To provide economic stimulus and support as a result of the coronavirus pandemic, Congress recently passed the Coronavirus Aid, Relief and Economic Security Act of 2020 (“CARES Act”). There are important provisions in this legislation that offer financial assistance to people facing COVID-19 related economic hardship.

Retirement Account Withdrawal Penalty Temporarily Waived

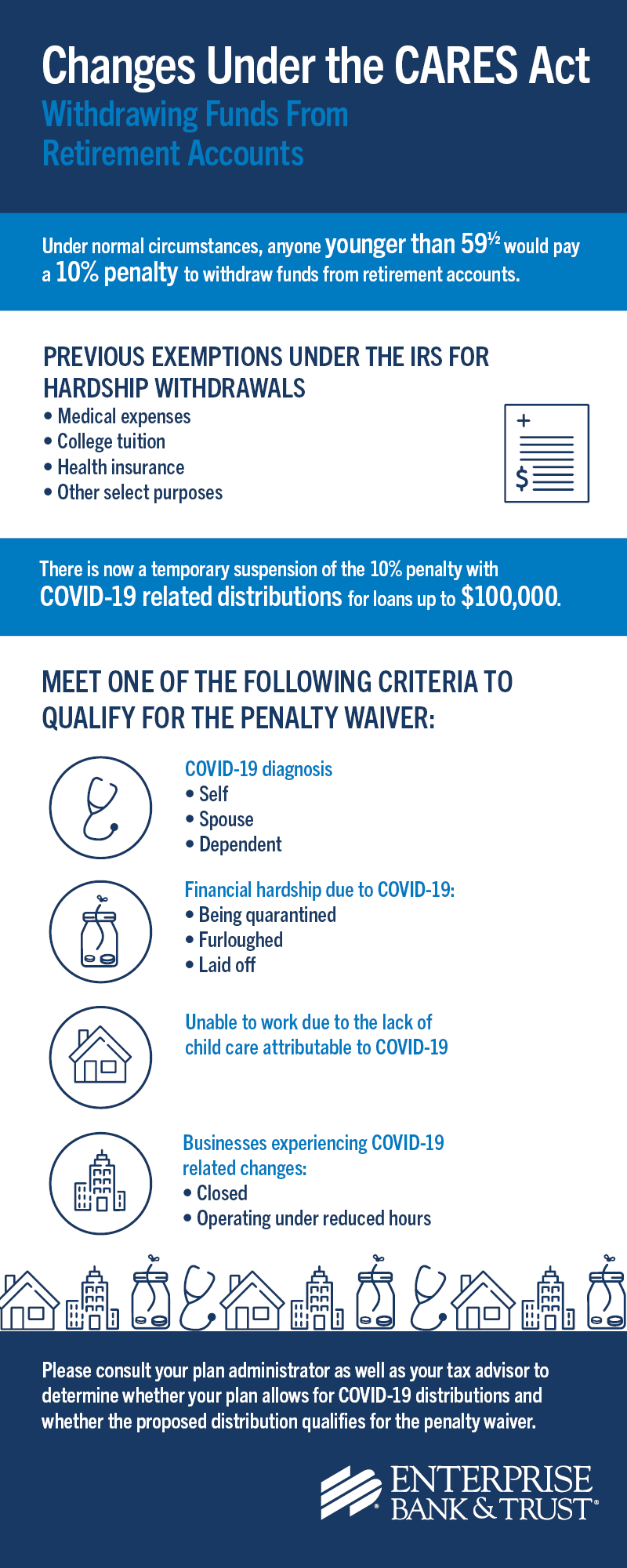

The CARES Act enables persons younger than age 59½ to make COVID-19 related withdrawals of up to $100,000 from their retirement accounts without paying a penalty. Previously, persons below this age paid a 10% penalty for most distributions in addition to tax owed.

Under the CARES Act, persons younger than 59½ must meet one of the following criteria to qualify:

- Diagnosed with COVID-19.

- Have a spouse or dependent diagnosed with COVID-19.

- Experience financial hardship as a result of being quarantined, furloughed or laid off due to the COVID-19.

- Inability to work due to the lack of child care attributable to COVID-19.

- Business owner who operated their business under reduced hours or closed due to COVID-19.

Income Tax Withholding for Retirement Accounts Withdrawals Suspended

In addition to the 10% penalty, persons taking early withdrawals from their employer’s retirement plan have historically been subject to a mandatory 20% income tax withholding at the time of distribution. Under the CARES Act, withholdings for COVID-19 related employer plan distributions have been suspended until the end of the year.

People seeking to make withdrawals from employer-sponsored retirement accounts received yet another helping hand from this bill. Although the 20% withholding was waived, income tax on such distributions must still be paid. Normally, income arising from retirement account distributions must be recognized and thus taxed in the year of withdrawal. The CARES Act modifies this and enables income from the withdrawal to be spread evenly over 2020, 2021 and 2022, thus spreading the tax liability over a three year period.

While spreading the tax liability over several years will be beneficial to some, there may be circumstances when recognizing all withdrawal income in 2020 could be beneficial. Consult your financial advisor for guidance on the best option for your circumstances.

Returning Prior Withdrawals to Retirement Accounts to Avoid Taxes

The CARES Act also provides ways for people who took a retirement account distribution in 2020 to return the withdrawals and avoid paying income tax on these distributions. There are two options.

- If the distribution was taken within the last 60 days, a 60-day rollover can be executed and the funds returned to the retirement plan. This opportunity is not available, however, if another rollover has been completed within the last 365 days.

- A second option allows qualifying distributions from retirement accounts to be repaid in a lump sum or in contributions spaced over a three-year period ending in 2022. Spreading repayment of the withdrawal over several years could be very helpful to those struggling to replace income lost during the coronavirus crisis. (Note: Distinguishing the repayment to the retirement account from new contributions will be subject to guidance and/or regulations yet to be issued by the Internal Revenue Service.)

It is important to note that the above options for the 60-day rollover and repayment of the distribution over a three-year period are not available to individuals who are not the account owner, such as in cases of an inheritance.

Loans from Employer Retirement Plans

Many employer-sponsored retirement plans permit loans to plan participants. Prior to the CARES Act, the maximum loan amount permitted was the lesser of 50% of the employee’s plan balance, or $50,000. The CARES Act increases the loan amount to $100,000 and permits the plan administrator to loan up to the entire balance of the participant’s plan balance. Repayment of loans from the plan made through December 31, 2020, can be delayed for up to one year.

Enterprise Bank & Trust – Your Partner During Uncertain Times

The CARES Act of 2020 provides many employees and retirement account owners with several less restrictive ways to access cash in their retirement accounts. Before making a retirement account withdrawal, consult your plan administrator and your tax advisor to ensure you qualify.

Follow this blog and our social media accounts for more information about managing through the COVID-19 crisis.