Capital Markets Playbook | Q4 2021

2021 Q2 Summary

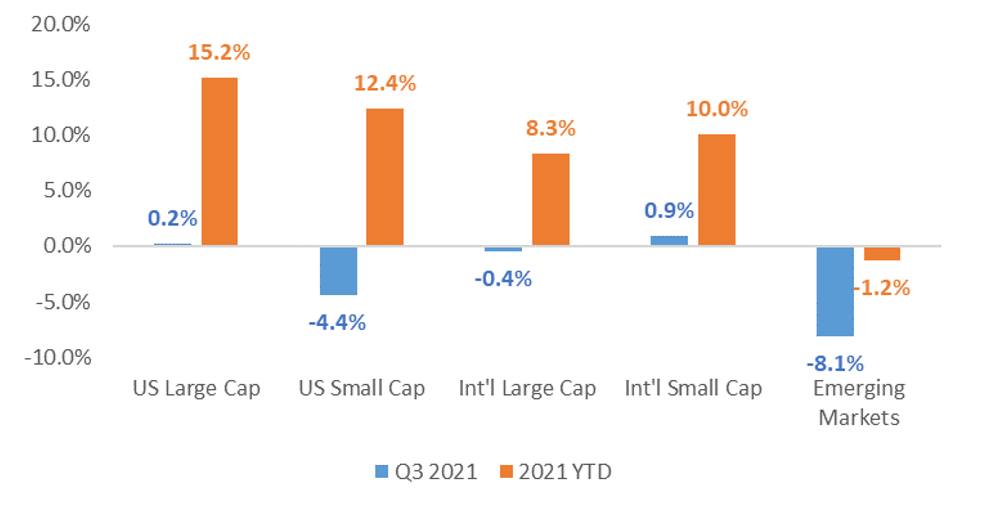

- Equity markets took a breather in September following a historically strong recovery from pandemic lows set in March 2020.

- Despite closing down nearly 5% in September, U.S. large cap equity did post a small gain for the third quarter.

- U.S. small cap and emerging market equities struggled in Q3, ending down 4% and 8% respectively.

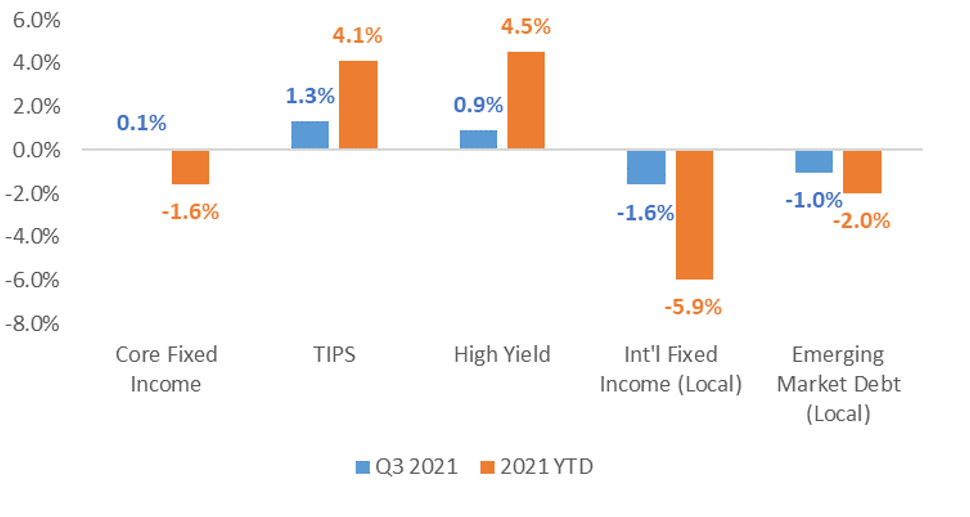

- Most major fixed income markets posted small gains in the third quarter as investor demand for more conservative assets improved.

- Treasury Inflation Protected Securities (TIPS) and High Yield have outperformed most major fixed income assets classes in 2021.

- Treasury Inflation Protected Securities (TIPS) and High Yield have outperformed most major fixed income assets classes in 2021.

Equity Returns

Fixed Income Returns

Macroeconomic Outlook for the Next 6-12 Months

- Economic growth

- Economic activity in developed countries (including the U.S.) will continue to grow above long-term trend rates.

- U.S. economic growth is likely to decelerate in the quarters ahead, but economic activity will remain well above “trend” in 2022.

- The global economic rebound will continue at an uneven pace.

- U.S. and China are likely further along in their respective recoveries. Other developed and emerging market economies are likely to grow at a faster rate than the U.S.

- U.S. economic growth is likely to decelerate in the quarters ahead, but economic activity will remain well above “trend” in 2022.

- Economic activity in developed countries (including the U.S.) will continue to grow above long-term trend rates.

- Inflation

- Supply disruptions are likely to continue for certain goods and services for the next few quarters. Supply-demand imbalances are likely to ease for industrial commodities by mid 2022.

- Strong energy demand over the winter months may push energy prices higher over the short term.

- Expect inflation to remain higher than the Federal Reserve’s 2% target over the short term (sustained “runaway inflation” is unlikely).

- Monetary policy

- Monetary policy will remain highly accommodative over the short term, but the Fed is likely to begin tapering its quantitative easing program in the fourth quarter of 2021.

- The Fed’s short-term policy rate may increase in 2022, but rates will remain historically low through 2023.

- Fiscal policy

- Another round of fiscal stimulus in the U.S. may fall short of earlier expectations, but some agreement on additional spending is likely in 2021.

Market Outlook for the Next 6-12 Months

- Changes in monetary policy, fiscal policy, inflation and interest rates will likely create short-term periods of volatility in equity and fixed income markets.

- The Fed’s tapering activities will put upward pressure on intermediate and long-term interest rates, but a “taper tantrum” is unlikely.

- Fiscal stimulus is likely to be much lower than originally anticipated. Fiscal spending on social programs are likely to be dialed back. “Hard infrastructure” fiscal spending is likely to get through Congress in 2021.

- Inflation will continue to be a topic of concern for the next few quarters. Firms with the ability to pass on higher prices to consumers are likely to outperform over the short term.

- A short-term, moderate pullback in U.S. equity markets is likely (and healthy).

- U.S. large cap equities appear rich from a fundamental perspective and a correction is more likely than it has been over the past year.

- Any correction in equity markets should be orderly. A major market sell off is unlikely, absent a major unexpected macro event.

- On a relative basis, international and emerging market equities still remain attractive from a fundamental perspective. International equities may be better positioned to outperform compared to emerging market equities.

- Value remains attractive relative to growth and is poised to outperform as the global economic recovery continues.

- Fixed income may continue to struggle as intermediate and long-term interest rates are likely to move higher.

- Short-duration fixed income may be the best performing fixed income asset class until the Fed signals its intention to raise short-term interest rates.

- Expect short-term yields to remain near the “zero lower bound” through at least mid 2022.

- Expect the yield curve to steepen marginally until the Fed increases its short-term policy rate.

- Expect the yield curve to flatten once short-term rate hikes begin.

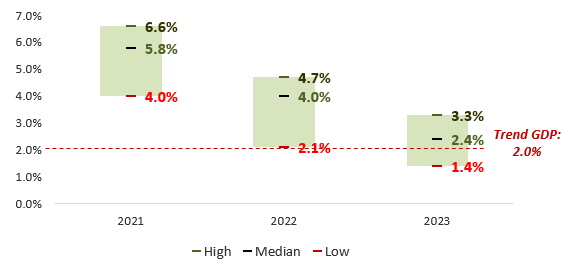

2021 Theme: Above Trend Economic Growth

- U.S. economic growth has been strong in 2021 despite COVID-19 disruptions and increasing inflation.

- U.S. economic growth, as measured by real GDP, is expected to be nearly triple the trend rate in 2021.

- The U.S. economy is likely in mid cycle, meaning that economic activity will probably slow in 2022.

- By the end of 2023, economic growth in the U.S. is expected to be slightly above its long-term trend rate of 2%.

- Takeaways

- The prospects of higher interest rates will likely have a more meaningful impact on future economic growth in the U.S. than any other macroeconomic variable.

- The faster the Fed dials back its accommodative monetary policy, the faster economic growth slows.

US GDP Growth Projections

2021 Theme: Monetary Policy

- The Fed uses its monetary policies to achieve its dual mandate of:

- Full employment

- Price stability

- The Fed’s inflation mandate has been met, but unemployment remains higher than it was before the pandemic.

- If the unemployment rate were closer to 4%, the Fed may consider raising short-term interest rates sooner (current unemployment rate is close to 5.5%).

- Takeaway

- The Fed will likely not begin increasing short-term interest rates until: 1) its tapering program is complete, and 2) unemployment improves further.

- The Fed will likely not begin increasing short-term interest rates until: 1) its tapering program is complete, and 2) unemployment improves further.

US Unemployment Rate Projections

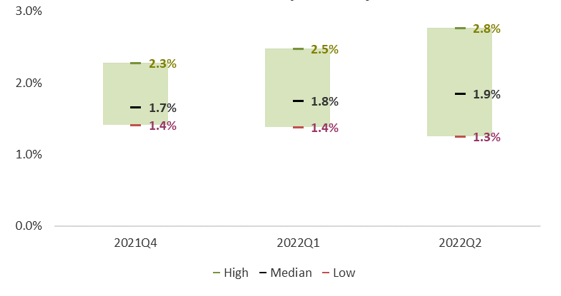

Range of US Inflation Projections

2021 Theme: Steeper Yield Curve

- The U.S. treasury yield curve has steepened meaningfully since the beginning of 2021.

- In other words, intermediate and long-term interest rates have increased at a higher rate than short-term interest rates.

- Short-term rates are likely to remain close to current levels until the Fed raises its short-term policy rate.

- The Fed has implied it may begin raising short-term interest rates in mid to late 2022.

- The Fed is unlikely to adjust its short-term policy rate until it has completely unwound its quantitative easing program.

2-Year US Treasury Yield Projections

10-Year US Treasury Yield Projections

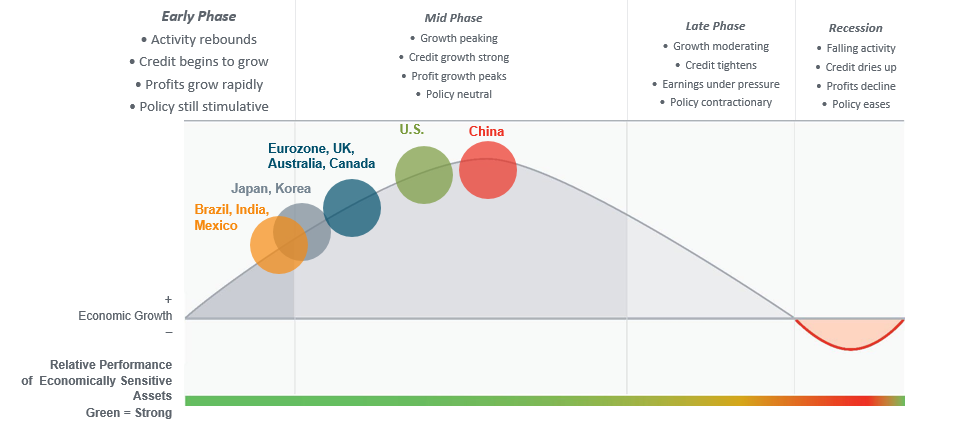

Global Economic Growth Is Uneven

The Economic Cycle

- The U.S. economy has likely shifted into the mid-cycle phase, as a broadening expansion accompanied the economy’s reopening.

- Major economies are on differing trajectories, with a number of developing countries inhibited by their more-limited vaccination and reopening progress.

- The global cycle’s momentum is widening, with staggered reopenings likely leading to ongoing improvement.

2021 Playbook: U.S. Equity

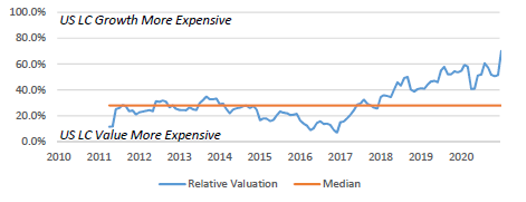

- Value stocks continue to lead YTD performance but underperformed in the quarter. Higher volatility is expected through the end of the year.

- Valuations remain high in certain asset styles.

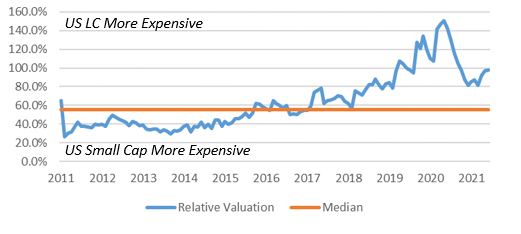

- US large cap stocks are trading at a Forward P/E above their 20-year median, while U.S. small caps are trading slightly below their 20-year median.

- U.S. large cap value looks particularly attractive compared to U.S. large cap growth. We continue to take a balanced approach in client portfolios.

- U.S. small cap stocks look attractive compared to U.S. large cap stocks.

- Earnings growth is expected to remain strong through the end of the year and then slow to more normalized rates in 2022.

- Factors that could impact company profits are the increasing costs associated with supply chain disruptions, labor costs and shortages, the recent rise in energy and transportation costs, etc. If companies are unable to pass these higher costs on to the consumer, companies may miss earnings growth expectations.

Relative Valuation: US Large Cap Growth vs. US Large Cap Value Forward P/E

Relative Valuation: US Large Cap vs. US Small Cap Forward P/S

2021 Playbook: Fixed Income

- Yields for intermediate and longer-term investment grade fixed income asset have steadily been increasing on expectations of strong earnings, economic growth and concerns of continuing above-average inflation.

- A steeper yield curve was not unexpected, but the pace of the steepening has caught some investors off guard.

- In the second quarter of 2021, yields did decrease, yet in a year’s time frame the trend has been to increase.

- Short-dated yields are likely to stick close to current levels until the Fed adjusts its monetary policy to become less accommodative.

- While longer dated yields are expected to continue to increase as economic recovery takes hold and inflation persists, it is likely that the pace of increase is gradual until the Fed begins adjustments in its monetary policy.

- Takeaway

- Shorter duration fixed income is likely to continue to outperform longer duration fixed income as the economic recovery gains momentum.

- Yields for intermediate and longer-term investment grade fixed income asset have steadily been increasing on expectations of strong earnings, economic growth and concerns of continuing above-average inflation.

- A steeper yield curve was not unexpected, but the pace of the steepening has caught some investors off guard.

- In the second quarter of 2021, yields did decrease, yet in a year’s time frame the trend has been to increase.

- Short-dated yields are likely to stick close to current levels until the Fed adjusts its monetary policy to become less accommodative.

- While longer dated yields are expected to continue to increase as economic recovery takes hold and inflation persists, it is likely that the pace of increase is gradual until the Fed begins adjustments in its monetary policy.

- Takeaway

- Shorter duration fixed income is likely to continue to outperform longer duration fixed income as the economic recovery gains momentum.

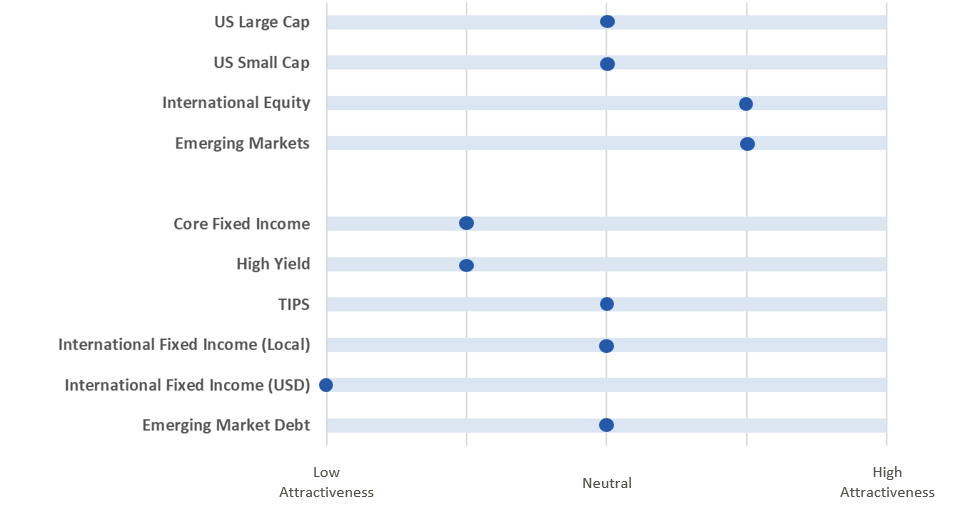

2021 Playbook Summary

- The above table indicates where each major investment asset class falls on the distribution of attractiveness (from low to high). This table is meant to provide a standardized and comparable view of the level of opportunity in each asset class category.

- In subsequent quarters, we will discuss any movement along the scale for each asset class and the driving forces behind the change in outlook.