Market Flash Report | January 2022

Economic Highlights

United States

- The U.S. economy grew at a much better than expected pace to end 2021 due to sizeable boosts in inventories and consumer spending, and despite signs that the acceleration likely tailed off toward the end of the year. Gross domestic product increased at a 6.9% annualized pace in the fourth quarter, well ahead of the 5.5% estimate. Consumer activity and business spending led the gains, which propelled the U.S. economy to its strongest full year (+5.7%) since 1984. Consumer activity, which accounts for more than two-thirds of GDP, rose 3.3% for the quarter. Gross private domestic investment, a gauge of business spending and inventory build, soared 32%. Inventories added 4.9% to the headline growth, boosted in particular by motor vehicle dealers.

- Omicron likely created weakness in the employment market during January. While the official employment report is due February 4, the latest reading from ADP showed a decline of 301,000 in private payrolls in January. The estimate was for a gain of 200,000 and this was the first negative reading since December 2020. The pandemic-sensitive leisure and hospitality industry was the hardest hit, losing 154,000 jobs. Economists expect the non-farm payroll report on February 4 to show a gain of 150,000 new jobs during January. The Federal Reserve will be watching closely as it has indicated that the economy is nearing full employment and rate hikes are likely to begin in March.

- The manufacturing sector in the U.S. softened a bit last month with the ISM Manufacturing Index falling to 57.6 from 58.8 in December. New orders weakened modestly while production and employment strengthened. The latest reading on the service sector showed some softening due to declines in business activity and new orders. Respondents continue to cite supply chain bottlenecks as a major issue along with higher sustained raw input prices.

- Rates and equity markets have stabilized over the past week and higher quality growth has moved higher. While growth/tech stocks will continue to be sensitive to higher rates, not all growth is created equal and we believe there will be increased bifurcation between high quality and low quality unprofitable growth stocks

Non-U.S. Developed

- The eurozone economy grew 0.3% Q/Q or 4.6% Y/Y in Q4. Based on initial estimates, eurozone GDP advanced 5.2% in 2021. Spain (+2.0%) recorded the highest increase compared to the previous quarter, followed by Portugal (+1.6%) and Sweden (+1.4%). Declines were recorded in Austria (-2.2%), Germany (-0.7%) and Latvia (-0.1%). The latest HIS Composite PMI reading from the eurozone showed weakness. The gauge fell to an 11-month low of 52.4 in January although there was dispersion between services and manufacturing. The service sector hit a 9-month low while manufacturing activity hit a 5-month high.

- The Japanese economy is expected to accelerate its expansion in fiscal 2022 following a sharp turnaround toward the end of 2021 as private consumption continues to recover with subdued coronavirus infections. Analysts predict the world's third-largest economy will see annual real 2-4% growth in fiscal 2022 starting April, even though concerns remain about a COVID-19 resurgence and the lingering global semiconductor shortage. The government predicts 2.7% growth in fiscal 2021, followed by a 3% increase in fiscal 2022. Economists say strong growth is expected especially in the first half of 2022 in Japan, thanks to restaurants, bars and other hospitality businesses returning to normal operations and the government's stimulus initiatives.

Emerging Markets

- China’s economy grew by 8.1% in 2021 as industrial production rose steadily through the end of the year and offset a drop in retail sales. Fourth quarter GDP rose by 4% Y/Y, slightly ahead of the 3.6% increase forecast by economists. For the full year, economists expected an average of 8.4% growth in 2021. Industrial production increased 4.3% Y/Y in December, fixed asset investment grew by 4.9% Y/Y, investment in real estate rose 4.4% and manufacturing investment increased 13.5%. One concern is the big miss in retail sales. Retail sales grew only 1.7% Y/Y in December, falling short of expectations by a wide margin.

- China and many other countries in Asia have zero tolerance COVID-19 policies in place that have led to weakness in consumer and business spending during periods of high incidence. Several investment banks such as Goldman Sachs and Morgan Stanley have trimmed their 2022 GDP growth estimates for China based on their strict COVID-19 restrictions in place to control the pandemic.

- While most of the developed and emerging world are implementing tighter monetary policy, China has shifted towards more stimulus and easing to boost/support growth. The Chinese government has cut several key borrowing rates and the expectation is for more cuts in the near future. The balancing act within China will be the slowing consumer due to the zero tolerance COVID-19 policies and supporting economic growth. Infrastructure/investment spending is likely to be the answer from the government to boost growth in 2022. China’s policy was a headwind for the global economy last year, but should provide a tailwind in 2022.

- It is nice to see some degree of decoupling occur between U.S. and emerging markets early in 2022. EMs have lagged U.S. equities by a wide margin for the past decade, but they provided relative outperformance in a very challenging January market environment. Most EM gains have come from the rebound in China and strong gains from Brazil. EMs are cheap on a relative basis and most countries have done a good job staying ahead of the inflation curve. While we don’t think that it is likely that EMs outperform with the U.S. struggling, it is encouraging to see better performance to start the year.

Market Performance

Fixed Income

- Treasury and sovereign bond yields across the globe surged higher in January leading to a challenging month for core fixed income.

- Credit held up fairly well considering the carnage in riskier assets.

- Bank loans provided a nice hedge against rising rates.

U.S. Equities

- For the first time in a while, U.S. equities lagged non-U.S. equities in January.

- Value trounced growth and large caps

- outperformed small caps.

- Most of the selling was in the tech- heavy Nasdaq.

Non-U.S. Equities

- Non-U.S. equities softened towards the end of the month despite providing relative outperformance versus the U.S.

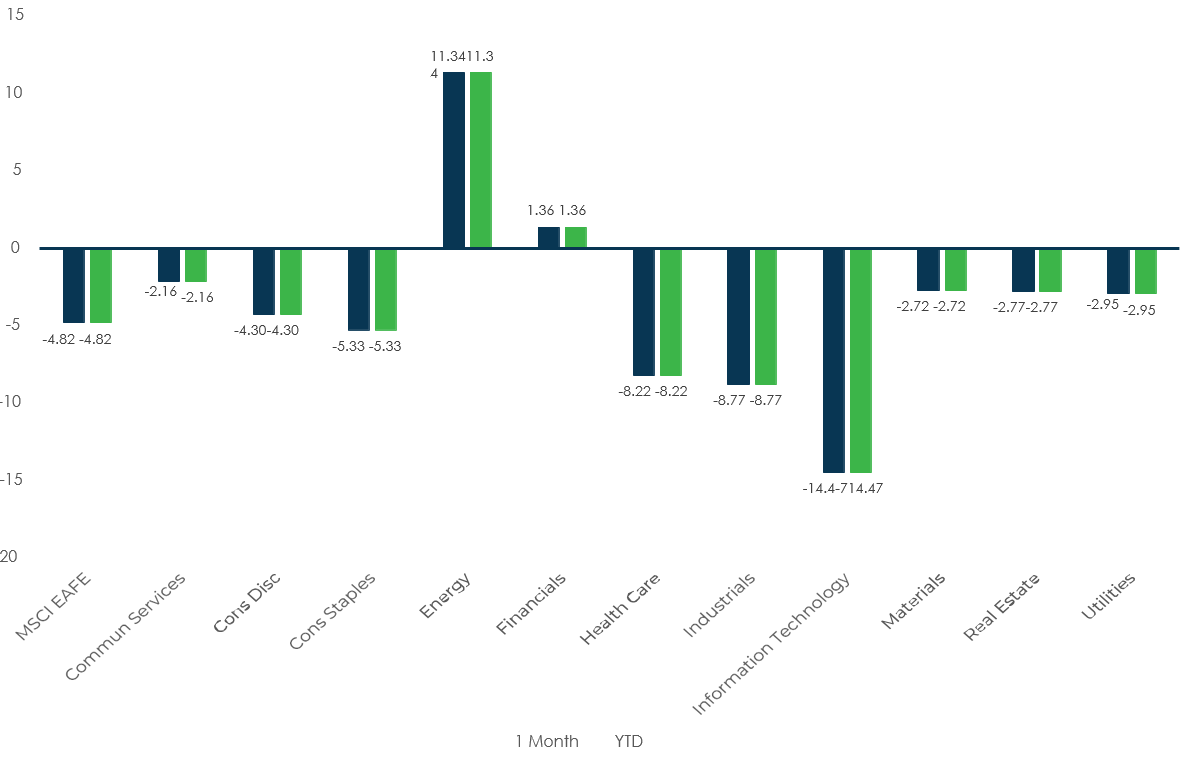

- EAFE markets tend to be value driven so that explains a lot of the relative outperformance.

- Similar to the U.S., growth trailed value and small caps lagged large caps.

- EMs fell only 1.9%, largely due to relative outperformance from China and Brazil.

- The stronger USD hurt returns.

Sector Performance – S&P 500 (as of 1/31/22)

Sector Performance – Russell 2000 (as of 1/31/22)

Source: MSCI

Sector Performance – MSCI EM (as of 1/31/22)