Market Flash Report | December 2021

Economic Highlights

United States

- After slowing in Q3, U.S. economic growth is expected to have accelerated in Q4. Current estimates for the quarter are in the range of 6.5-7.5%, with the Atlanta Federal Reserve’s current estimate sitting at 7.6%. GDP estimates for the full year 2022 are in the 3-4% range, which is well above trend levels, but 2023 should see a sharp deceleration. COVID-19 was relatively benign for most of Q4 until the Omicron variant surge started impacting travel and other key industries late in the year. We believe Q4 and Q1 2022 GDP forecasts will have to come down due to the impact of Omicron on business activity and consumer spending. Overall, the U.S. economy was the real star performer in 2021.

- The November employment report disappointed with only 210,000 new jobs added to the economy. The estimate was 550,000 and the prior two months of readings were revised higher. The unemployment rate fell sharply to 4.2% from 4.6%, even though the labor force participation rate increased for the month to 61.8%, its highest level since March 2020. The broader U6 unemployment rate also declined sharply from 8.3% to 7.8%. Sectors showing the biggest gains in November included professional and business services (90,000), transportation and warehousing (50,000) and construction (31,000). Wages rose 4.8% Y/Y and job growth in leisure and hospitality was weak.

- We continue to believe the biggest risk to equities and other risk assets is runaway inflation that leads to a more hawkish Fed, forcing the Fed to tighten monetary policy more aggressively than expected. Thus far, the Fed will be ending its bond buying program by March with three rate hikes forecast in 2022, according to the latest dot chart. Based on the Fed Funds Futures, the market is currently pricing in 3-4 rate hikes this year. Sustained inflation is a problem and it could ultimately lead to a more aggressive rate hike schedule from the Fed. One potential wildcard is COVID-19/Omicron which could put a dent in economic growth. Any weakness could prompt the Fed to back off a bit to boost and support growth.

Non-U.S. Developed

- The pace of eurozone economic growth slowed in December as rising COVID-19 infection rates hit service sector activity, offsetting improved manufacturing growth amid alleviating supply delays. Firms’ costs and average selling prices continued to rise sharply, though rates of increases cooled from November’s record highs. The Eurozone Composite PMI fell to 53.4 in December from 55.4 in November. The composite hit a 9-month low while the service sector hit an 8-month low and manufacturing hit a 10-month low. With the eurozone implementing stricter/harsher restriction measures due to COVID-19, risk is to the downside for the economy already dealing with rising prices and supply chain shortages.

- The Japanese economy is expected to accelerate its expansion in fiscal 2022 following a sharp turnaround toward the end of 2021 as private consumption continues to recover with subdued coronavirus infections. Analysts predict the world's third-largest economy will see annual real 2-4% growth in fiscal 2022 starting April, even though concerns remain about a COVID-19 resurgence and the lingering global semiconductor shortage. The government predicts 2.6% growth in fiscal 2021, followed by a 3.2% increase in fiscal 2022. Economists say strong growth is expected especially in the first half of 2022 in Japan, thanks to restaurants and bars and other hospitality businesses returning to normal operations and the government's stimulus initiatives.

Emerging Markets

- The World Bank recently cut its forecast for the Chinese economy in 2021 and 2022. The bank now expects China's GDP to expand 8% in 2021 compared with a year ago, down from its previous forecasts of 8.1% from October and 8.5% from June. It also cut its 2022 forecast from 5.4% to 5.1%, which would mark the second slowest pace of growth for China since 1990, when the country's economy increased 3.9% following international sanctions related to the 1989 Tiananmen Square massacre. China's economy grew 2.2% in 2020. China was the only major economy to post positive growth in 2020, but downside risks have increased over the past year, led by the property sector downturn, the government’s regulatory crackdown and rising Omicron cases.

- In response to slowing economic growth, the Chinese central bank cut its main lending interest rate for the first time in 20 months, along with a 50 bps cut to the Reserve Requirement Ratio. Unlike past downturns where the Chinese government could boost growth through infrastructure and real estate investment, it appears to have fewer options available. Given the current property sector troubles, further real estate investment seems unlikely. As the government attempts to rebalance the economy towards the consumer, increased spending will be needed to support growth.

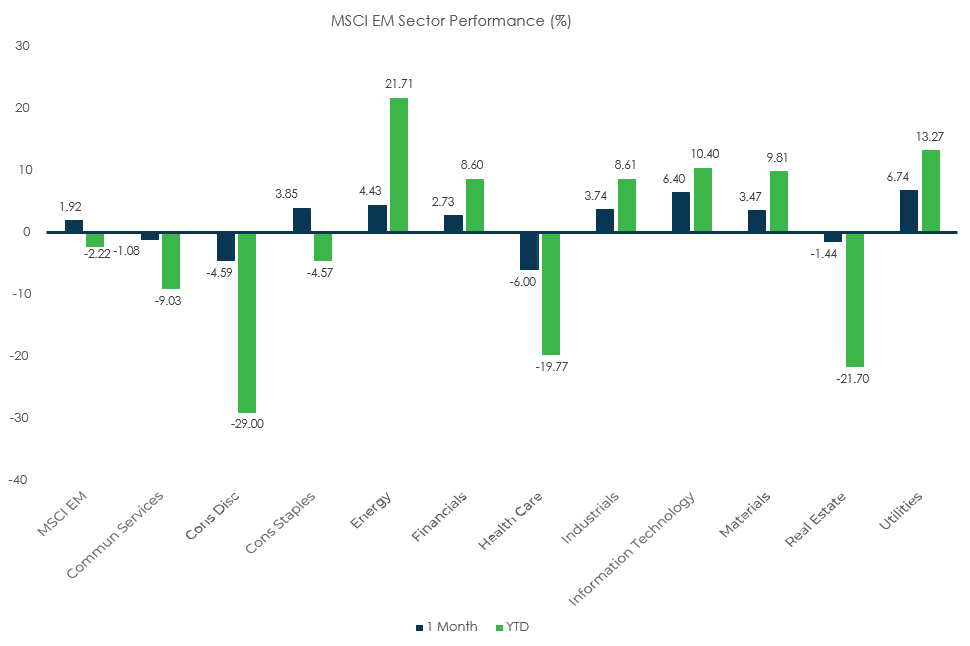

- EM equities and bonds struggled in 2021 while developed economy assets largely raced higher. The downturn in Chinese equities was largely to blame, but the growth story in EMs suffered a bit relative to developed markets. 2022 will be an important year for EMs to demonstrate the attractiveness of their long-term investment thesis. GDP and earnings growth have lagged the U.S. in recent years and investors are struggling to see the upside of investing in EM equities that have routinely lagged developed markets. Investors have also been questioning the investability of Chinese equities with the recent government regulatory crackdown. Risks have increased while the long-term investment thesis has clearly been damaged. Inflation and tighter global monetary policy is another reason to be cautious. Persistent underperformance and the potential for mean reversion are the main positive short-term investment thesis drivers.

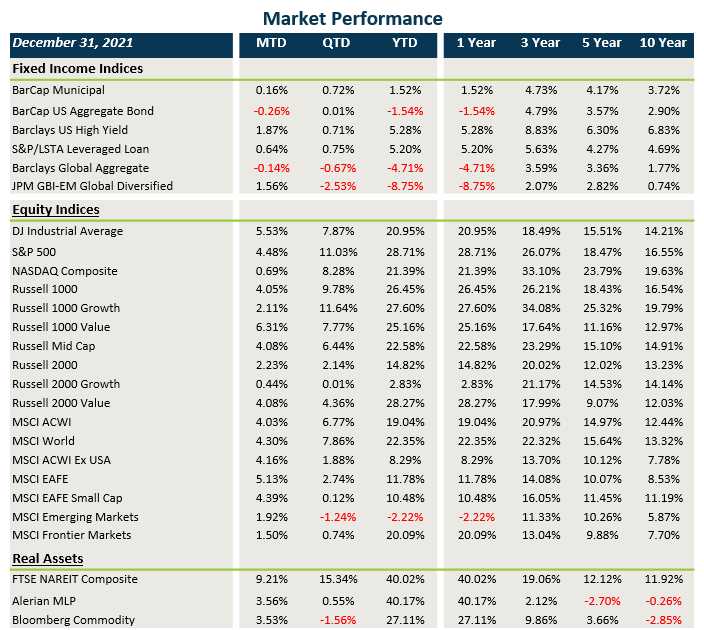

Market Performance (as of 12/31/21)

Fixed Income

- Treasury yields were range-bound to end the year and this led to slight gains in core fixed income and better returns in munis.

- Credit spreads tightened in December with solid gains posted in investment grade, high yield and loans.

- Bonds outside the U.S. were hurt by the backup in rates.

U.S. Equities

- Global equities ended the year on a strong note, led by a resurgence of value stocks.

- Large cap stocks outperformed small

- cap stocks in the U.S.

- LCG beat LCV in 2021, but SCV smashed SCG for the year.

Non-U.S. Equities

- Non-U.S. equities rebounded sharply last month, led by strong returns from Europe.

- Similar to the U.S., value stocks outperformed growth stocks, and large caps beat small caps.

- U.S. dollar weakness boosted EAFE returns by 81 bps, but currency weakness in EMs cost investors approximately 40 bps of performance in December.

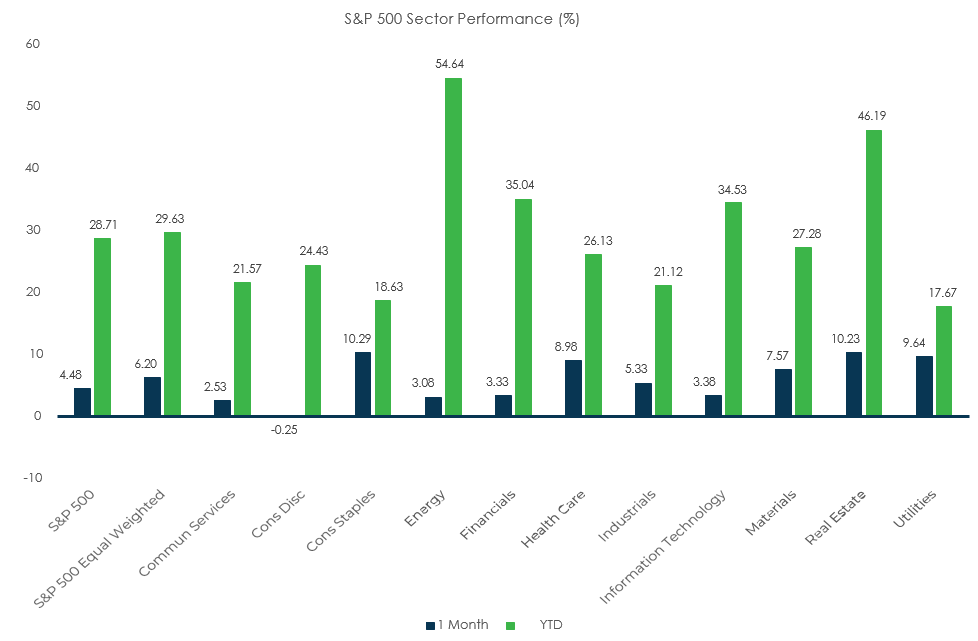

Sector Performance – S&P 500 (as of 12/31/21)

Sector Performance – Russell 2000 (as of 12/31/21)

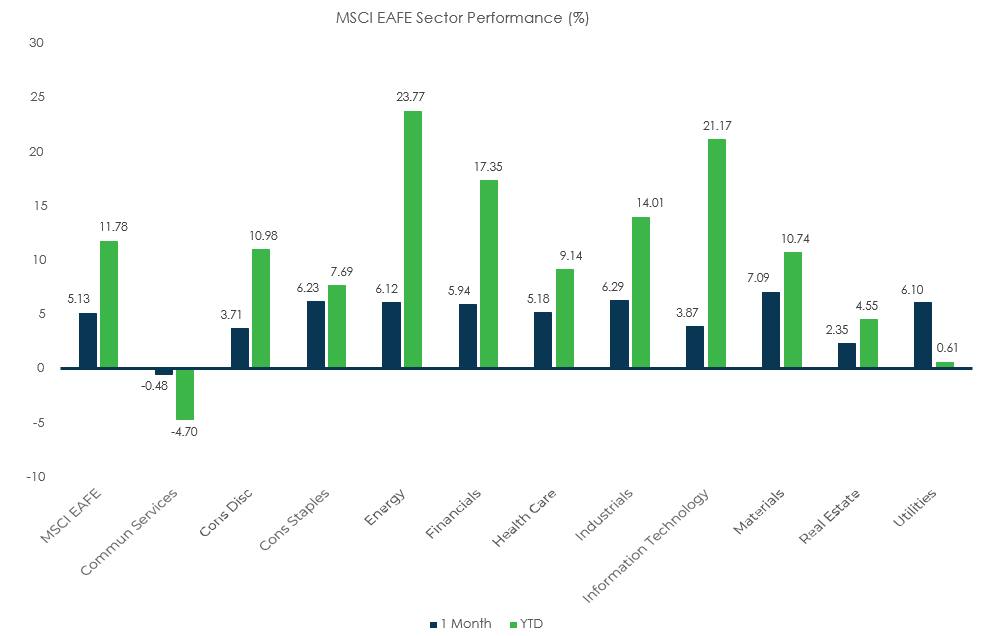

Sector Performance – MSCI EAFE (as of 12/31/21)

Sector Performance – MSCI EM (as of 12/31/21)