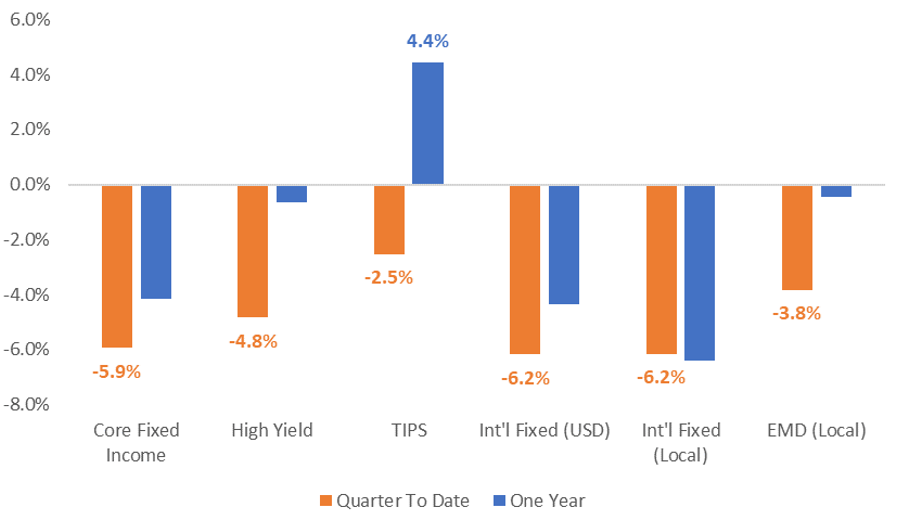

- Fixed Income markets registered some of the worst performance in years, with most major bond indices declining.

- Persistent high inflation and the Federal Reserve signaling it may raise interest rates faster than investors had previously expected sent yields higher during the quarter.

- Persistent high inflation and the Federal Reserve signaling it may raise interest rates faster than investors had previously expected sent yields higher during the quarter.

Equity Market Performance

Fixed Income Market Performance

Fixed Income Market Performance

Macroeconomic Outlook For the Next 6-12 Months

- Economic Growth:

- Economic activity in the US will decelerate in 2022.

- US economic growth in 2022 will not be as strong as it was in 2021.

- Although a recession remains unlikely in the short term, certain macroeconomic variables (tighter monetary policy, flat yield curve, etc) are beginning to signal that an economic contraction cannot be entirely ruled out.

- The global economic rebound will continue at an uneven pace.

- In the developed world (Europe and parts of Asia), economic growth is expected to moderate as well.

- Economic activity in the US will decelerate in 2022.

- Inflation:

- Expect inflation to moderate in 2022 but remain above the Fed’s 2% target through 2022.

- While many supply constraints continue to linger, there are signs of improvement in capacity utilization, labor participation, shipping rates, and other factors that have created headwinds since the pandemic began.

- Strong demand for certain goods and services over the summer months are likely to impact certain industries more than others (travel, hospitality, and entertainment are likely to see very strong excess demand over the spring and summer months of 2022).

- Interest Rates:

- The Federal Reserve may raise its short term policy rate a total of seven times in 2022. Markets have already priced in a 50bp rate hike, expected in May 2022. Interest rate hikes will slow, however, if the Fed becomes more concerned about an economic contraction.

- The Fed may also work to shrink the size of its balance sheet through its quantitative tightening program. In theory, this should put upward pressure on intermediate and long term yields. That said, the upward movement on yields could be offset by “flight to safety” behaviors if the threat of an economic contraction increases.

Market Outlook For the Next 6-12 Months

- Equities:

- Equity market volatility in the US is likely to be higher than normal as tighter monetary policy, inflation, COVID, and Russia/Ukraine continue to create uncertainty for investors.

- International and Emerging Market stocks are “cheap” relative to US stocks.

- That said, this segment of the equity market is subject to heightened levels of volatility over the short term due to the situation in Ukraine.

- Value stocks in the US remain cheap relative to growth stocks and may outperform as interest rates move higher.

- Growth stocks could, however, see increased demand if economic growth expectations decline.

- Fixed Income:

- The Fed’s monetary policy activities will create volatility in fixed income markets in 2022.

- High Yield fixed income is expensive on a historical perspective and may see selling pressure as the Fed’s monetary policy tightening program progresses.

- Higher quality corporate bonds and US Treasuries are the most attractive segment of the fixed income market as economic growth slows.

2022 Theme: The Pandemic Begins to Evolve Into An Endemic

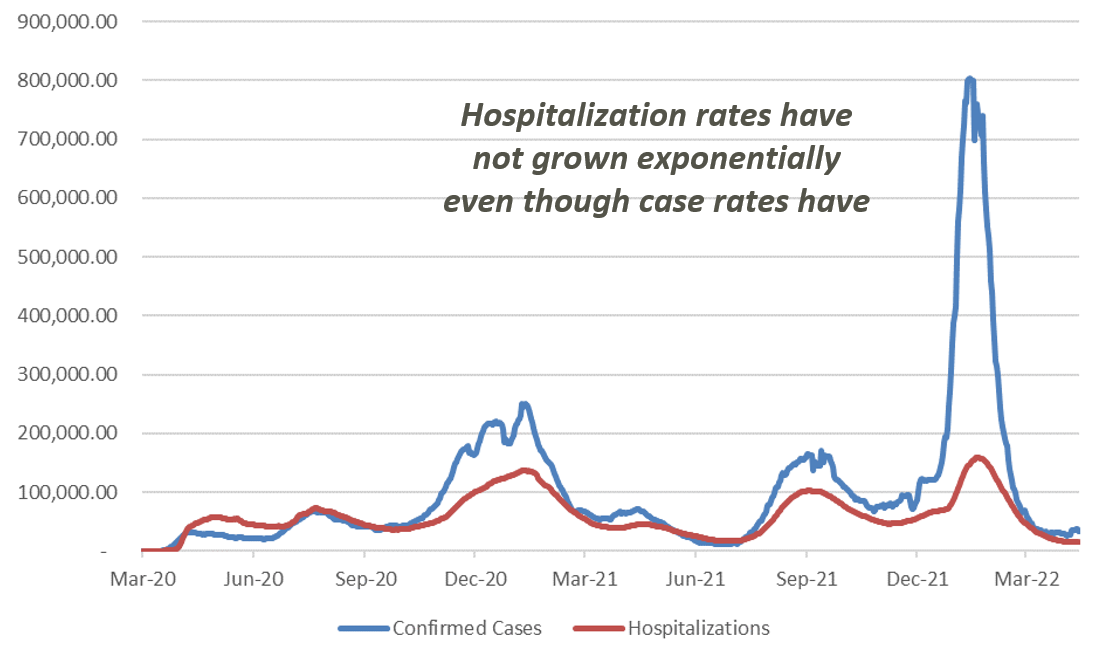

- Despite its explosive growth and quick transmissibility, the Omicron variant appears to be less dangerous than previous COVID variant surges.

- And while the health care system is currently struggling with capacity concerns, current data suggests the following:

- Vaccinations greatly reduce the potential for severe disease, hospitalizations, and death.

- Health care professionals have made tremendous progress with treatment procedures and have dramatically improved patient recovery times.

- New, less invasive vaccinations and therapies are likely to continue to hit the market in 2022.

- The combination of infections and vaccinations has the US population getting closer to “herd immunity”.

- Takeaways:

- The seriousness of the current or future COVID variants should never be discounted, but the pandemic may show signs of evolving into an endemic in 2022.

- The potential of “economic shutdowns” are lower than they have been since the beginning of the pandemic.

- Freedom of movement and activity will be greatly enhanced in 2022, which should support strong economic growth in 2022.

US COVID Confirmed Cases and Hospiralizations - 7 Day Average

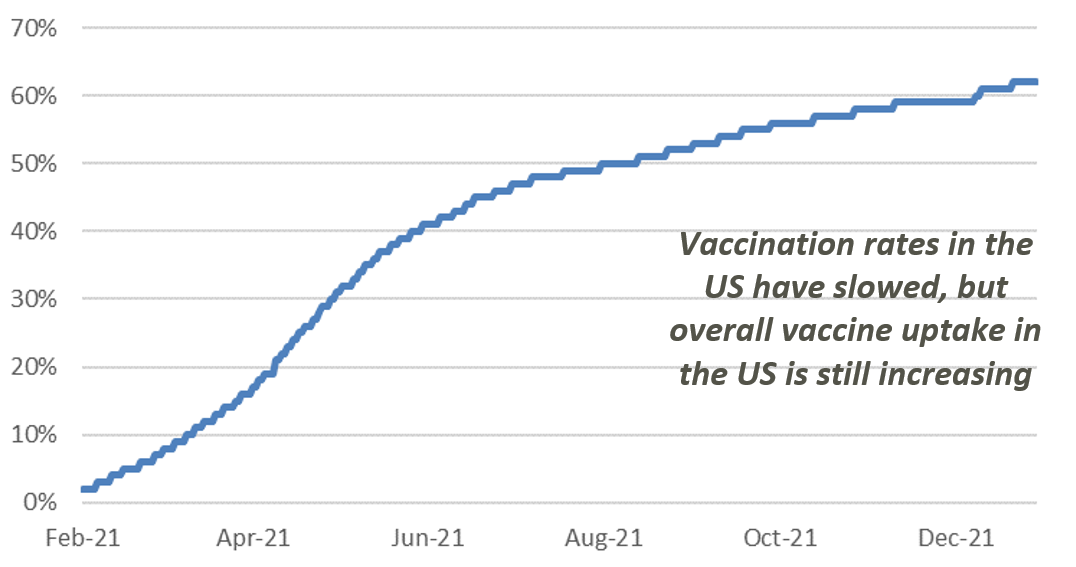

Percentage of US Population Fully Vaccinated

Percentage of US Population Fully Vaccinated

2022 Theme: Tighter Monetary Policy

- The Fed uses its monetary policies to achieve its dual mandate of:

- Full employment

- Price stability

- With inflation running high and unemployment close to pre-pandemic levels, the Fed has plenty of room to tighten monetary policy in 2022.

- Inflationary pressures are expected to moderate in 2022 and return to pre-pandemic levels in 2023.

- Unemployment may return to its pre-pandemic level in 2022.

- Takeaways:

- The Fed’s monetary policy tightening will help dampen inflation in 2022, but inflation will remain higher than normal in 2022.

- If the Fed increases the pace of its monetary policy in 2022, inflation may slow more than expected, but it may also result in higher unemployment.

- Forward looking expectations suggest that the base case is that the yield curve remains flat through 2023.

- Expected 2-10 year treasury yield spread in 2022: 0.5%

- Expected 2-10 year treasury yield spread in 2023: 0.3%

- Takeaways:

- Monetary policy expectations are subject to change as economic conditions evolve, which could lead to increased volatility in bond markets in the short term.

- Actively managed fixed income investments are most likely to outperform during periods of heightening rate volatility.

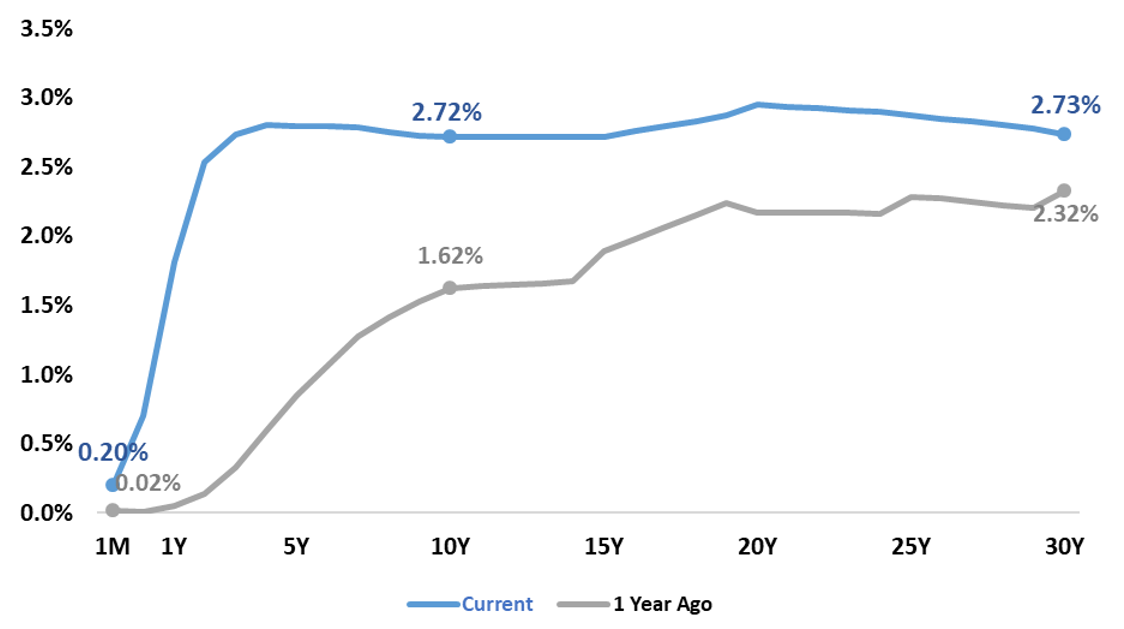

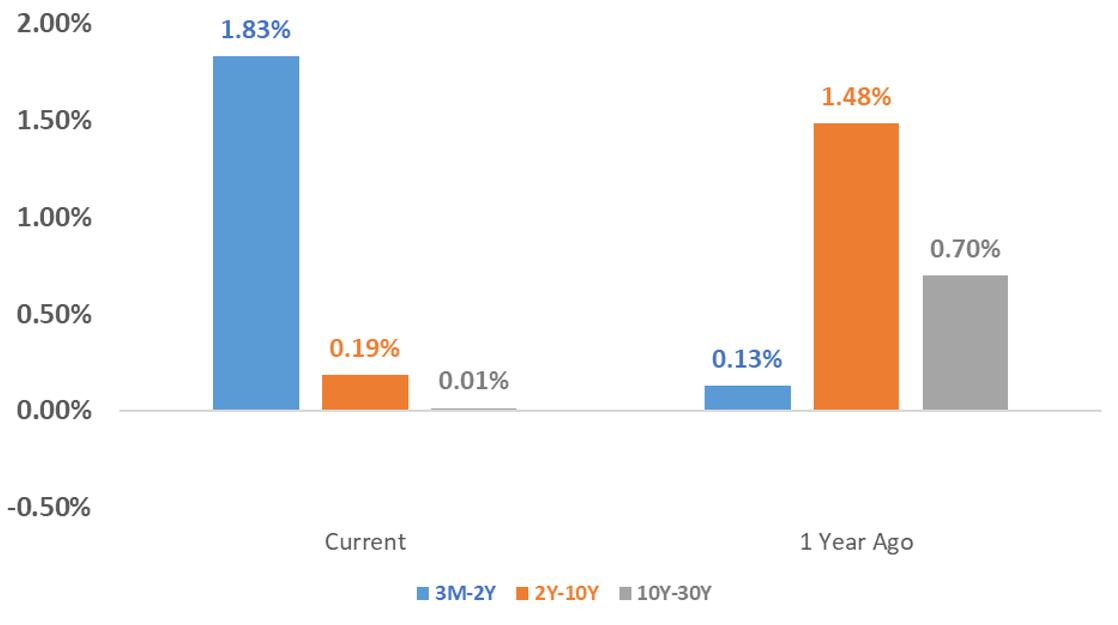

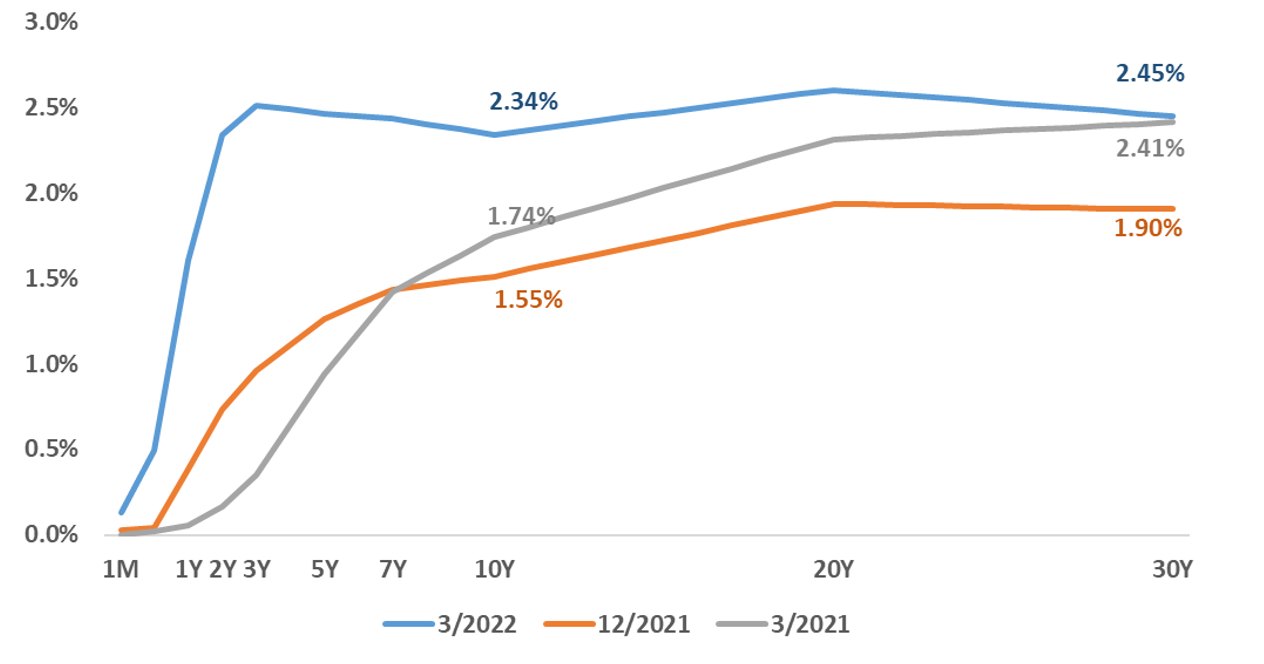

- The Fed’s plans to tighten monetary policy has pushed Treasury yields higher in the first three months of 2022.

- At the end of Q1, treasury yields were at their highest levels since the pandemic began.

- Monetary policy expectations have “flattened” the intermediate and long term portions of the yield curve.

- Ex: 10 year treasury yields were the same as 30 year treasury yields at the end of Q1.

- A flatter yield curve suggests that bond market participants expect lower growth and lower inflation in the future.

- The current yield curve suggests that the probability of an inversion is elevated.

- Yield curve inversion, the dynamic whereby long term yields are lower than short term yields, has historically preceded contractions in economic activity.

- Takeaway:

- If certain portions of the yield curve inverts, (ex: 2-10 year) for a sustained period of time, the likelihood of an economic recession increases.

US Treasury Yield Spreads

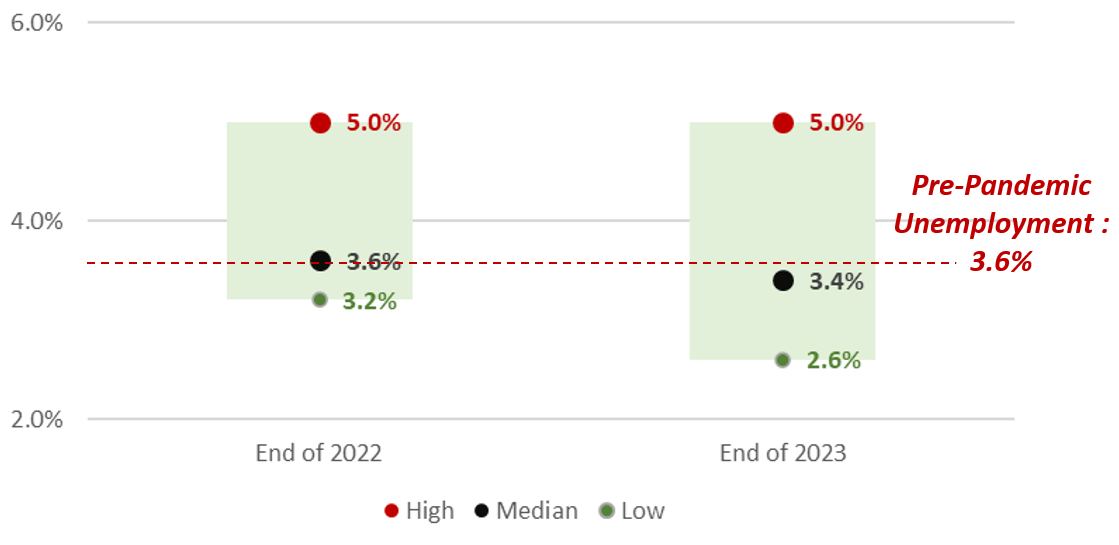

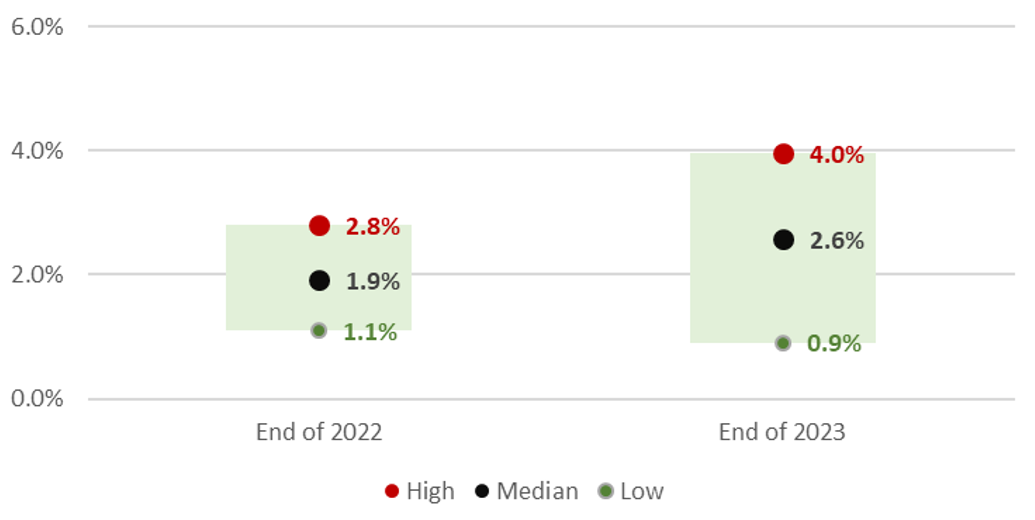

Projected Range of US Unemployment Outcomes

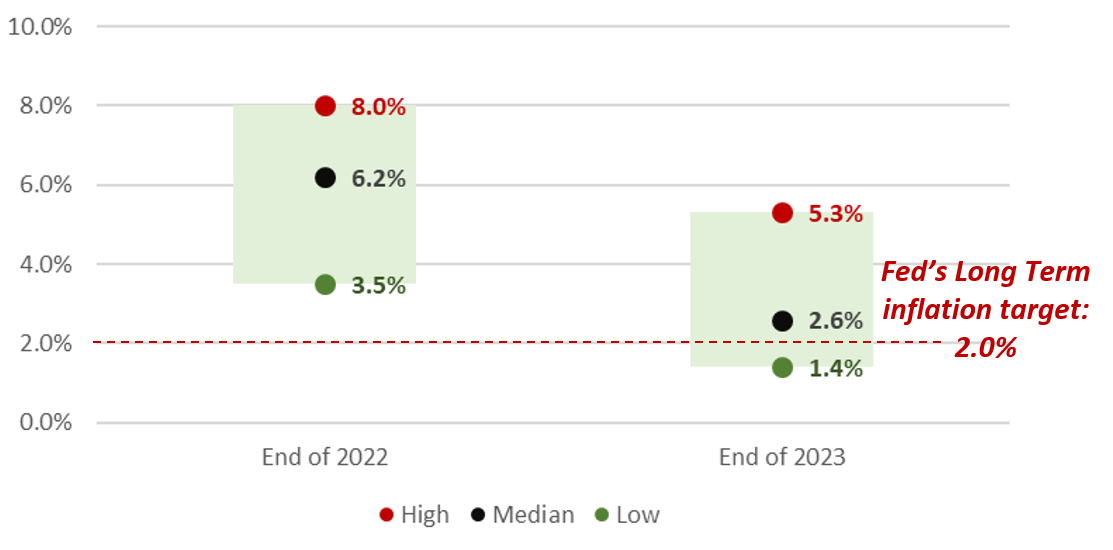

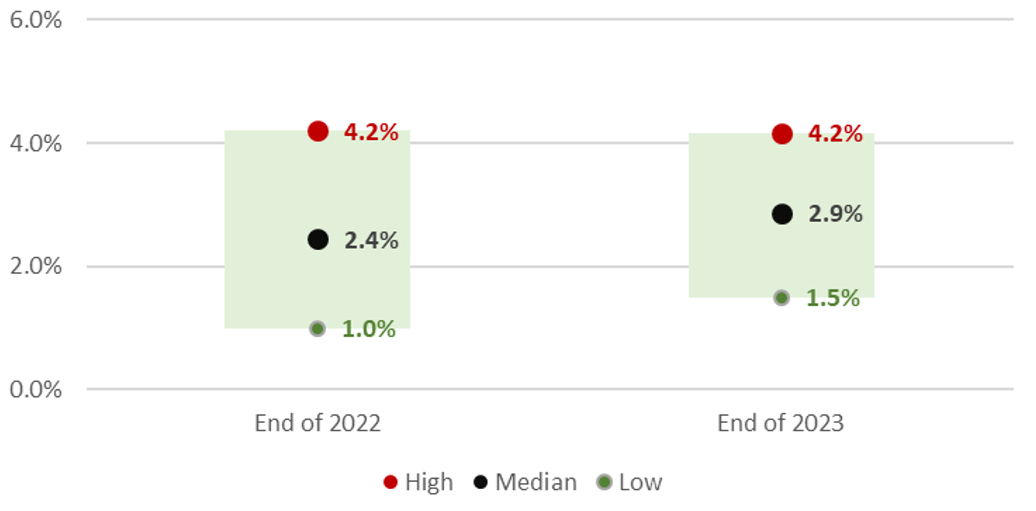

Projected Range of Inflation Outcomes

Projected Range of Inflation Outcomes

Projected Range of 2-Year US Treasury Yield Outcomes

Projected Range of 2-Year US Treasury Yield Outcomes

Projected Range of 10-Year US Treasury Yields

US Treasury Yields

US Treasury Yields

2022 Theme: Tighter Monetary Policy

2022 Theme: Decelerating, But Strong Economic Growth

- US economic growth projections have declined in recent weeks due to expectations for tighter monetary policy than previously anticipated.

- 2022 GDP estimates have declined about 0.5% since the Fed began to signal a more aggressive rate hike cycle that what the marketed had priced in.

- The risk of an economic contraction has increased in recent weeks but the likelihood of a 2022 recession in the US remains low.

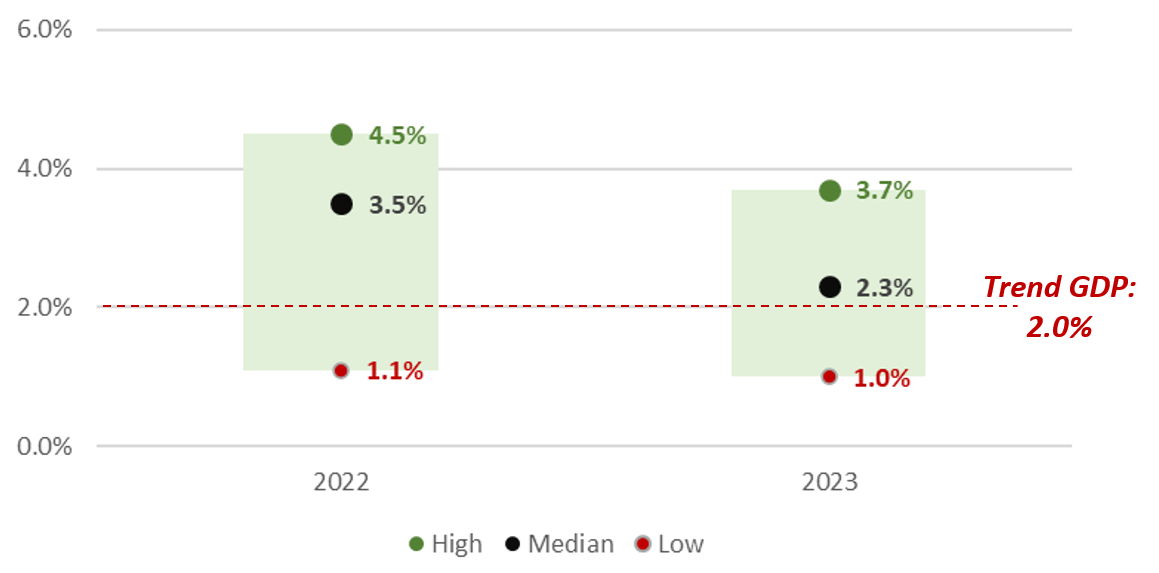

- Despite falling growth expectations, economic growth in the US is still expected to exceed trend GDP in 2022 and 2023.

- Takeaways:

- The prospects of higher interest rates will likely have a more meaningful impact of future economic growth in the US than any other macroeconomic variable.

- The faster the Fed dials back its accommodative monetary policy, the faster economic growth slows.

Projected Range of US Economic Growth

2022 Theme: Midterm Elections

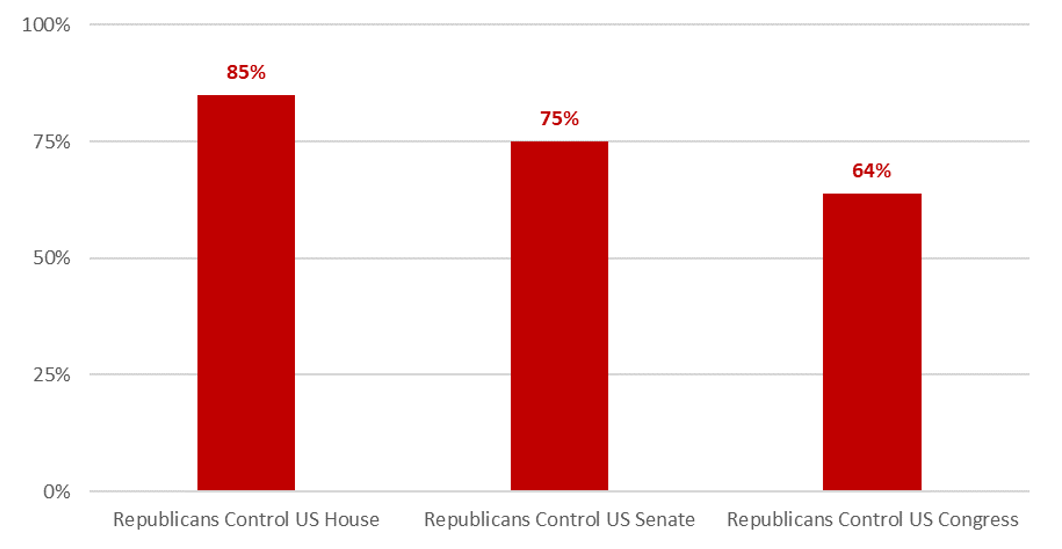

- Polling currently suggests that Republicans are likely to take back leadership in the US House and US Senate.

- Current polling should be considered as “noise” and investors should be ready for a long and contentious campaign season.

- Takeaways:

- Polling surprises will occur over the next several months and any market reaction to new polling trends is likely to be short term in nature.

- Investors should avoid making long term investment decisions based on changing political headlines.

Probability of Leadership Change Polling Data as of 3/31/2022

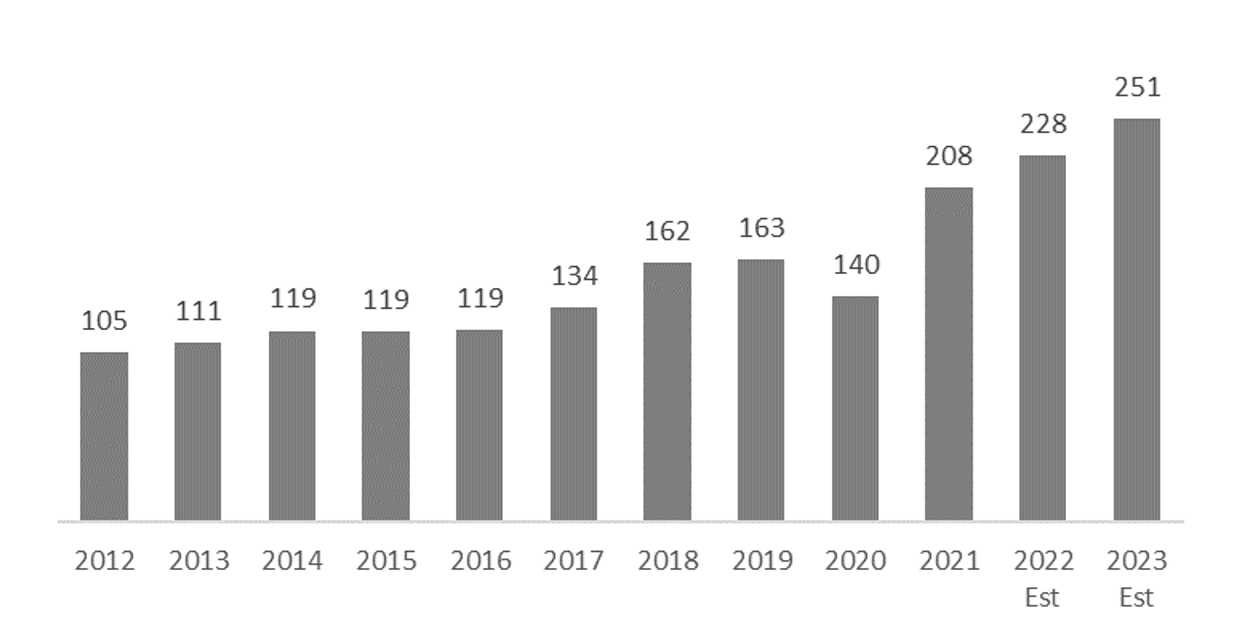

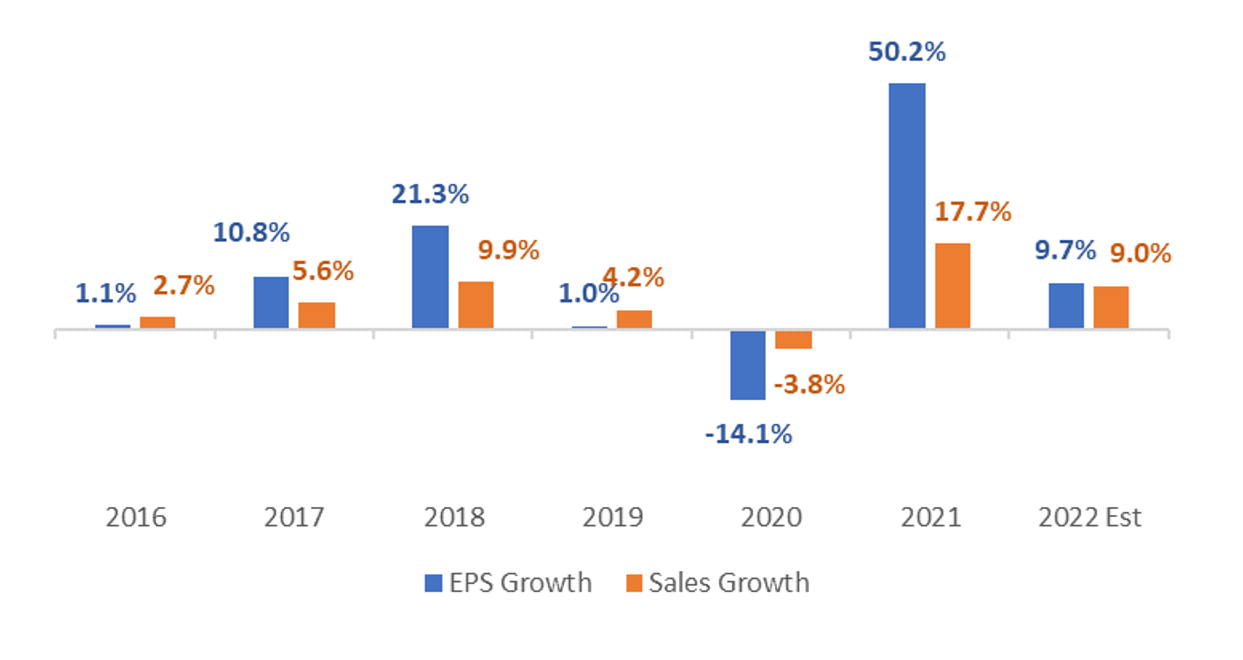

2022 Theme: Decelerating Growth in Corporate Earnings

- US corporate earnings growth in 2021 beat expectations by a very large margin as firms successfully navigated supply chain disruptions, labor shortages, and higher inflation.

- Current consensus estimates suggest that US corporate earnings growth will decelerate in 2022 but remain above the historical trend rate.

- Corporate earnings are expected to grow by close to 10% in 2022, about 40% higher than the historical average of 6%.

- Takeaways

- Persistent supply-chain disruptions and labor shortages could pressure companies bottom line in 2022, but investors should remember that firms successfully navigated these challenges in 2021.

- If the Fed’s monetary policy is more aggressive than currently expected, corporate earnings may come under additional pressure in 2022.

S&P 500 Bottom-Up EPS Actuals & Estimates

S&P 500 Earnings & Revenue Growth

2022 Playbook: US Equity

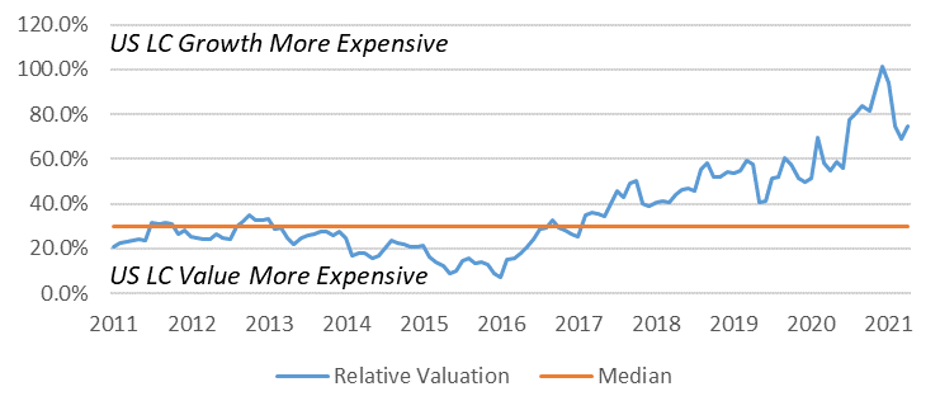

- Most valuation measures of U.S. stocks continue to look expensive.

- Most fundamental valuations indicate that US Large Cap equities are between 25%-50% more expensive than the historical average.

- “Growth” stocks in the US are significantly more expensive than “Value” stocks, despite their significant underperformance year to date.

- Historically, “Value” stocks have tended to outperform “Growth” stocks during periods of increasing interest rates.

- Takeaways:

- Strong corporate earnings expectations point to positive returns for US stocks in 2022, but high valuations will likely limit the potential upside.

- Investors can improve the risk and return profile of their investment portfolio by reducing any “overweight” to US “growth” stocks.

Relative Valuation

US Large Cap Growth vs. US Large Cap Value

Forward P/E

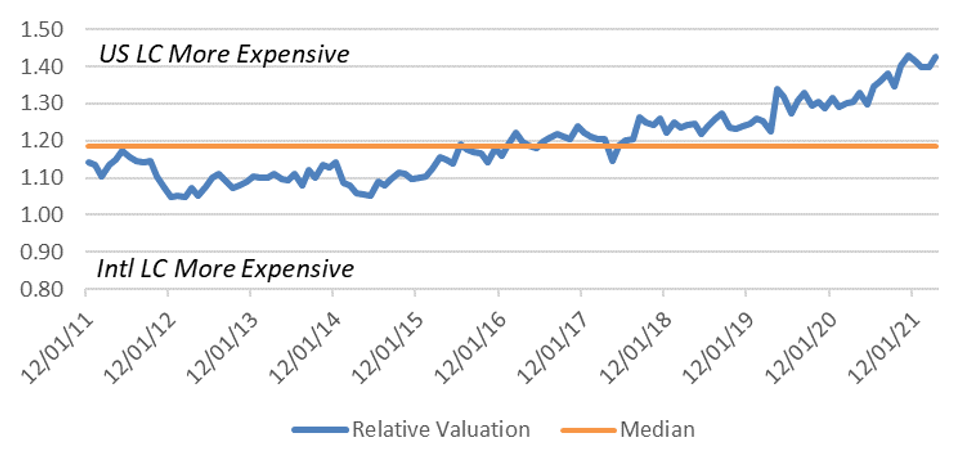

Relative Valuation

Relative Valuation

US Large Cap vs. International Large Cap

Forward P/E

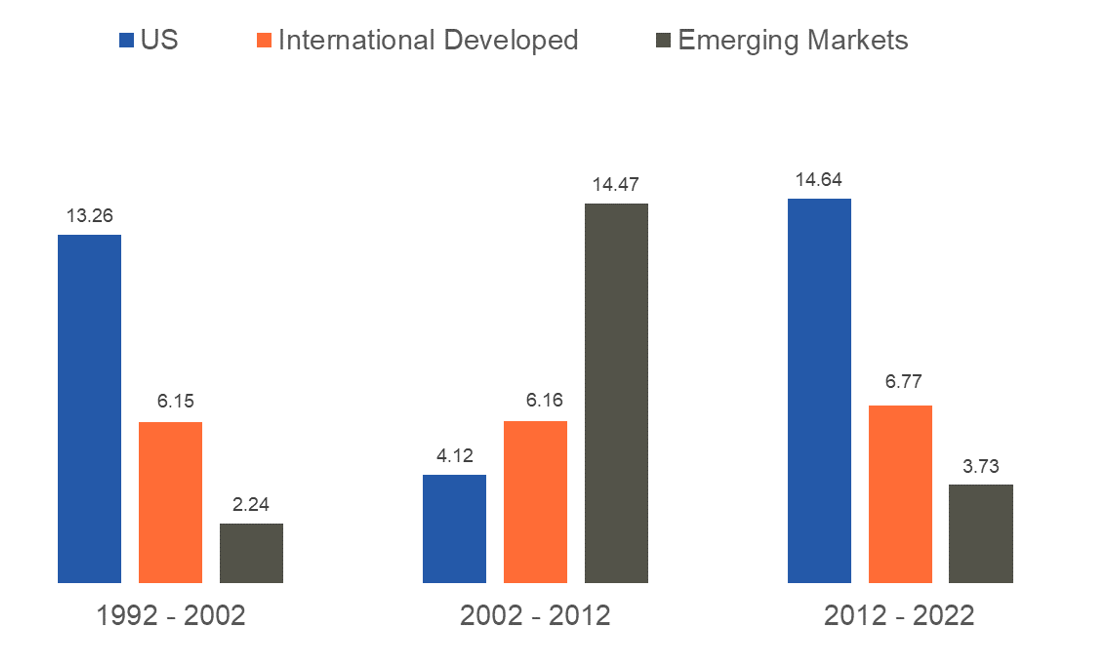

2022 Playbook: International Equity

- US investors have benefited from home-country overexposure in the past 10 years.

- Consistent outperformance of the US equity markets is not a natural state and will reverse at some point.

- Historical returns over longer time periods show that return differences between US and international markets are cyclical in nature (the current cycle of US outperformance is the longest ever recorded).

- International and emerging market equities are much cheaper than US equities and have a higher upside as a result.

- Additionally, International and Emerging Market equities have a larger weight of “Value” stocks than US markets.

- Takeaways:

- Investors that shy away from International and Emerging Market equities are likely reducing the upside potential of their investment portfolios.

World Equity Market Performance

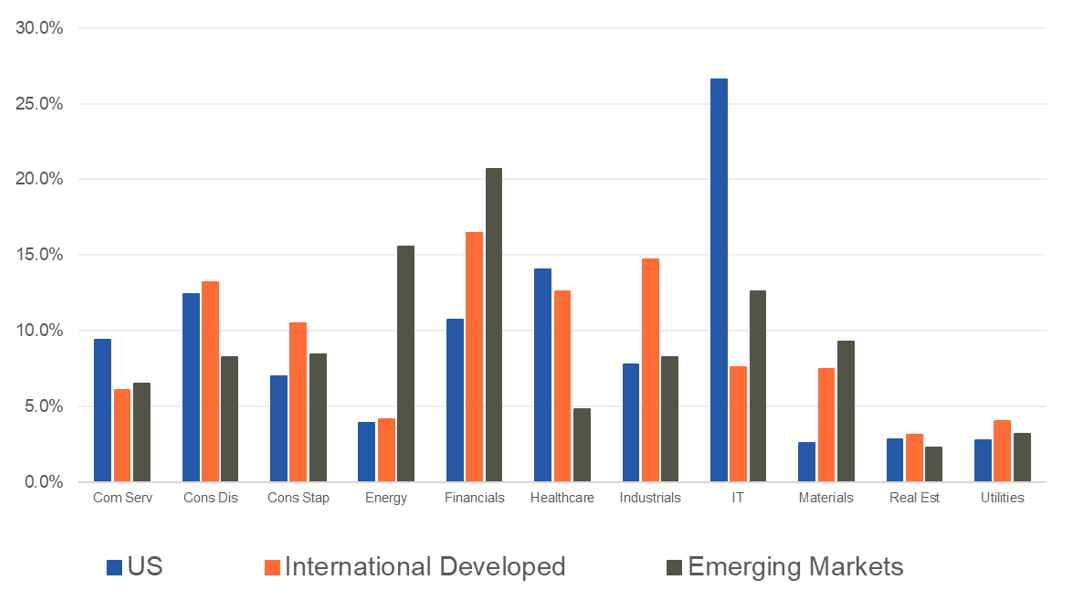

World Equity Sector Allocation

2022 Playbook: Fixed Income

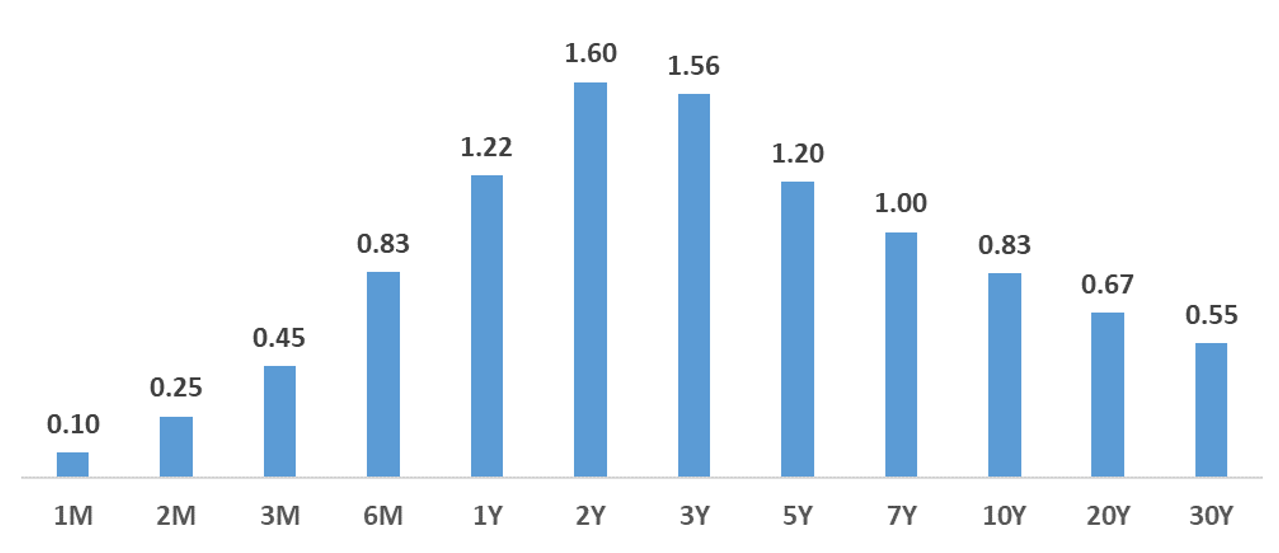

- Interest rates on the short end of the yield curve have exploded higher as a result of monetary policy expectations.

- Longer term yields have not increased to the same extent as short term yields, creating a flattening in the yield curve.

- Takeaways:

- A marginal increase in portfolio duration may be appropriate as a result of the recent move in short term rates

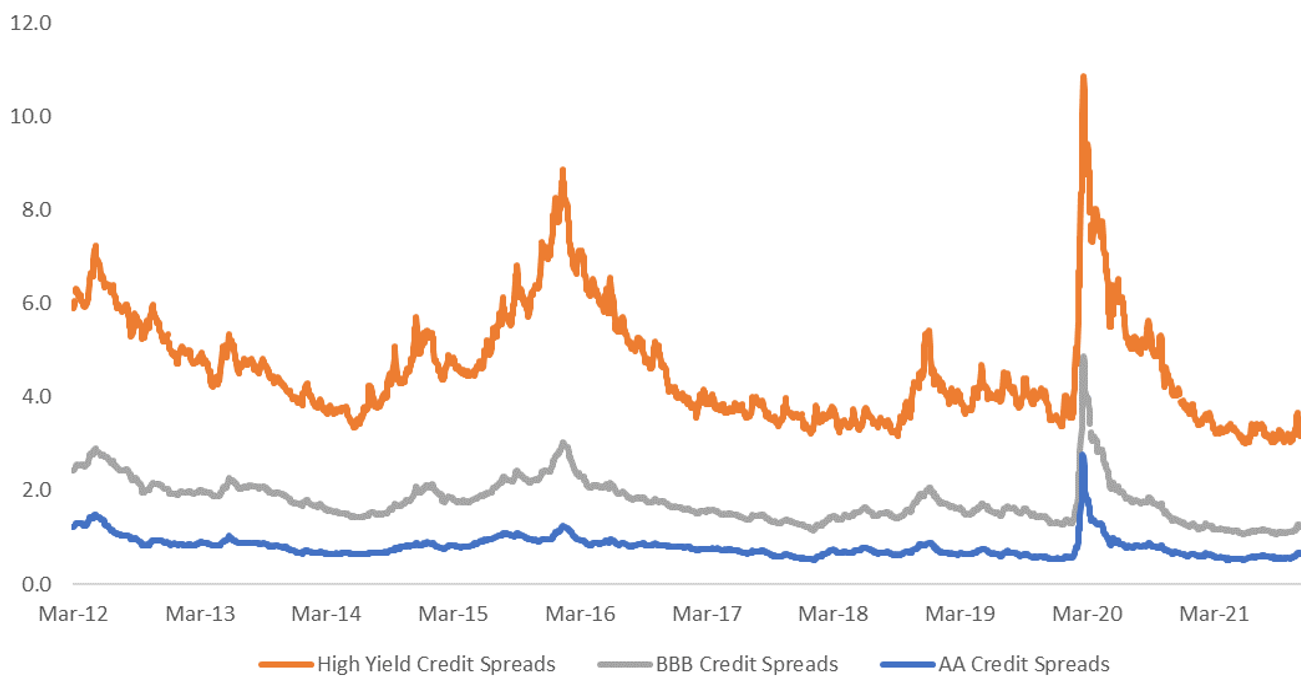

- Corporate credit is historically expensive from a fundamental perspective.

- Spreads have widened during the first quarter of 2022 but still remain low from a historical perspective.

- Corporate credit can face headwinds during periods of slower than expected economic growth.

- Takeaways:

- Repositioning the fixed income portfolio to include higher quality credit is prudent given the current economic outlook.

- Repositioning the fixed income portfolio to include higher quality credit is prudent given the current economic outlook.

US Treasury Yields

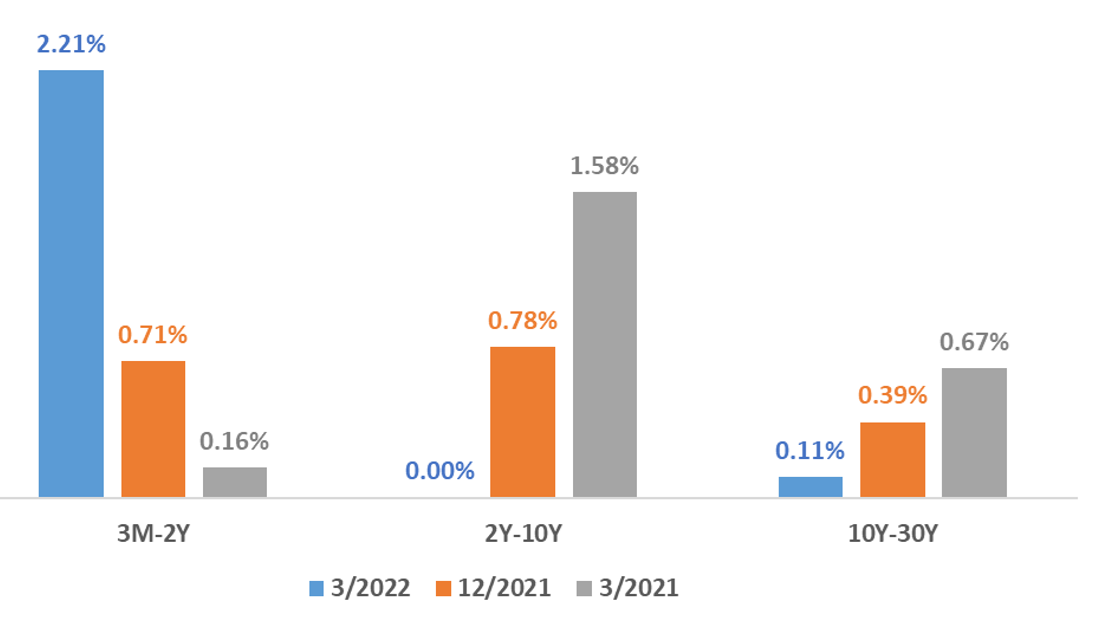

US Treasury Yield Spreads

Change in Yields (3/2022 minus 12/2021)

US Credit Spreads

2022 Theme: Tighter Monetary Policy

2022 Playbook Summary

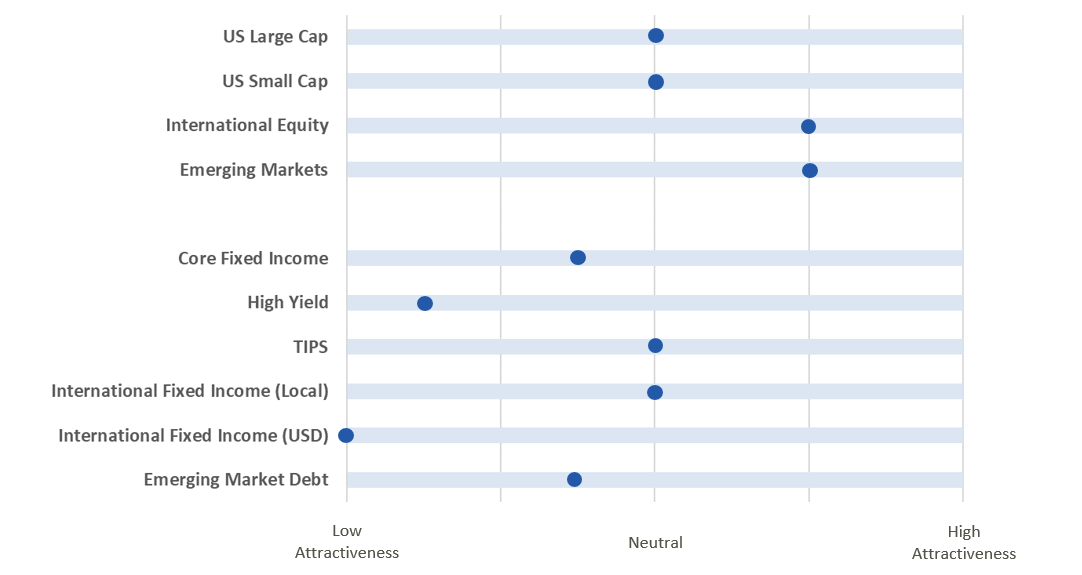

- The above table indicates where each major investment asset class falls on the distribution of attractiveness (from low to high). This table is meant to provide a standardized and comparable view of the level of opportunity in each asset class category.

- In subsequent quarters, we will discuss any movement along the scale for each asset class and the driving forces behind the change in outlook.