Capital Markets Outlook | Q3 2020

Themes For the Second Half of 2020

- Despite the strong rebound in equity markets since March 23, uncertainty remains much higher than normal.

- Investors will continue to focus on the following themes as they attempt to project just how quickly economic growth will rebound in the second half of 2020 (and beyond):

- Coronavirus

- Will policymakers be able to avoid shutting down certain sectors of the economy as virus growth rates continue to escalate?

- Will schools open in the Fall?

- Will the health care system have the capacity to handle higher case loads?

- Will an effective vaccine be available for distribution in early 2021?

- Fiscal Stimulus

- Will Democrats and Republicans be able to agree to another round of stimulus before summer recess?

- US Trade Policy

- Will the US escalate trade disputes with trade partners in Europe and China?

- General Election

- Will there be a power shift in Washington? If so, will potential regulatory policy and tax policy changes impact corporate earnings expectations in a material way?

- Coronavirus

What to Expect:

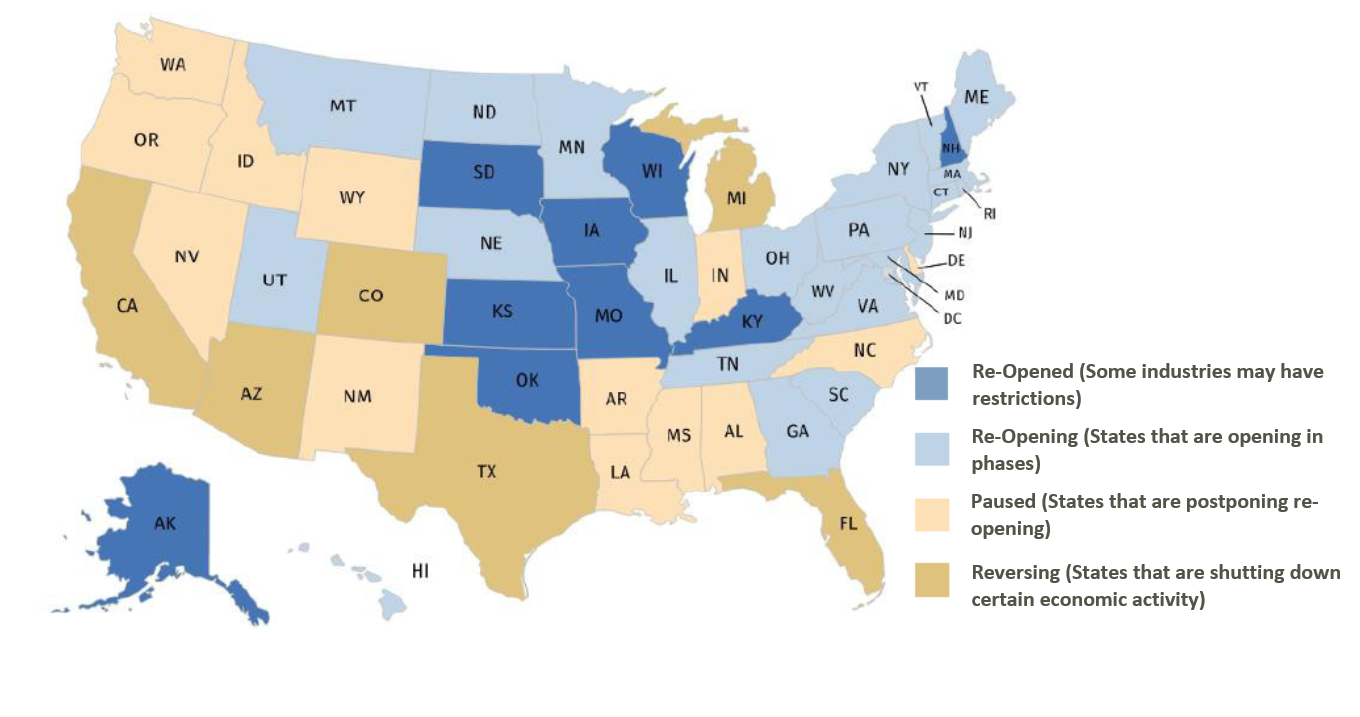

Targeted "Shutdowns"

- Re-opening activities are likely to be sporadic in the second half of 2020 as virus cases grow.

- Expect certain states and certain industries to be impacted more than others.

- States with high population densities are more likely to pause or reverse economic re-openings than states with lower population densities.

- Industries associated with travel and entertainment are likely to face a slower recovery until a safe and effective vaccine is distributed.

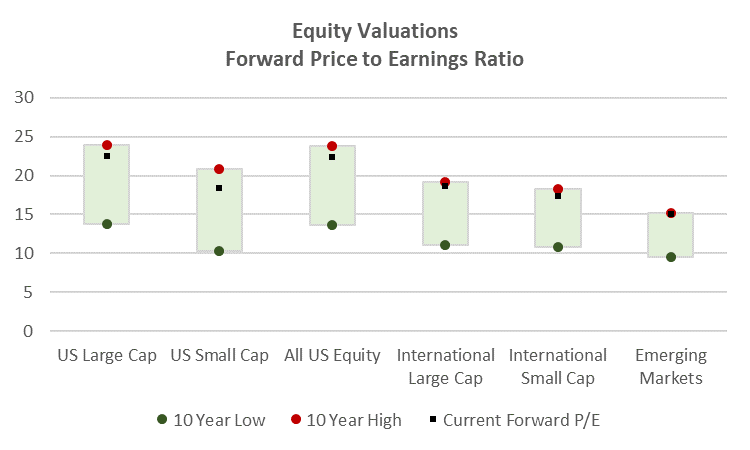

Equities Have Limited Upside, Increased Downside Risk Over the Short Term

- Equity markets have rebounded strongly since bottoming in March.

- Some equity markets posted positive performance in the first half of 2020.

- Markets have looked past historically slow economic growth and high unemployment, assuming that growth will accelerate in the quarters ahead.

- As a result, stocks have rarely been more expensive over the past 10 years.

- If the current expectations for corporate earnings end up being too optimistic, stocks are likely to move lower.

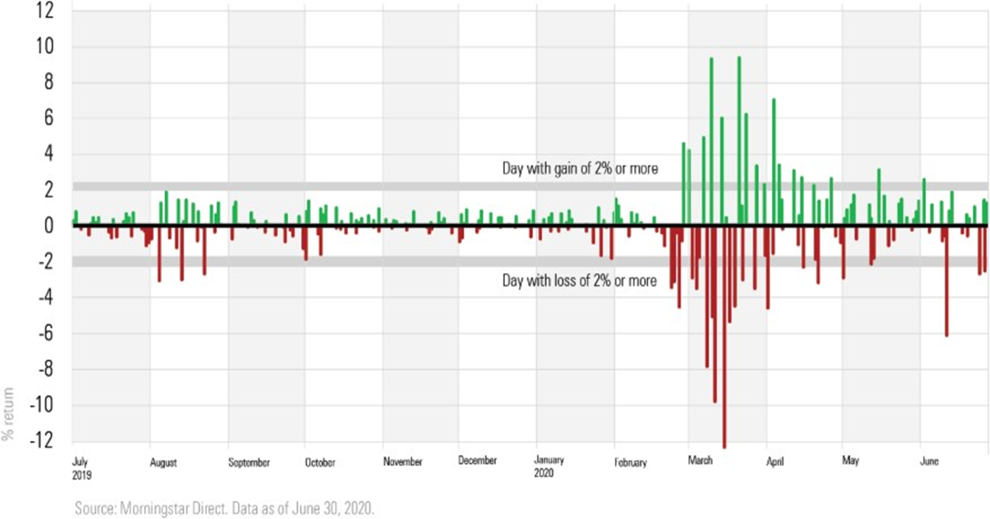

Continuation of Higher Than Normal Equity Volatility

- Although volatility has declined in the past couple of months, it is still much higher than “normal”.

- Expect volatility to continue to remain higher than normal until a safe and effective vaccine is ready for distribution.

Daily Percentage Change: S&P 500 Index

Interest Rates

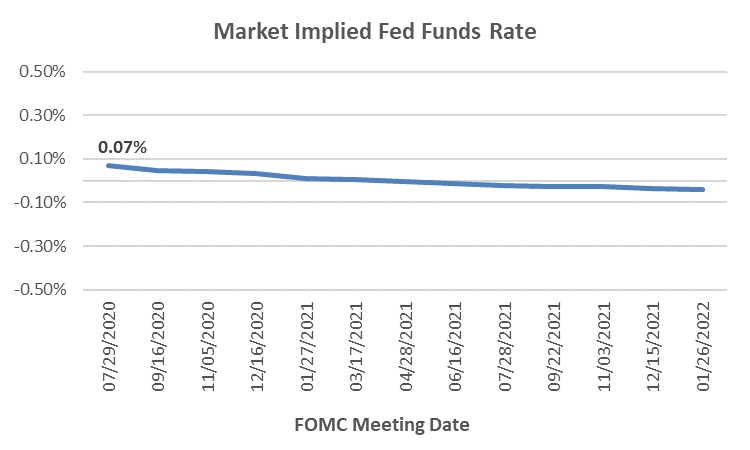

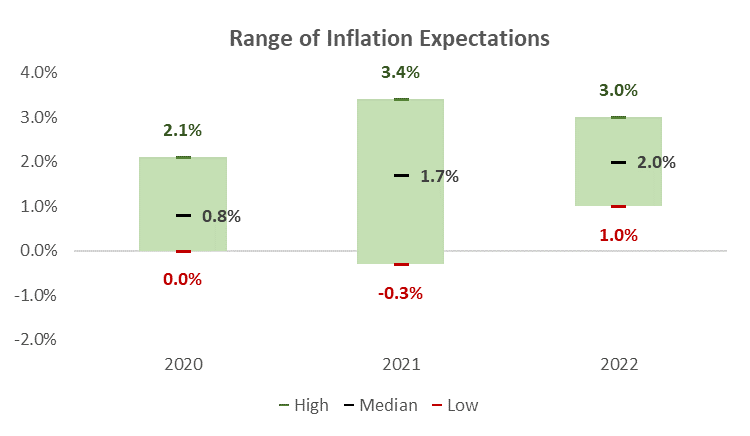

Low Interest Rates, Slow Growth in Inflation

- High unemployment and low inflation are likely to keep rates low for an extended period of time.

- Inflation, while still very low, should tick higher as consumer confidence and business confidence improves.

- It is likely that inflation will grow slowly, but remain below (or near) the Fed’s inflation target of 2% over the next couple of years.

Escalation of Trade Issues

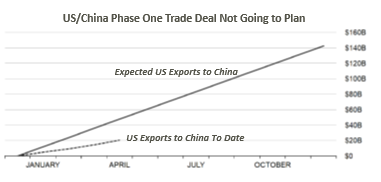

- The US/China Phase One trade deal is in jeopardy as US exports to China are well below what was expected.

- Tensions over the origin over the coronavirus and the new security law in Hong Kong have not helped the trade situation between the US and China.

- Trade disputes with other US trade partners (Japan, European countries) could also escalate in the months leading into the general election.

- Although trade issues with European trading partners could create volatility over the short term, US trade disputes with China are likely to persist over the longer term, regardless of which party has power in Washington.

Summary

- Markets are likely to remain volatile as a number of uncertainties weigh on consumer and business confidence.

- Stocks look expensive for a historical valuation perspective and short term equity risk is skewed to the downside.

- Although the likelihood of a large scale economic shut down is unlikely, many regions in the US are likely to see pauses or reversals to re-opening activities as it appears virus cases will continue to grow over the short term.

- Interest rates will remain low for quite some time as unemployment is likely to remain above 2019 levels for at least another year.

- Inflation may tick higher in the months ahead, but is likely to stay near the Fed’s long term target of 2%.

- US trade policy may create additional anxiety in the months ahead as disputes with China and European trade partners appear to be escalating.

- The general election in the US is likely to create significant headline risk in the lead up to November.

- Equity markets may be able to shrug off all of these risks if investors remain confident that a safe and effective vaccine will be available in early 2021.