Market Flash Report | October 2021

Economic Highlights

United States

- The U.S. economy grew at a 2% rate in the third quarter, its slowest gain of the pandemic-era recovery, as supply chain issues and a marked deceleration in consumer spending stunted the expansion. Economists were expecting a downwardly revised reading of 2.8% growth during Q3. Consumer spending, which makes up 69% of the $23.2T U.S. economy, increased at just a 1.6% clip in Q3 after rising 12% in Q2. Spending for goods tumbled 9.2%, spurred by a 26.2% plunge in expenditures on longer-lasting goods like appliances and autos, while services spending increased 7.9%, a reduction from the 11.5% pace in Q2. Federal government spending fell by 4.7%, due largely to a halt in services and processing for the SBA Paycheck Protection Program.

- Core personal consumption expenditures (PCE), which exclude food and energy and are the preferred gauge by which the Federal Reserve measures inflation, rose 4.5%, a deceleration from Q2’s 6.1% increase but still well above the pre-Covid-19 pace. The headline PCE price index increased 5.3% in Q3, down from 6.5% in the previous period. The latest CPI reading showed an increase of 5.4% Y/Y at the headline level and 4% when excluding volatile food and energy. While average hourly earnings are growing at a 4.6% annualized rate, they still trail the pace of inflation.

- Manufacturing activity in the U.S. slowed a bit in October. The ISM Manufacturing Index fell from 61.1 in September to 60.8 in October. New orders and production softened last month while employment and prices gained ground. Survey respondents continue to state that demand is robust, but supply chain issues are increasingly impacting businesses. The latest service sector reading was the September ISM report that pinned service sector activity at 61.9. Within the service sector, business activity and new orders remain at very strong levels.

Non-U.S. Developed

- Eurozone business activity growth slowed sharply to a six-month low in October amid increasing supply bottlenecks and ongoing COVID-19 concerns, dropping most markedly in manufacturing though also cooling in services. Survey-record price increases were meanwhile reported as firms sought to pass an unprecedented rise in costs on to customers. The ISM Composite PMI fell from 56.2 in September to 54.3 in October with manufacturing activity hitting a 16-month low. By all accounts, the eurozone economy entered Q4 on weak footing after rebounding earlier in 2021. We believe that risk is to the downside within the eurozone economy and this trend of underperforming expectations should continue.

- The Bank of Japan (BOJ) recently trimmed its estimates for economic growth. The Japanese central bank said the economy will likely grow 3.4%, rather than the 3.8% projected in its previous policy-setting meeting in July. Core consumer prices excluding volatile fresh food are forecast to stay at 0.0%, lower than the earlier projection of a 0.6% increase. A major difference versus other developed economies is the lack of persistent inflation. Japan’s central bank indicated it will continue with its ultra-accommodative monetary policy. The BOJ kept its "yield curve" control program to set short-term interest rates at minus 0.1% and guide 10-year Japanese government bond yields around 0% to keep borrowing costs low for companies and households. The BOJ will continue to purchase ETFs and has upgraded its 2022 GDP growth forecast slightly.

Emerging Markets

- The Chinese economy expanded 4.9% year-on-year in the third quarter of 2021, easing sharply from a 7.9% growth in the previous period and slightly missing market consensus of 5.2%. It was the slowest pace of expansion since the third quarter of 2020, amid several headwinds including power shortages, supply chain bottlenecks, a persistent property bubble and COVID-19 outbreaks. Considering the first three quarters of the year, the economy grew 9.8% from a year earlier, with final consumption accounting for 64.8% of GDP growth. For 2021, China has set an economic growth target of above 6% after growing the least in over four decades in 2020.

- China’s official manufacturing PMI fell from 49.6 in September to 49.2 in October, a big decline from the economic recovery experienced during the early days of the pandemic. Manufacturing activity has been hit hard by rising raw material prices and softer domestic demand. The official service sector PMI also fell last month from 53.2 in September to 52.4 in October. Rolling COVID-19 outbreaks across the country have impacted consumer demand over the past few months and this could continue moving forward. Within manufacturing, the price component rose to its highest level on record while the production component fell to its lowest level since inception.

- Chinese inflation hit a 6-month low in October while retail sales rebounded 4.4% in September (above expectations).

- Brazil’s GDP shrank 0.1% Q/Q during Q2 2021, ending three straight quarters of expansion and missing market expectations of 0.2% growth. The agricultural and industrial sectors were the main drivers of the contraction, falling 2.8% and 0.2% respectively. On a yearly basis, the economy grew by 12.4%, the most on record but below expectations of 12.8%. For Q3, Brazil’s economy is projected to increase 0.3% Q/Q.

- India’s economy grew 20.1% Y/Y during Q2, ahead of the 19% expectation. Private expenditure increased 19.3%, investment 55.3%,

- exports 39.1% and imports 60.2% while public expenditure dropped 4.8%. For Q3, India’s economy is forecast to grow 12%.

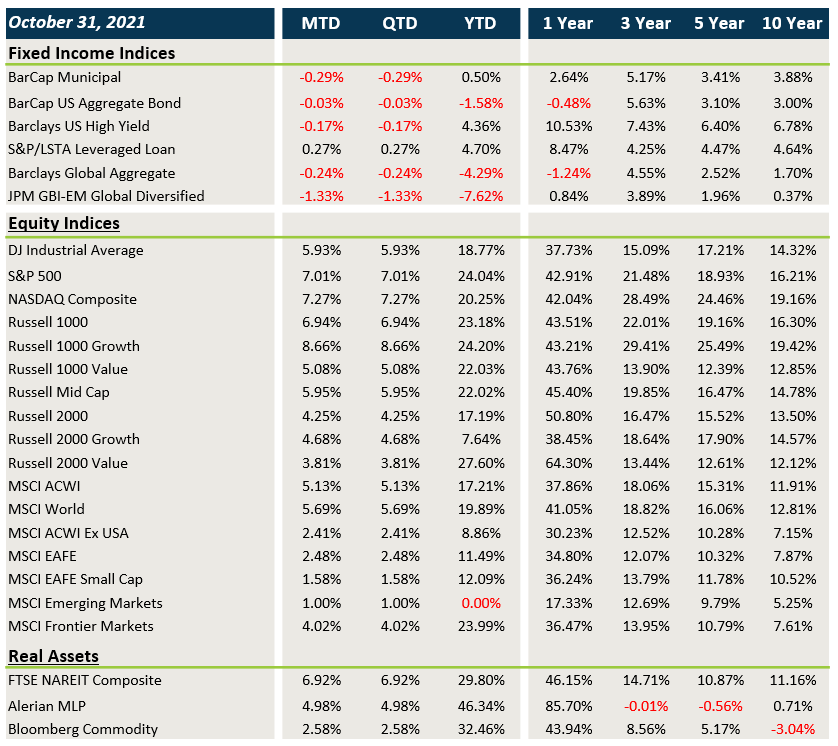

Market Performance (as of 10/31/21)

Fixed Income

- Treasury yields were fairly range-bound in October and this led to slight losses in core fixed income and munis.

- Credit spreads widened last month and the sharp move higher in sovereign debt yields created losses in non-U.S. fixed income.

U.S. Equities

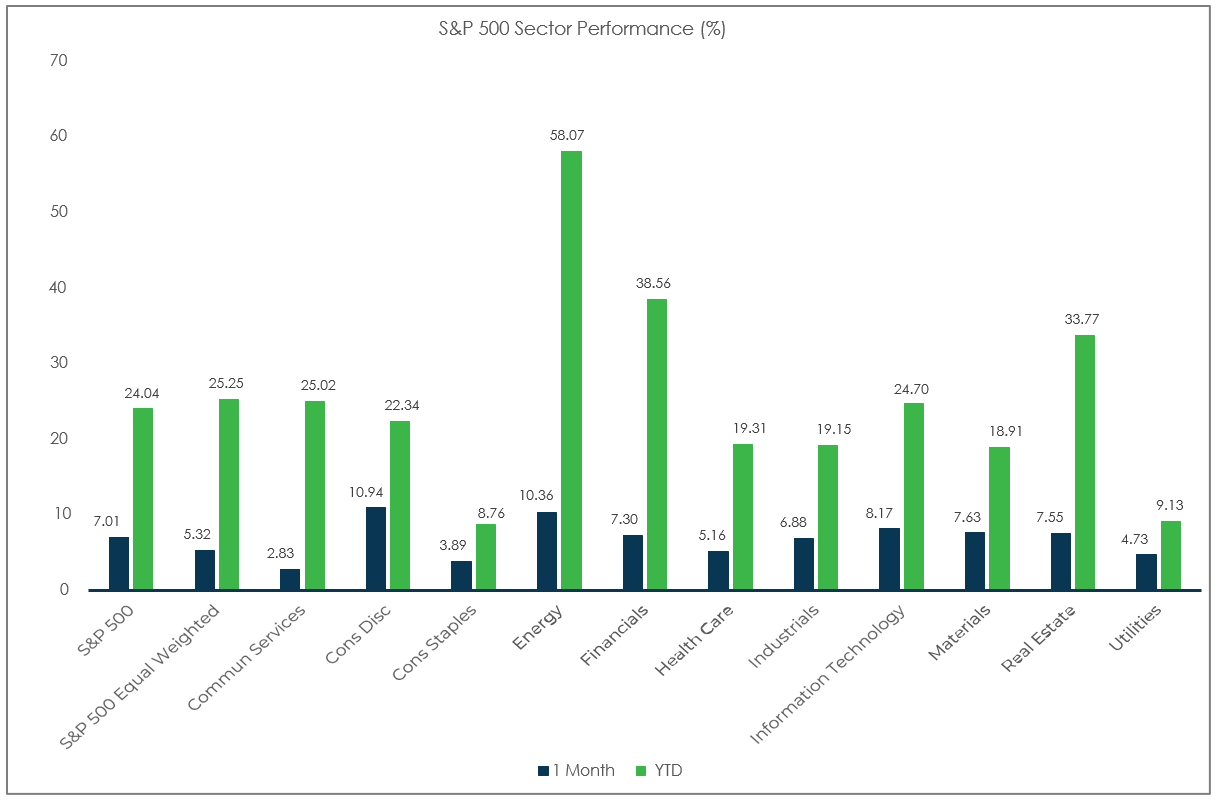

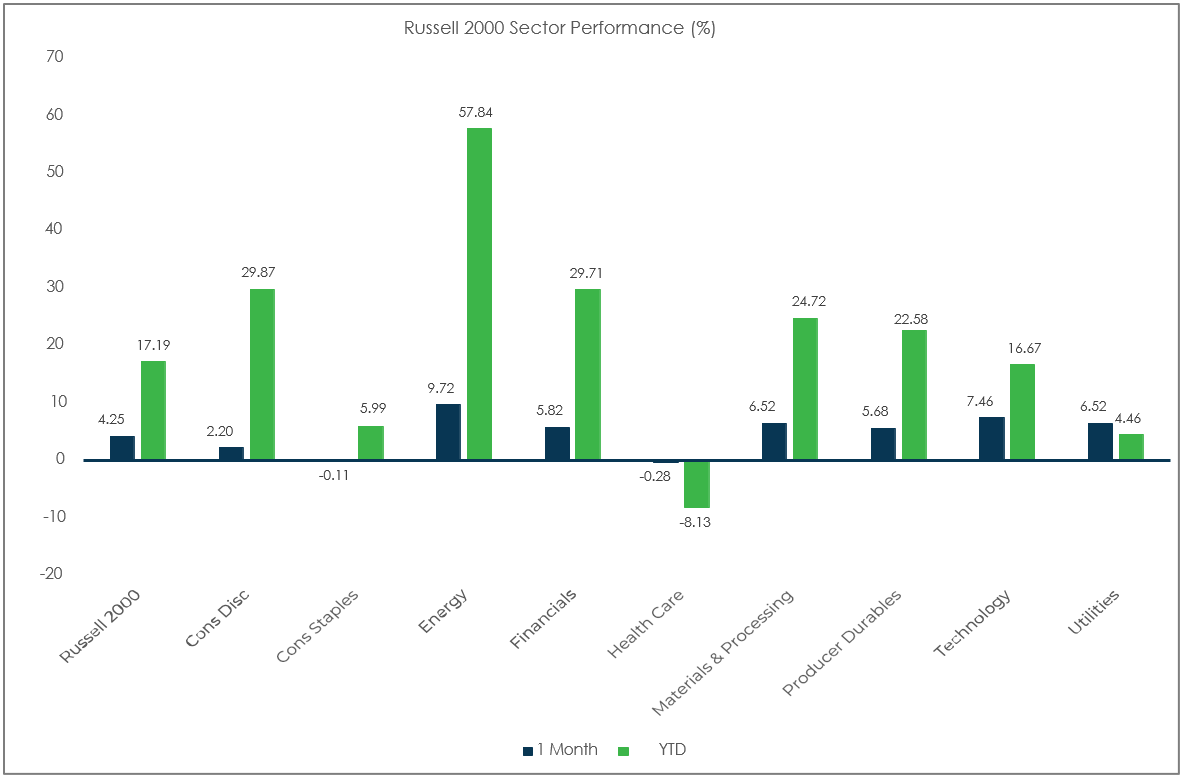

- U.S. equities rebounded sharply in October after exhibiting weakness during the previous month.

- Large cap stocks outperformed small caps, and growth surged past value in October.

- The tech-heavy Nasdaq was the best performing benchmark in October.

Non-U.S. Equities

- Non-U.S. equities significantly lagged

- U.S. equities last month with particular weakness from Japan.

- Similar to what occurred in the U.S., growth beat value and large caps outperformed small caps.

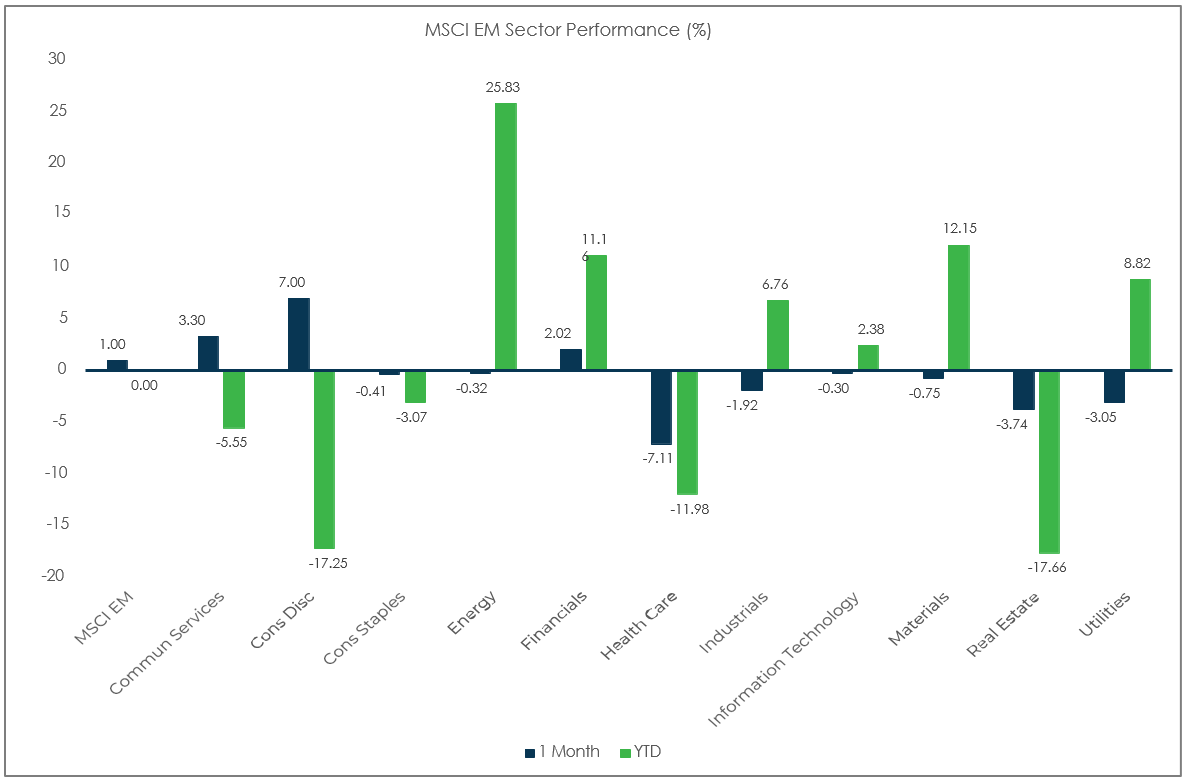

- EM equities gained 1% in October, driven by a rebound in Chinese equities. Latin America was a weak spot last month.

- The weaker USD added 27 bps to MSCI EAFE returns and 9 bps to MSCI EM returns.

Sector Performance – S&P 500 (as of 10/31/21)

Sector Performance – Russell 2000 (as of 10/31/21)

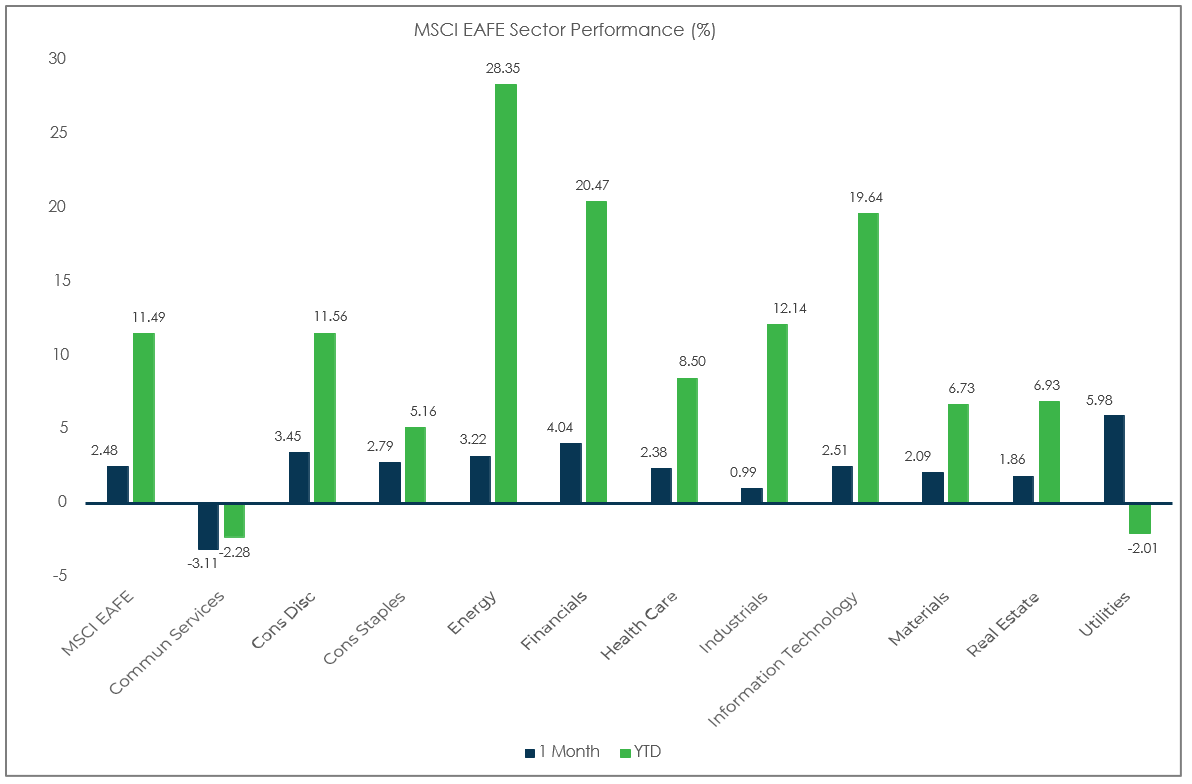

Sector Performance – MSCI EAFE (as of 10/31/21)

Sector Performance – MSCI EM (as of 10/31/21)