2020 Summary

- Despite a massive slowdown in economic activity, a huge spike in unemployment, and a contentious general election in the US, equity markets did tremendously well in 2020.

- Global equity markets plunged more than 30% in February and March, but finished up for the year.

- International Large Cap stocks were the laggard in 2020, finishing the year up by about 8%.

- Fixed Income markets also posted strong gains in 2020.

- Unhedged International Fixed Income posted the strongest gains, up more than 10% in 2020.

- As markets have already priced in a return to some version of “normal” already, investors should be prepared to see some new “winners” across capital markets.

Equity Performance 2020

Fixed Income Performance 2020

Themes for 2021

- 2020 was a good reminder to investors of the following:

- Downside shocks to markets are often quick and terribly difficult to predict.

- The market is forward looking and places more emphasis on the long term than it does on the immediate future.

- As a result of this forward looking dynamic, equity markets may be priced completely different than what economic reality currently suggests.

- As vaccines begin to enter the marketplace, 2021 certainly offers a lot of hope to folks across the globe.

- Equity markets have exploded high based on the hope that a return to “normal” is imminent.

- But, have stock prices moved too high too fast? Will corporate earnings be able to keep pace with expectations for a strong 2021 and 2022.

- Themes for 2021

- COVID vaccines should lead to stronger business and consumer confidence, higher spending, and above trend economic growth.

- Above trend economic growth will result in reflation and an improvement in unemployment across the globe.

- Monetary policy will remain accommodative and rates will remain near historic lows.

- Healthcare policy, tax policy, trade policy, and fiscal policy will be more predictable.

- Valuations in many equity asset classes look extremely expensive and certain equity asset classes may struggle as a result.

- Stronger economic growth may result in a “leadership change” in equity asset classes.

2021 Themes

The Virus and Vaccines

- The rollout of vaccines across the globe will slowly put an end to the pandemic.

- Several vaccines have already hit the market place and more are expected to be approved for emerging use in early to mid 2021.

- Despite the optimism surrounding the vaccines, it will take a few months before it will become clear just how successful vaccinations will be.

- The first several months of 2021 will result in millions of inoculations, but the broader population will not have access to the vaccine until the summer months.

- The success of the vaccination programs will be depend on the following:

- Will there be an ample supply of raw materials needed to manufacture the vaccines at a large scale?

- Will policymakers implement a well functioning distribution and delivery system?

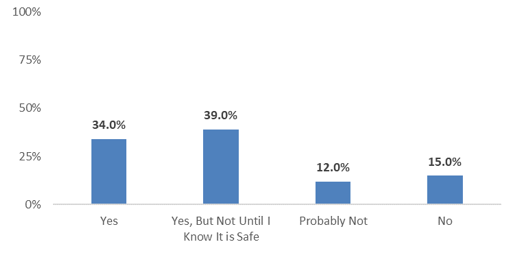

- Will at least 70% of the population to take the vaccine?

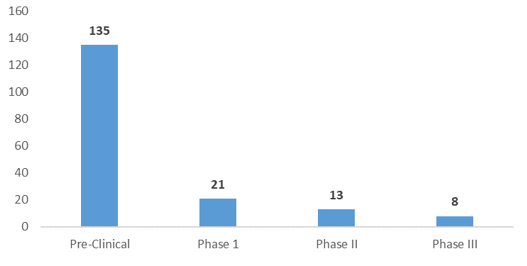

Vaccine Candidates

Trial Status

Will Americans Take a COVID Vaccine?

Survey Data

Above Trend Economic Growth

Economic Growth

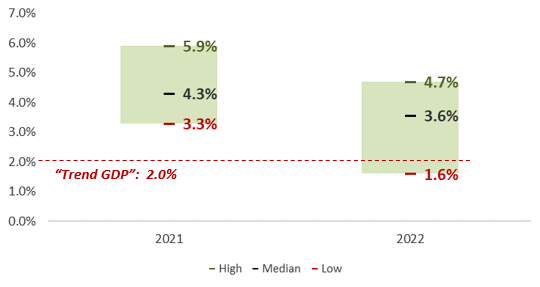

- Economic growth may be “soft” in early 2021, with a surge of economic activity expected in the second half of the year.

- Expect economic growth in many countries (including the US) to be far higher than the historical trend.

Unemployment

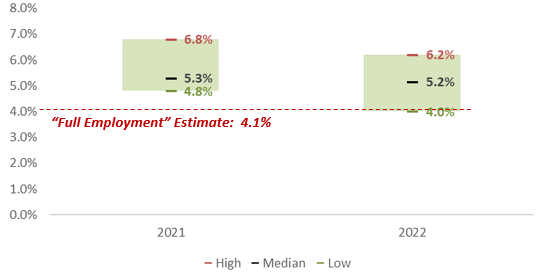

- Unemployment will improve in the US and abroad.

- Current unemployment rate: 6.7%

- In the US, unemployment will remain below the Federal Reserve’s measure for “full employment” through the end of 2022.

US GDP Growth Projections

US Unemployment Rate Projections

US Dollar Weakness

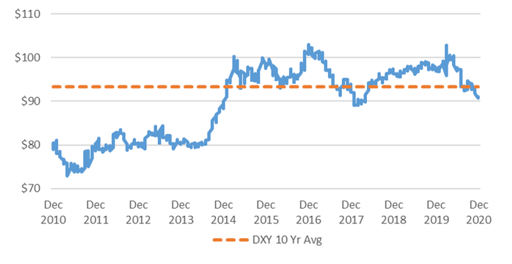

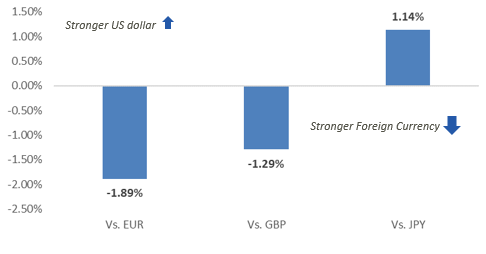

- Since the onset of the Global Pandemic, the US dollar has weakened relative to a basket of major currencies.

- Dollar weakness is likely to continue in 2021, due to the following factors:

- Coordinated global economic growth is likely to lead to “capital flight” out of the US and into International/Emerging Market economies

- Explosive growth of money supply and expanding US fiscal deficit as a result of stimulus measures.

- Asset classes that benefit from dollar weakness:

- International and Emerging Market Equities

- Value equities (US)

- International Fixed Income (Unhedged)

- Emerging Market Debt (Unhedged)

US Dollar Index

US Fiscal Deficit Projections

Reflation

- Although the risk of significantly higher levels of inflation remains low, inflation expectations are likely to move higher in 2021.

- Inflationary expectations are likely to increase due to:

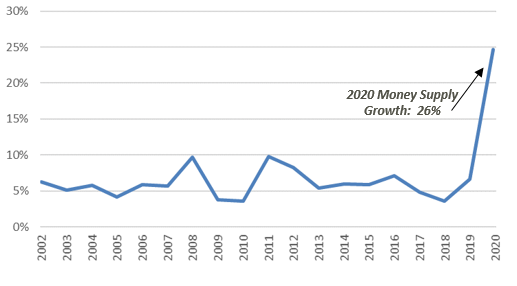

- Explosive growth in US money supply as a result of massive stimulus measures

- The Federal Reserves commitment to achieve “above target” inflation from some period of time

- An imbalance between supply and demand that results from the release of “pent up demand”

- Asset classes that benefit from a growth in inflation expectations:

- Emerging Market Equities

- Value equities (US)

- Real Assets (Commodities, REITS)

- Treasury Inflation Protected Securities

Growth in Money Supply

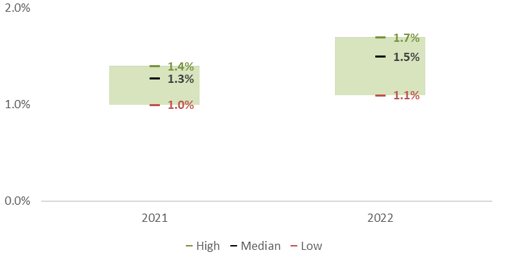

Range of US Inflation Projections

Low Rates

- Monetary policy will remain accommodative as the global economy continues to recover from the pandemic.

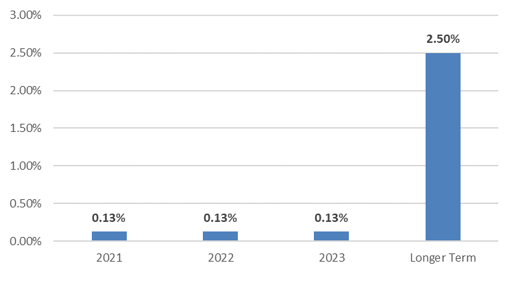

- The Federal Reserve will likely continue its quantitative easing program through 2021 and expects to keep short term rates near 0% until 2023.

- Accommodative monetary policy, reflation, and strong economic growth will lead to a steeper yield curve in 2021.

- Expected 2-10 year spread by end of 2021: 100-125bps

- Asset classes that benefit a steepening in the yield curve:

- US Small Cap Equities

- Value equities (US)

- Short Duration Fixed Income

Projected Fed Funds Rate Target

10 - Year US Treasury Yield Projections

More Certainty from Policymakers

Investors were uncertain for much of 2020 as it related to the decisions made by policy makers. 2021 is likely to be more predictable.

- Fiscal policy

- Expect governments around the world to continue to support economic activity through fiscal stimulus.

- Additional fiscal stimulus will occur in the US, but questions remain over the potential amount and timing.

- Trade Policy

- A softening of trade disputes between the US and European (and some Asian) trade partners is likely.

- Tariffs may remain in some US trade relationships (ex: China), but additional tariffs are unlikely.

- Tax Policy

- Although some tax reform is possible in the US, the prospects of major tax reform may need to wait until 2022.

- The slim majority held by Democrats may limit the potential for large scale tax reform, at least until the economy is on more solid footing.

- Although some tax reform is possible in the US, the prospects of major tax reform may need to wait until 2022.

- Healthcare Policy

- Significant changes in healthcare policy are unlikely and uncertainty about the future of the Affordable Care Act will dissipate.

- Climate Policy

- US and International governments will place a greater focus on investing in clean and alternative energy.

2021 Playbook

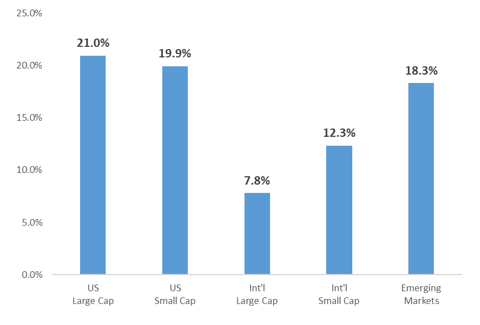

Global Equity

- Although strong economic recovery is likely in 2021, certain portions of the equity market may struggle to produce high returns due to elevated valuations.

- International and Emerging markets may be expensive from a fundamental perspective as well, but are not nearly as expensive as US stocks.

- Factors that may provide a tailwind for International and Emerging Market equity investors:

- Attractive valuations relative to US stocks

- Expectations for a weaker US dollar

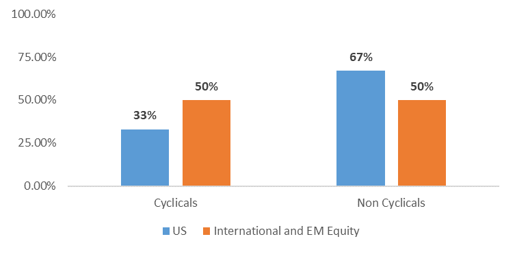

- International and EM equity composition is more cyclical in nature than US equity

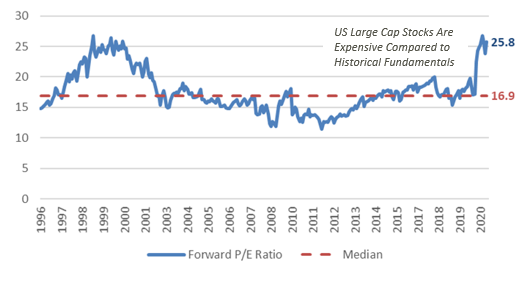

S&P 500 Forward P/E

Expected US Dollar Performance vs. Major Currencies 2021

Equity Market Composition

Allocation to Cyclicals vs. Non-Cyclicals

US Equity

- High flying US Large Cap Growth stocks are among the most expensive equities in the world heading into 2021.

- Ex: Facebook, Apple, Amazon, Alphabet, Microsoft, etc.

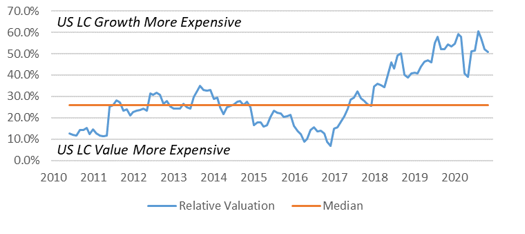

- From a relative valuation perspective, US Large Cap Value look particularly attractive compared to US Large Cap Growth.

- Additionally, Value stocks tend to outperform during periods of strong economic growth, higher inflation, and higher interest rates….all of which is expected in 2021.

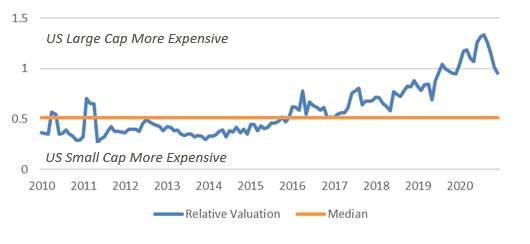

- From a relative valuation perspective, US Small Cap stocks looks particularly attractive compared to US Large Cap stocks.

- Small Cap stocks tend to outperform Large Cap stocks during periods of US dollar weakness.

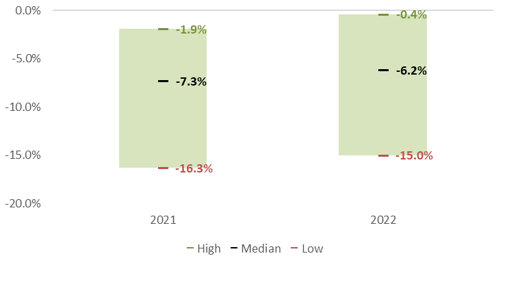

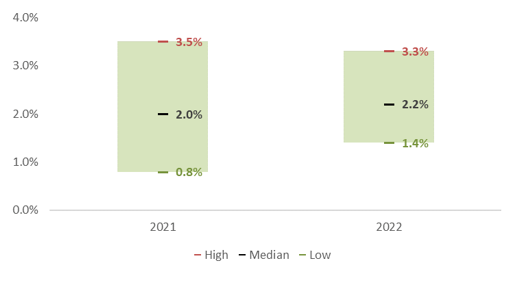

Relative Valuation

US Large Cap vs. Us Small Cap

Forward P/E

Relative Valuation

US Large Cap Growth vs. US Large Cap Value

Forward P/E

Real Assets

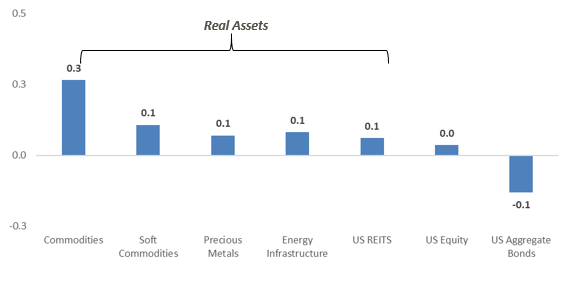

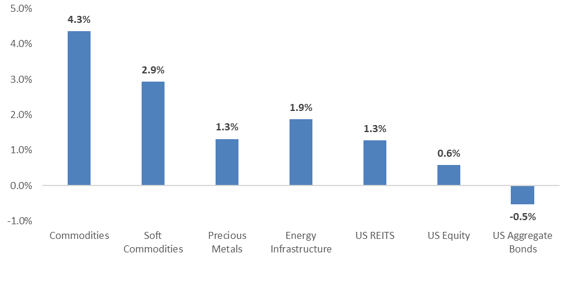

- A well-diversified investment portfolio should include “real assets”, or assets that tend to outperform during periods of increasing inflation expectations.

- Real assets include:

- Soft Commodities (agricultural commodities)

- Precious Metals (Gold, Silver, etc)

- Energy Infrastructure

- REITS

- A well diversified basket of commodities is likely to provide the best protection against unexpected increases in inflation.

- Energy Infrastructure and REITS do provide some protection against inflation, but tend to have a higher correlation to equities than Commodities.

- An additional allocation to commodities is not recommended at this time, but may be prudent in the months ahead.

Correlation to Inflation

Price Performance Given 1% Increase in Inflation

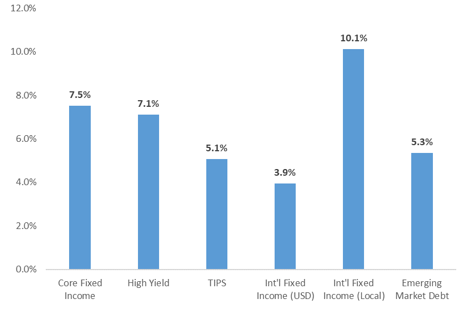

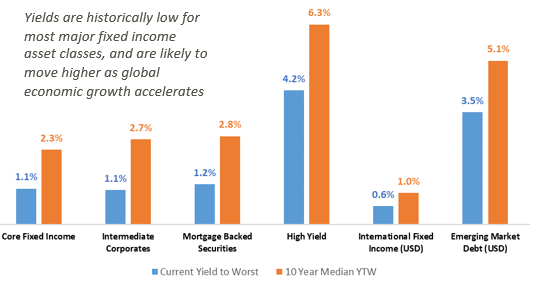

Fixed Income

- Although interest rates are expected to remain low on the short end of the yield curve for some time, it is likely that longer portions of the curve steepen in 2021.

- Investors that are seeking “outperformance” in the fixed income portfolio need to balance the following fixed income risks:

- Interest rate risk

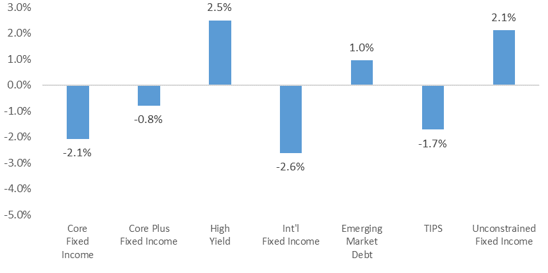

- Reduce the risk associated with a steeper yield curve using shorter duration fixed income assets (ex: Unconstrained Fixed Income).

- Credit Risk/Default Risk

- Add exposure to actively managed credit products that help improve portfolio yield (ex: Core Plus Fixed Income)

- Inflation Risk

- Add exposure to fixed income investments that perform well during periods of higher than expected inflation (ex: TIPS).

- Interest rate risk

Fixed Income Yield to Worst

1 Year Total Return if Interest Rates Increase by 0.50%

Cash

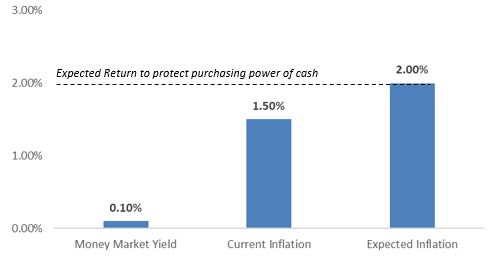

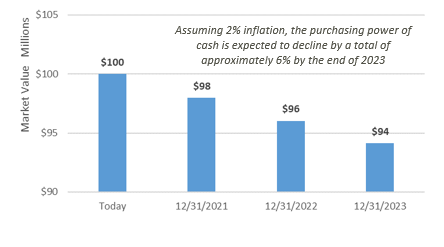

- Investors holding cash are likely to lose purchasing power in the years ahead.

- The Federal Reserve has committed to keeping its policy rates near the zero lower bound for an indefinite period of time.

- The challenge associated with holding cash:

- Savers (i.e. holders of cash) are likely to see the purchasing power of their cash decline over the next few years.

- In order reduce the risk of a loss in purchasing power, savers must take more risk.

"Savers" Will Not Keep Up With Inflation Any Time Soon

The Erosion of Purchasing Power Over Time in 0% Rate Environment

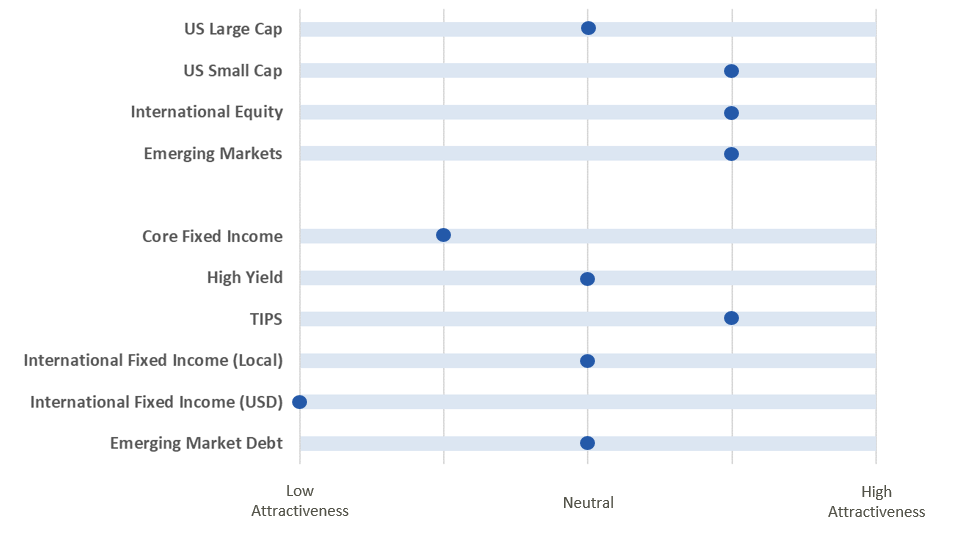

2021 Playbook Summary

- The table indicates where each major investment asset class falls on the distribution of attractiveness (from low to high). This table is meant to provide a standardized and comparable view of the level of opportunity in each asset class category.

- In subsequent quarters, we will discuss any movement along the scale for each asset class and the driving forces behind the change in outlook.