Capital Markets Playbook | Q2 2026

2026 Q1 Summary

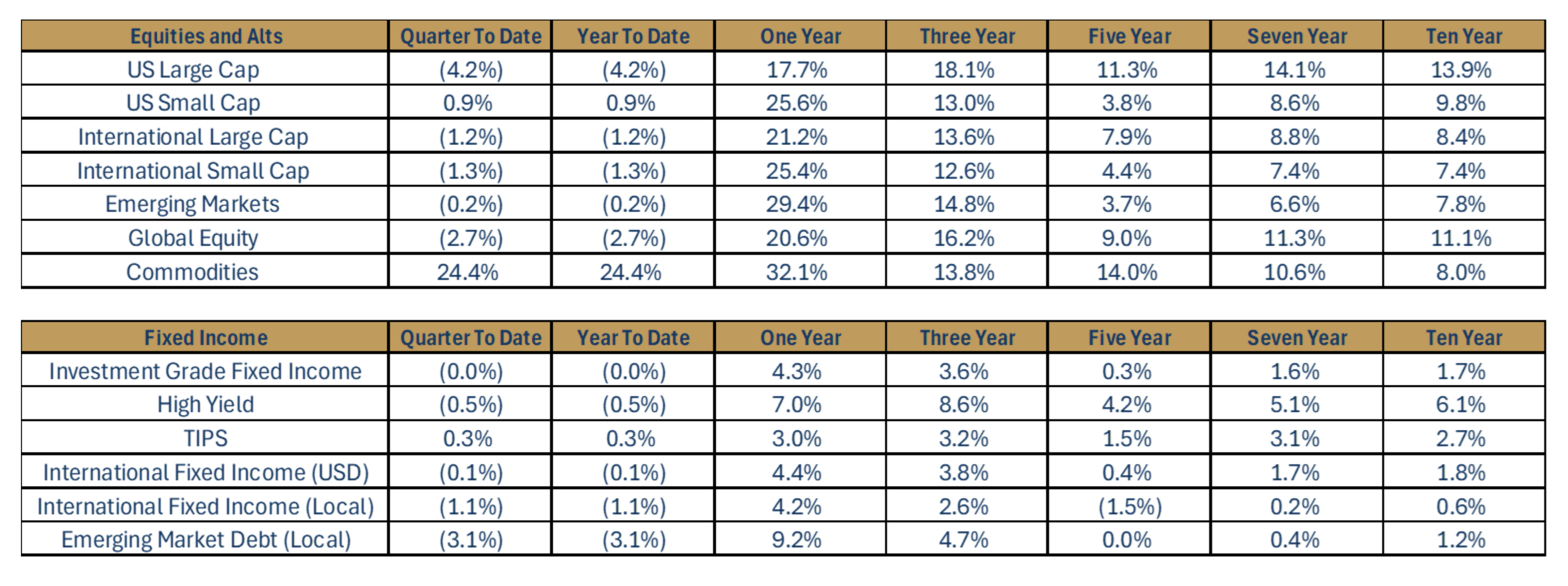

- Equity and fixed income markets gains from the first two months of 2026 were erased in March.

- The uncertainty associated with the conflict in the Middle East resulted in elevated volatility in both equity and fixed income markets.

- Global equity declined by close to 3% in Q1.

- U.S. large cap stocks, down 4.2% in Q1, underperformed all major equity asset classes.

- U.S. small cap stocks, the only major equity asset class that saw a gain in Q1, were up 0.9%.

- Commodities (+24.4%), by far the strongest-performing “risky” asset class in Q1, posted outsized gains due to energy supply chain disruptions arising from the conflict in the Middle East.

- Broad-based fixed income markets were largely flat in Q1.

- Investment Grade Fixed Income was unchanged in Q1.

- Riskier fixed income asset classes (ex: high yield, EM debt) underperformed more conservative fixed income asset classes as credit risk concerns mounted in Q1.

2026 Q1: In Review

- U.S. Macroeconomic Review

- Economic growth for 2025 was published in Q1 2026. The U.S. economy grew 2.1% in 2025 despite uncertainty around tariffs, sticky inflation and an uptick in unemployment.

- Economic growth for Q1 of 2026 may come in north of 2% due to ongoing strength in consumer spending.

- Unemployment, currently 4.3%, remained largely unchanged in Q1.

- The Federal Reserve’s preferred measure of inflation, the Personal Consumption Expenditures (PCE) Index, ticked slightly higher in Q1 and is currently 80bps above the Fed’s 2% inflation target.

- The Fed held its short-term policy rate steady at 3.5-3.75% in Q1. The Fed plans to keep monetary policy unchanged until there is more certainty with the conflict in the Middle East.

- Equity Market Review

- Equity market volatility spiked in the quarter due to the conflict in the Middle East.

- Broad-based equity markets finished the quarter down approximately -2.7%.

- Growth stocks underperformed value stocks, which finished the quarter in positive territory.

- U.S. small caps led all major equity asset classes and were the only equity asset class to report positive performance.

- Fixed Income Market Review

- Treasury yields moved higher in Q1 (ex: 10-Year Treasury Yield increased 20bps) as investors repriced inflation expectations and global risk.

- Credit spreads widened as investors repriced credit risk within less conservative fixed income asset classes (ex: high yield).

- TIPS outperformed all fixed income asset classes as inflation expectations increased slightly.

A Summary of Recent Market Events

- Volatility in global capital markets spiked in March, following escalating tensions and attacks between Iran and the U.S. Wall Street’s often-cited volatility index (“VIX”) peaked in March to levels more than double the index reading in the months prior. U.S. equity markets have sold off and U.S. Treasury yields have increased in the days since the conflict started. The S&P 500 declined approximately 9% from highs at the start of the year. Treasury yields across the curve have increased on both reduced expectations of the Fed cutting rates this year as well as heightened inflation expectations.

- It is uncertain how long the conflict will last. The possibility of sustained instability cannot be entirely ruled out.

- Market participants are paying close attention to the price of energy due to the possibility of prolonged energy supply chain disruptions. A key shipping route (Strait of Hormuz) has been largely impassable since the start of the conflict due to security and safety related issues. This has resulted in a disruption of approximately 20% of the global oil movement. The longer that key shipping routes remain impassable, the more likely it is that energy supply shortages will put upward pressure on global energy prices.

- Long-lasting energy shortages would likely result in higher inflation over time, but it is important to remember that energy prices are far less impactful to inflation compared to other variables, like wage growth.

- A short-lived energy shortage will have little impact on the U.S. economy for the full calendar year. It is important to remember that the U.S. has been a net exporter of energy for five years and has become more energy-independent. As such, the U.S. is less vulnerable to the risk of high energy prices than most countries across the globe.

- It is too early to determine how the Fed’s monetary policy will be impacted by the turmoil overseas. That said, the Fed has recently communicated to the market that short-term interest rates will likely remain at current levels for now. We do not expect that the current situation will change that assessment. It is also important to remember the Fed’s focus when setting monetary policy is on core inflation – a reading that excludes food and energy.

- A two-week ceasefire was announced between the U.S., Israel and Iran on April 7. This ceasefire, however, does not guarantee an end to the conflict. As such, investors should expect market volatility to remain higher than normal until there is a better understanding of when the conflict may end and when energy shipping can return to normal.

2026: Expectations for the Year Ahead

- 2026 U.S. Macroeconomic Preview

- Expected Case

- Economic growth in the U.S. is expected to be slightly higher than the long-term trend rate of (2.0%) in 2026.

- Consumer spending is expected to moderate and come in slightly below the long-term growth rate of 2.5%.

- Unemployment, currently at 4.3%, is expected to remain stable through the end of 2026.

- Wage growth is expected to continue moderating in 2026 and near its long-term growth rate (3.5-4.0%).

- Inflation is expected to increase in the first half of 2026 before declining in the second half of the year.

- PCE inflation, the Fed’s preferred measure of inflation, is expected to decrease to 2.5% by year-end 2026.

- The Fed may not change its short-term policy rate in 2026. And while it is more likely that the Fed will cut rates the next time it adjusts its short-term policy rate, a rate hike cannot be entirely ruled out, given the potential for sustained energy supply disruptions in the Middle East.

- Expected Case

- 2026 Equity Market Preview

- Expected Case

- Equity markets will continue to be more volatile than normal until there is more certainty with how the conflict in the Middle East will end.

- Corporate earnings are expected to be strong in 2026. Corporate earnings in 2026 are expected to outpace solid corporate earnings in 2025.

- AI-related investments will likely remain a key driver of performance. A broadening of earnings growth beyond the mega-cap tech sector is expected across multiple asset classes and areas of the market.

- Expected Case

- 2026 Fixed Income Preview

- Expected Case

- Short-term interest rates, which are driven by the Fed’s monetary policy, are unlikely to move meaningfully lower unless the Fed cuts rates.

- Intermediate and long-term interest rates, which are not significantly influenced by the Fed’s monetary policy, may prove to be volatile in the months and quarters ahead, as markets weigh concerns over U.S. debt, deficits and sticky inflation.

- Expected Case

Risks to the “Expected Case” in 2026

- Elevated Asset Class Valuations

- Equities and real estate make up a significant percentage of households’ total net worth. Equities and homes had significant price gains for the past five years, which has led to fairly expensive valuations. A reduction in asset values would likely lead to slower spending growth, weaker labor markets and slower economic growth.

- Concerns of private credit valuations have increased. It is important to remember that private credit makes up less than 2% of U.S. investment assets. Associated risks with this asset class seem manageable and concentrated within specific firms. Default rates remain contained, and there are no broad warnings signs around credit quality. However, a surge in redemption requests may prove contagious even when many borrowers are making timely payments.

- Unexpected Labor Market Weakness

- An unexpected softening of the labor market would create headwinds to consumer spending and lead to slower economic growth.

- Unexpected labor market weakness may create a more acute “affordability crisis” for low- and middle-income households.

- An Unexpected Pickup in Inflation

- Tariffs on imported goods could push inflation higher than expected, as its impact is still working its way into the economy.

- More aggressive and accommodative fiscal and monetary policy intervention may increase inflation and inflation expectations in the U.S.

- Rising energy prices have historically pressured headline inflation. If the conflict in the Middle East escalates further or if oil supply remains disrupted for an extended period, inflation expectations may rise further.

- Mounting Concerns Over U.S. Debt and Deficits

- Mounting concerns over U.S. debt and deficits could lead to higher long-term interest rates.

- Unexpected Geopolitical Issues and Midterm Elections

- Unexpected geopolitical events can significantly influence financial markets over short periods of time.

- Uncertainty associated with U.S. foreign policy could have negative impacts on market volatility, global trade flows and the global economy.

- The lead up to midterm elections in the U.S. could create news that negatively impacts market volatility over the short term.

- The “Unknown Unknowns”

- The most threatening risks to the “expected case” are always those that catch markets by surprise. The most recent examples of exogenous shocks are the emergence of COVID-19 in late 2019/early 2020 and the tariff announcements in early 2025.

2026 Expectations: Economic Growth

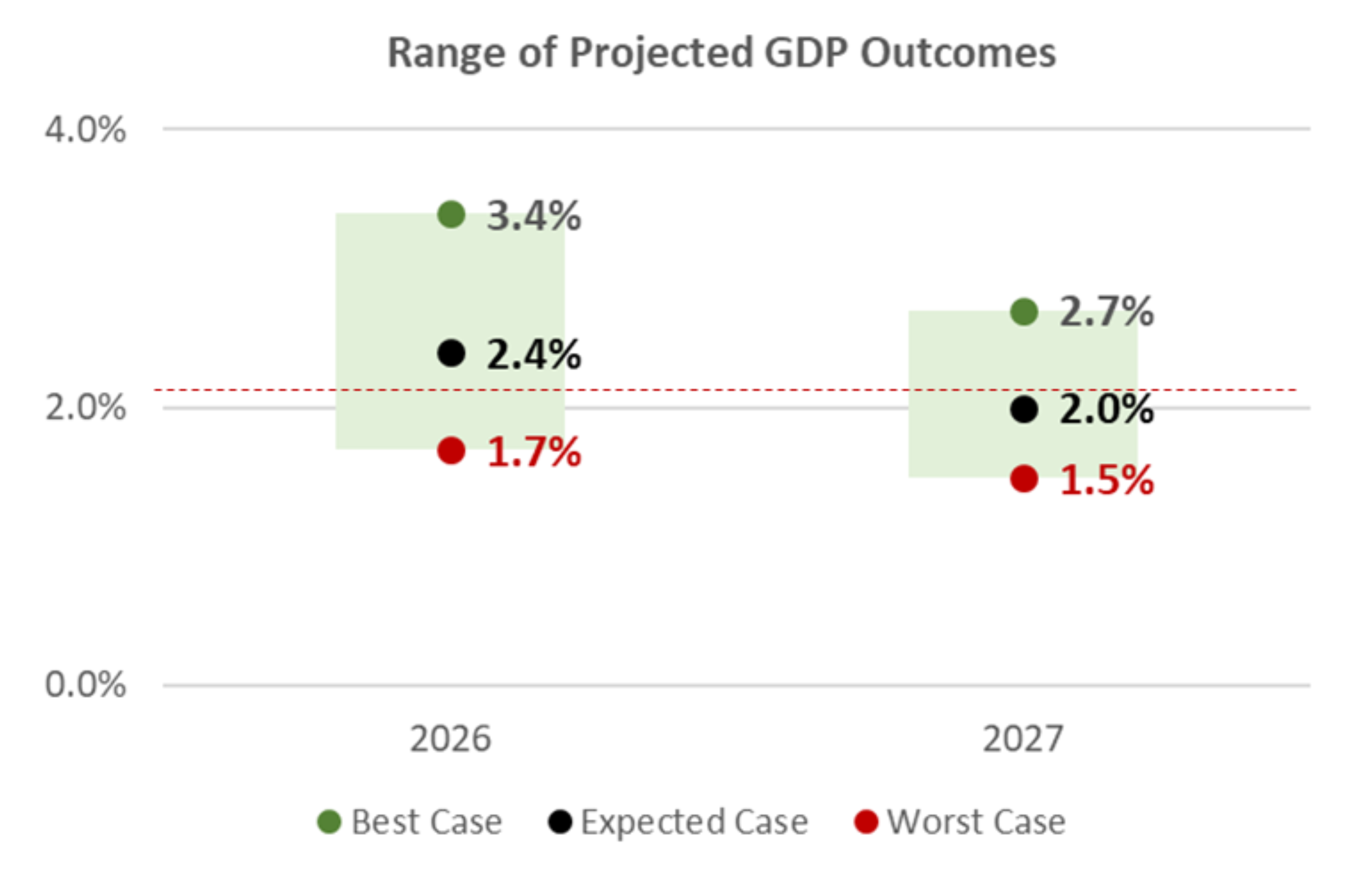

- U.S. economic growth is expected to continue its current growth path, remaining at or above trend levels through 2027.

- Unemployment is expected to remain stable and consumer spending is expected to remain fairly strong in 2026.

- While the probability of an economic contraction in the U.S. may be higher today due to energy related supply disruptions overseas, the expectation for continued strength in consumer spending implies a low recession risk in 2026.

- Scenarios

- Best Case

- Economic activity in the U.S. will come in well above its long-term trend rate over the next two years.

- Expected Case

- Economic activity in the U.S. is near its long-term growth rate over the next two years.

- Worst Case

- Economic activity is well below its long-term trend rate over the next two years.

- Best Case

2026 Expectations: Unemployment

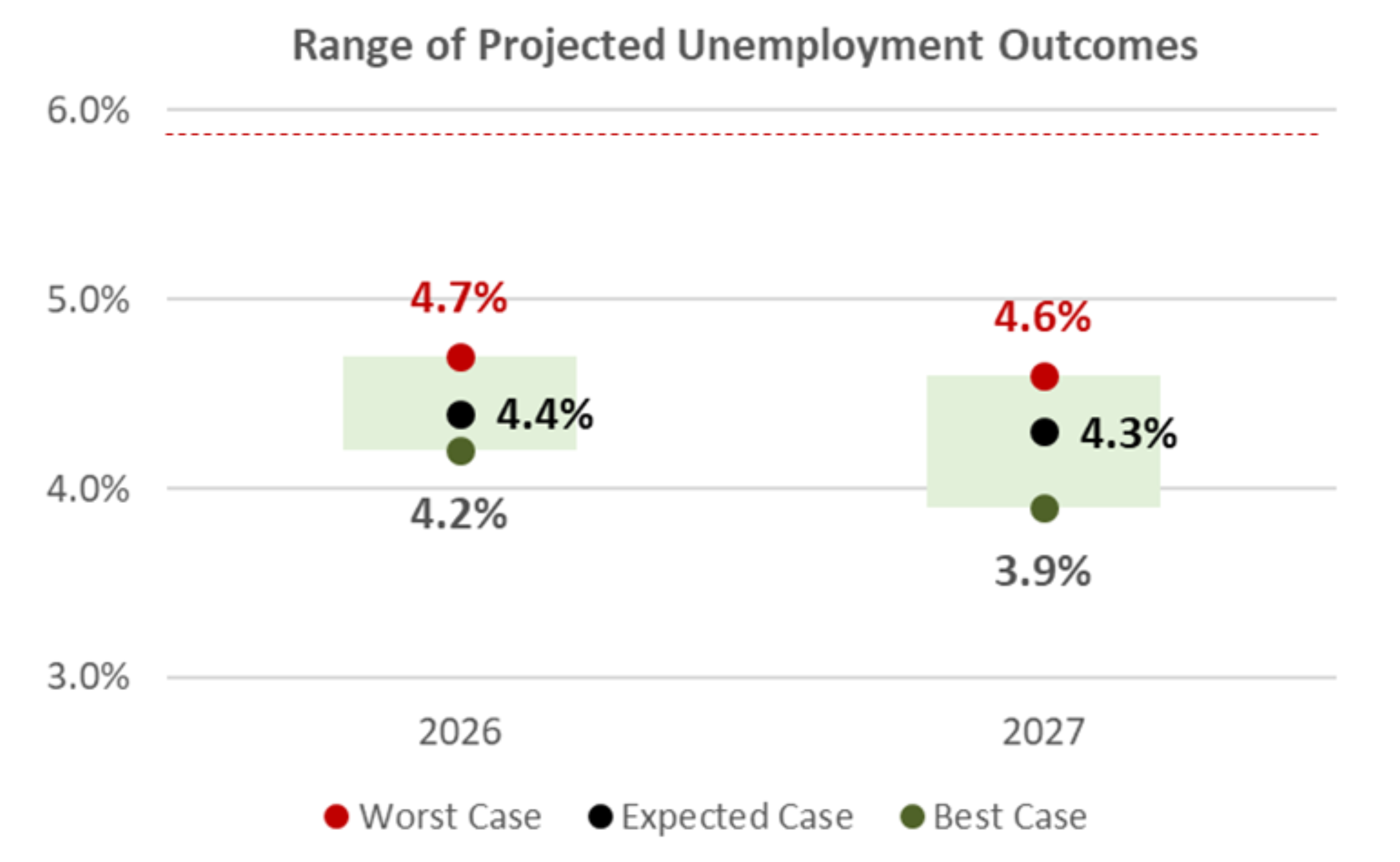

- Unemployment in the U.S. has been range bound at 4.3% and is expected to remain well below its long-term average through the end of 2026.

- The overall U.S. labor market remains strong, despite weakness in select industries.

- Labor markets continue to normalize as both hire rates and layoff rates trended lower in 2025. This trend is expected to continue through 2026. Unfilled job openings are back to pre-pandemic levels.

- While few expect unemployment to increase meaningfully in 2026, the risk of a meaningful spike in unemployment cannot be ruled out.

- Scenarios

- Best Case

- Unemployment declines from its current level and remains near historical lows over the next two years.

- Expected Case

- Unemployment remains near current levels as the U.S. economy grows and remains well below its longer-term trend rate.

- Worst Case

- Unemployment rises slightly through the end of 2027 as a result of meaningfully slower economic growth.

- Best Case

2026 Expectations: Inflation

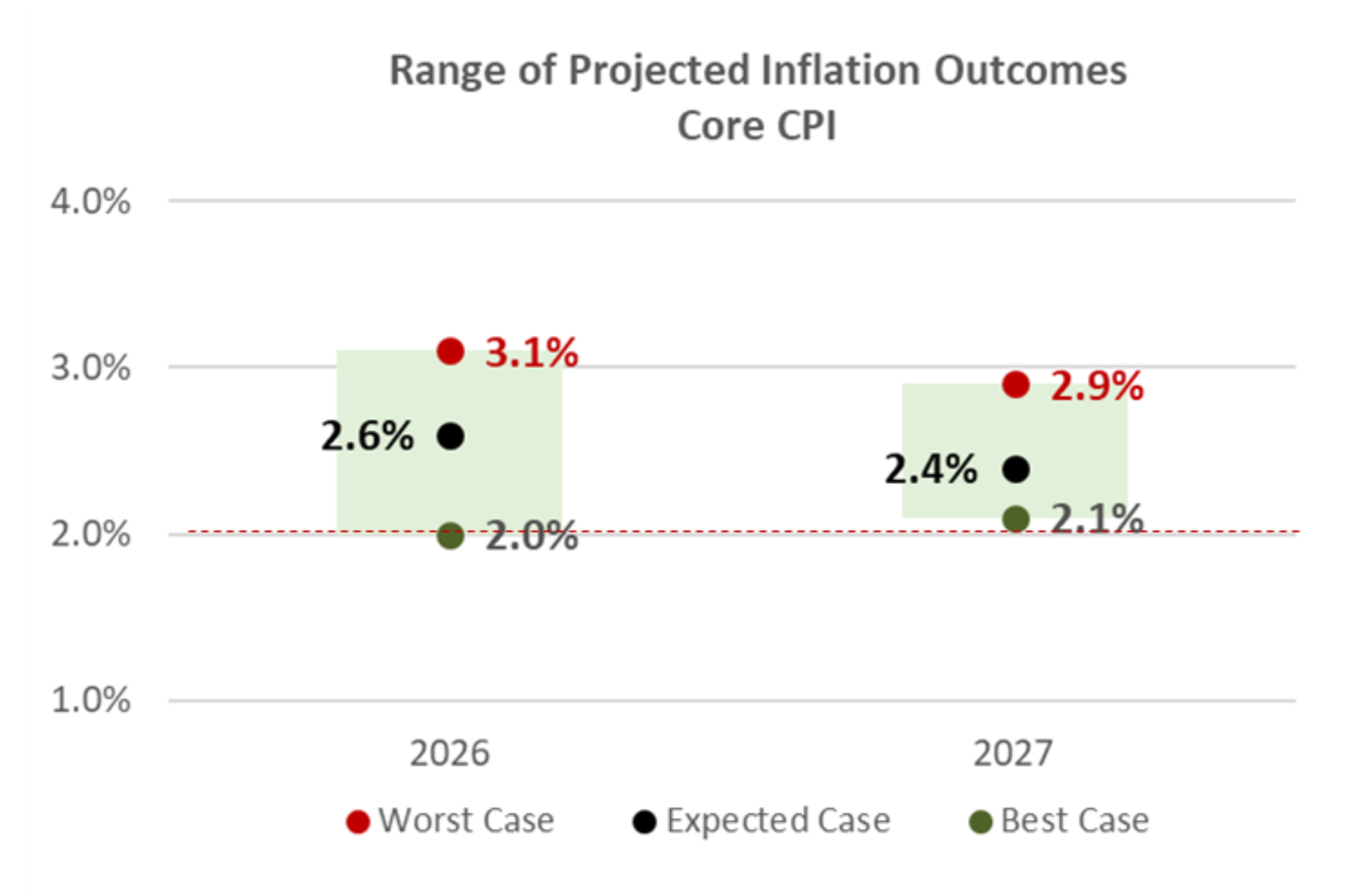

- Inflation is expected to decline in 2026 but remain above the Fed’s 2.0% inflation target for the full calendar year.

- Inflation is expected to increase in the first half of 2026 due to tariffs and higher energy prices, before falling to around 2.6% by the end of the year.

- Scenarios

- Best Case

- Inflation declines to the Fed’s long-term inflation target of 2% by the end of 2026.

- Expected Case

- Inflation continues to moderate very slowly and is about 0.5% higher than the Fed’s long-term inflation target by the end of 2026.

- Worst Case

- Inflation continues to be sticky throughout the aggregate economy and is approximately 1% higher than the Fed’s long-term inflation target through the end of 2026.

- Best Case

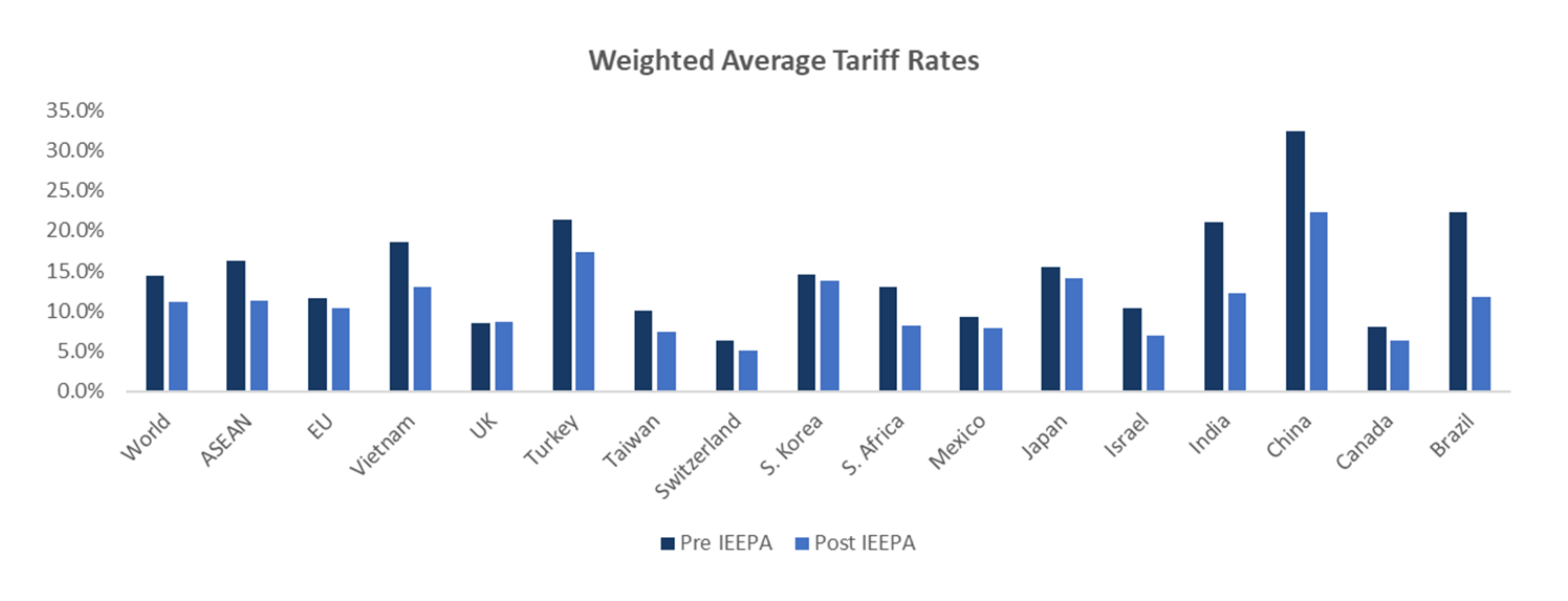

2026 in Focus: Tariffs

- On February 12, 2026, the U.S. Supreme Court struck down the IEEPA U.S. tariffs applied by the administration last year.

- In response to the cancellation of the IEEPA tariffs, the administration imposed a new global tariff of 10%. Under Section 122 of the Trade Act, these tariffs are “non-discriminatory,” meaning the 10% applies equally to all countries.

- The biggest declines in post-ruling tariff rates apply mainly to China, India and Brazil. However, tariff rates declined broadly across most trade partners. It is unknown if the administration will take further action to make up for the shortfall for tariff revenues following the cancellation of the IEEPA tariffs.

- U.S. firms may pass along higher tariff costs to consumers in 2026 that they were previously absorbing.

- Takeaway

- Following the Supreme Court ruling, trade policy for 2026 is in an unknown state. Any of the other options available to the administration lack the flexibility of the IEEPA tariffs. As of now, the decline in the average tariff rate means the impact of tariffs may soften.

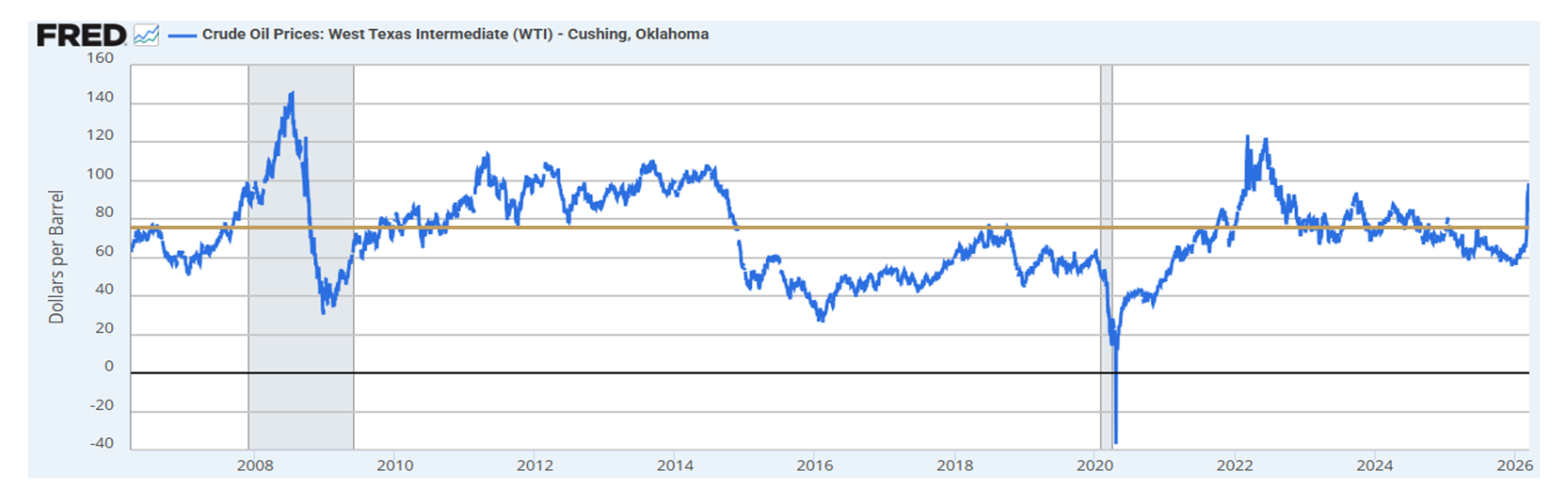

2026 in Focus: Geopolitical Implications

- The conflict in the Middle East has led to increased market volatility across global capital markets.

- The largest disruption has been centered around the energy market and transportation through the Strait of Hormuz.

- About 20% of the world’s oil shipments and more than 25% of globally traded liquified natural gas pass through the corridor.

- Energy shipping came to a stand still in March as the conflict in the Middle East intensified. Oil and natural gas prices spiked as energy supplies became dearer.

- Higher energy prices for a prolonged period of time can contribute to inflation. Higher inflation not only potentially handicaps the Fed’s ability to cut interest rates, but as higher prices flow through the economy and have a greater impact on consumer spending, decreases in global GDP growth rates would likely begin to materialize as well.

- Security price fluctuations fueled by uncertainty and developing headlines surrounding the situation can make it tempting for investors to react on impulse, but it is important to remain focused and not allow near-term market swings to alter your long-term outlook.

- Using history as a guide, regional wars and geopolitical shocks often trigger sharp market responses, but they are usually short lived in nature.

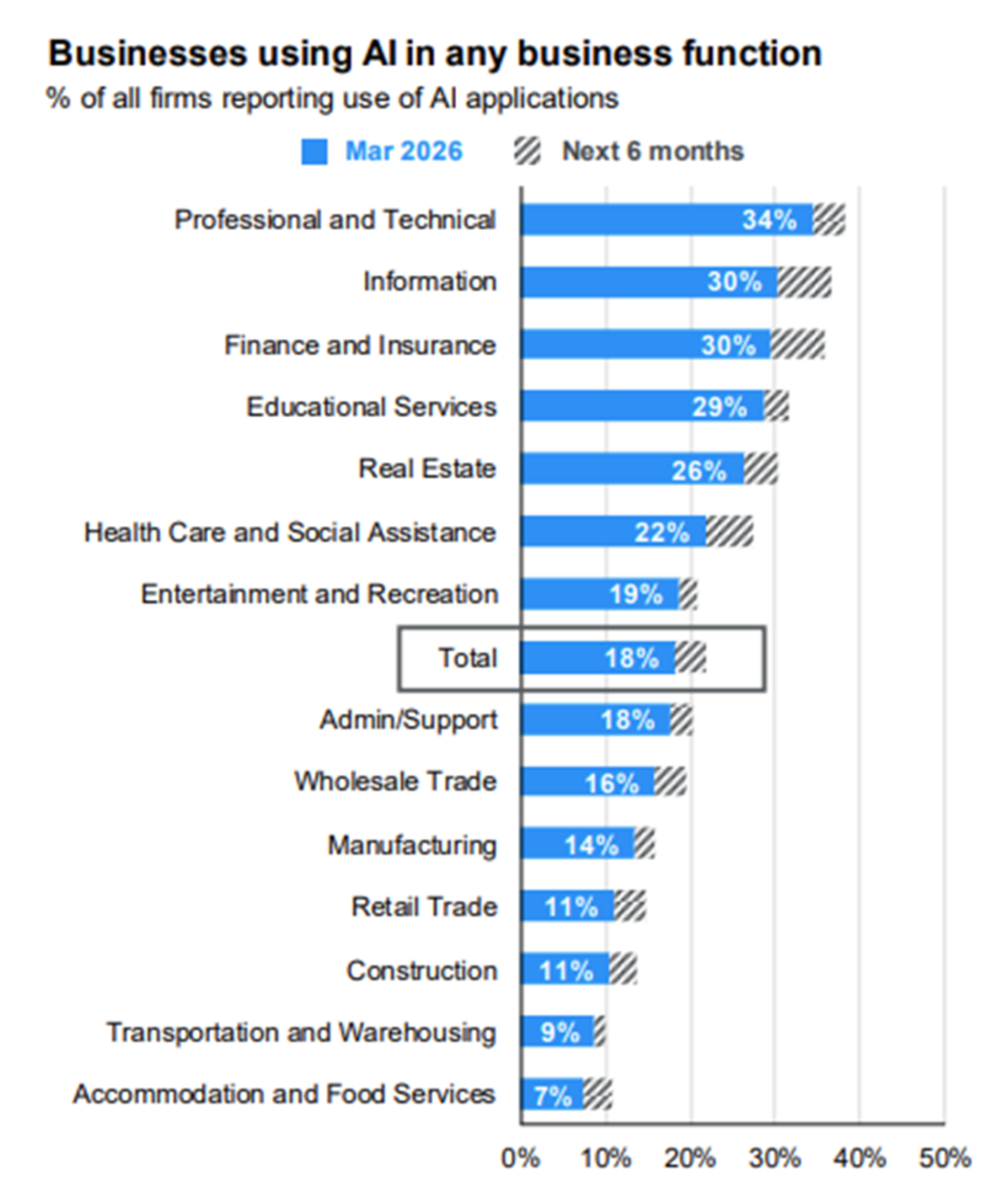

2026 in Focus: AI-Bubble Fears

- The implementation of AI continues to spread across nearly every business sector of the economy. A disproportionate share of equity market gains, especially in the U.S., have been driven by companies most directly exposed to AI over the past couple of years.

- Expectations for future revenue and earnings growth for these firms remain elevated, despite very lofty valuations.

- Despite a slowing in the momentum of the AI trade due to macroeconomic and geopolitical factors, the overall theme and growth potential remains intact.

- Unlike past bubbles centered around tech, AI leaders have shown persistent revenue and earnings growth. This is expected to continue, as we are still in the early stages of the AI cycle.

- Persistent revenue and earnings growth for AI firms is expected to continue as AI adoption rates accelerate in the quarters (and years) ahead.

- Takeaways

- AI is expected to be a transformational technology for the U.S. and global economy and is here to stay.

- Lofty valuations for AI stocks could lead to more downside risk than other parts of the stock market. Any meaningful drawdown in AI stocks is likely to present attractive investment opportunities for long-term investors.

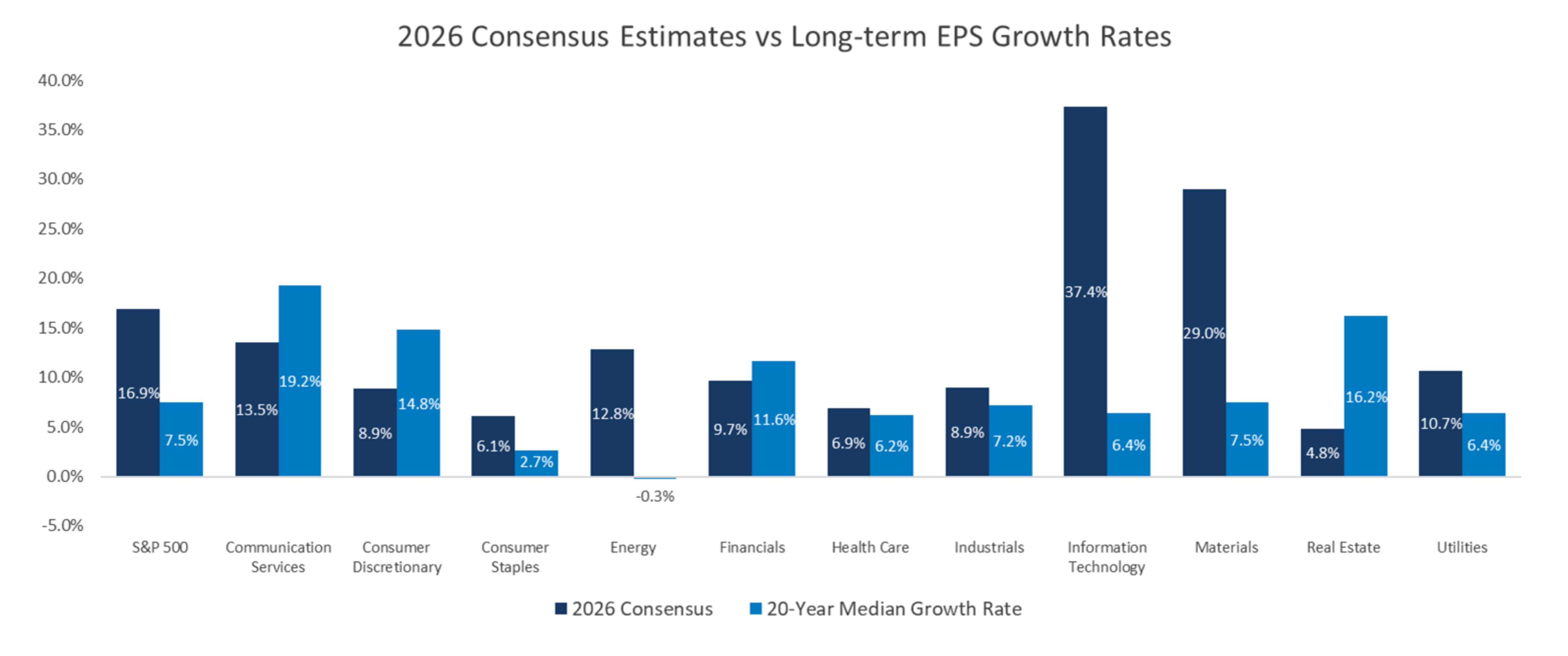

2026 in Focus: Earnings Expectations

- Earnings estimates for the S&P 500 have continued to rise despite geopolitical conflict.

- 2026 year-end earnings estimates have increased since the beginning of the year in the information technology, industrials, materials, health care, consumer staples, consumer discretionary and utilities sectors.

- Takeaway

- The information technology sector is expected to continue to report above-trend earnings growth in 2026. However, a broadening of earnings growth is expected beyond the mega-cap tech sector and across multiple areas of the market. Investors may benefit from diversification across sectors.

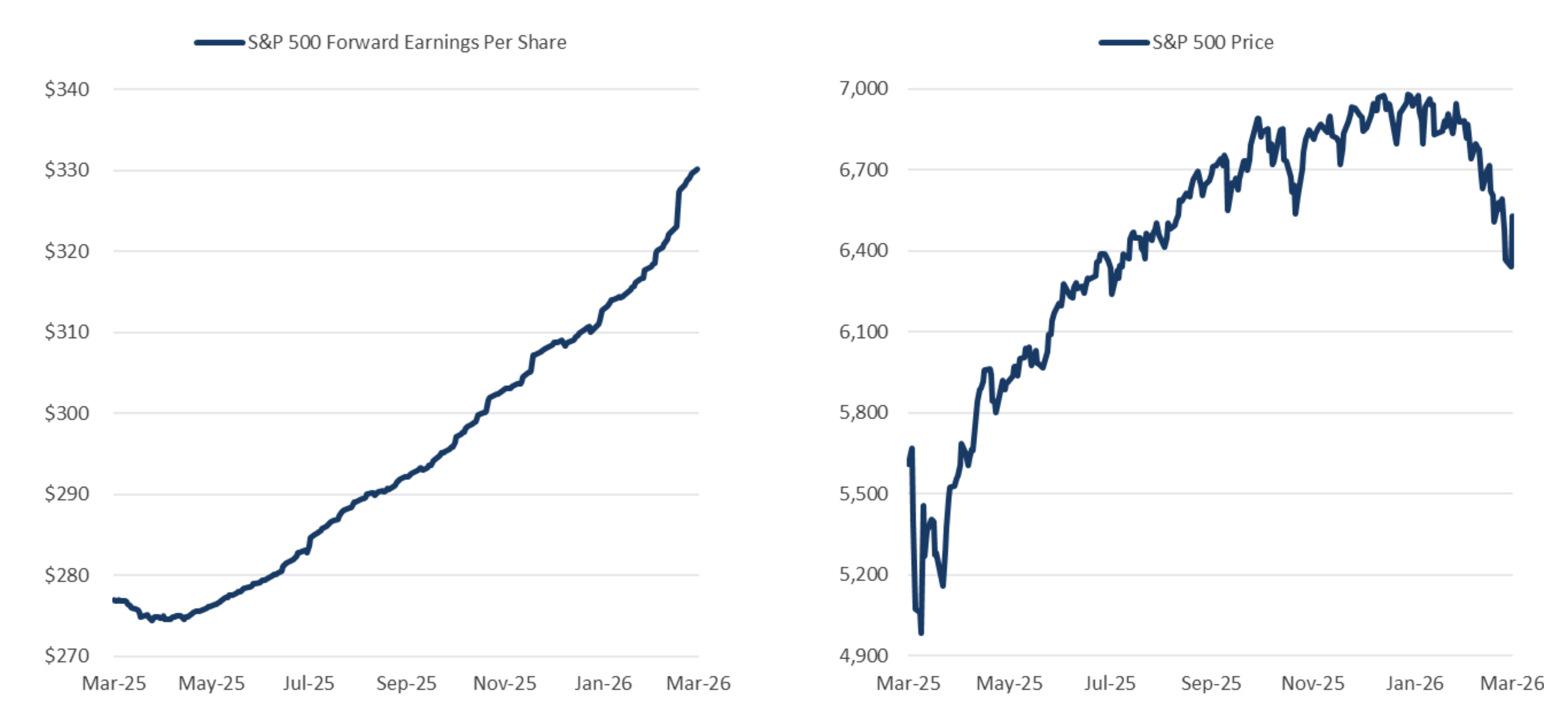

2026 in Focus: Earnings Expectations

Performance has been driven by multiple compression rather than earnings decline:

- Forward earnings expectations remain near highs while equity prices have declined, signaling a recalibration of valuation multiples.

- Even as earnings are rising, investors are currently willing to pay less for them. This reflects a shift in risk appetite rather than a change in the underlying earnings outlook.

- As valuations become more attractive due to earnings growth and price contracting, we believe that the ability to look past short-term volatility will benefit long-term investors.

- Takeaway

- Despite a backdrop marked by elevated geopolitical tensions and uneven economic data, corporate earnings remain notably resilient, underscoring the strength of the underlying fundamentals. Long-term investors should stay the course and look for opportunity as earnings growth is the primary driver of future stock prices.

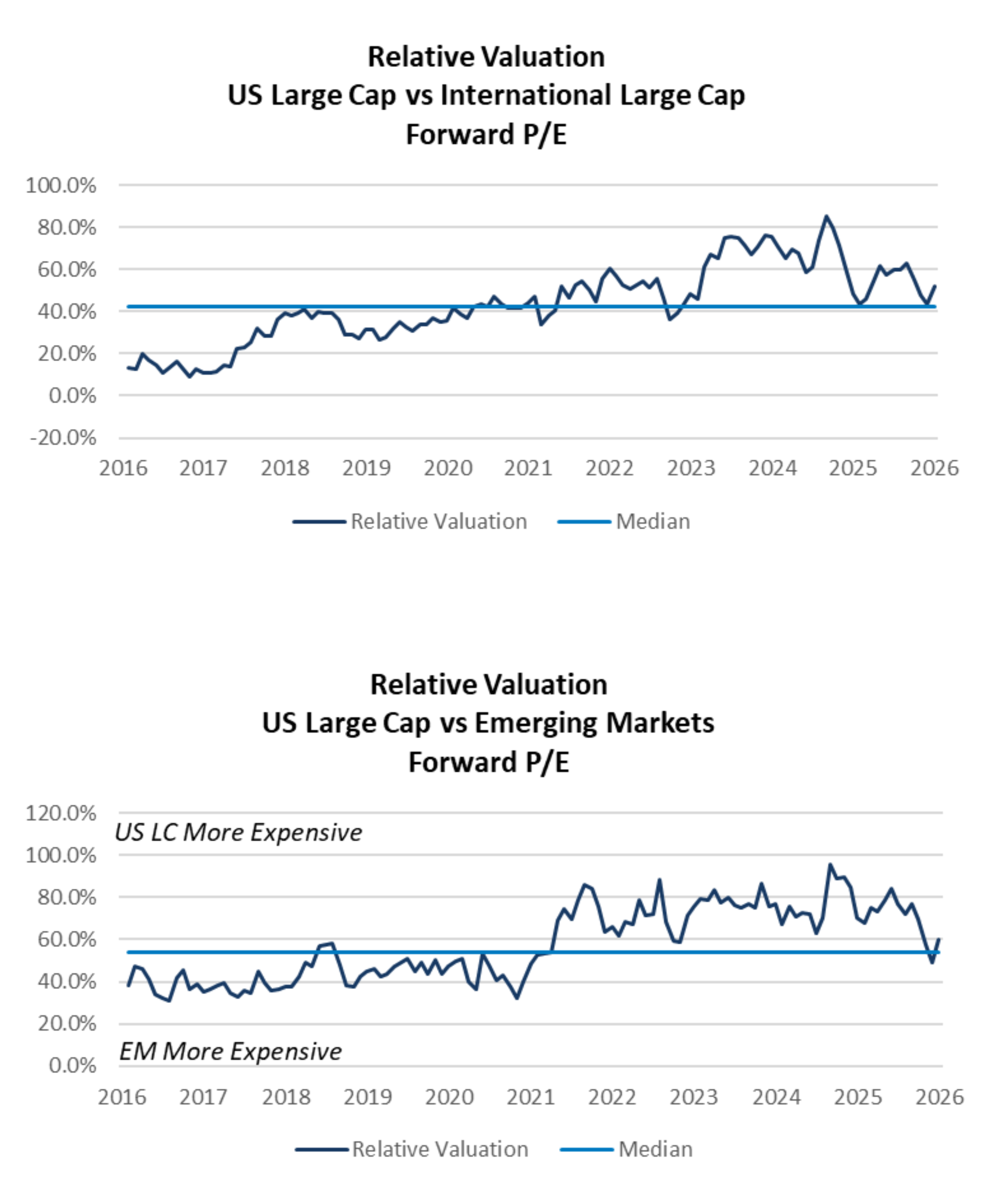

Relative Valuations: U.S. Large Cap Comparison

- International equities remain “less expensive” than U.S. stocks on a fundamental valuation basis, despite margin expansion in 2025 and early 2026.

- Emerging market equities also remain “less expensive” than U.S. stocks on a fundamental valuation basis, despite margin expansion in 2025 and early 2026.

- Takeaway

- Diversification outside the U.S. is prudent and we recommend investors have an allocation to international equity and EM equity.

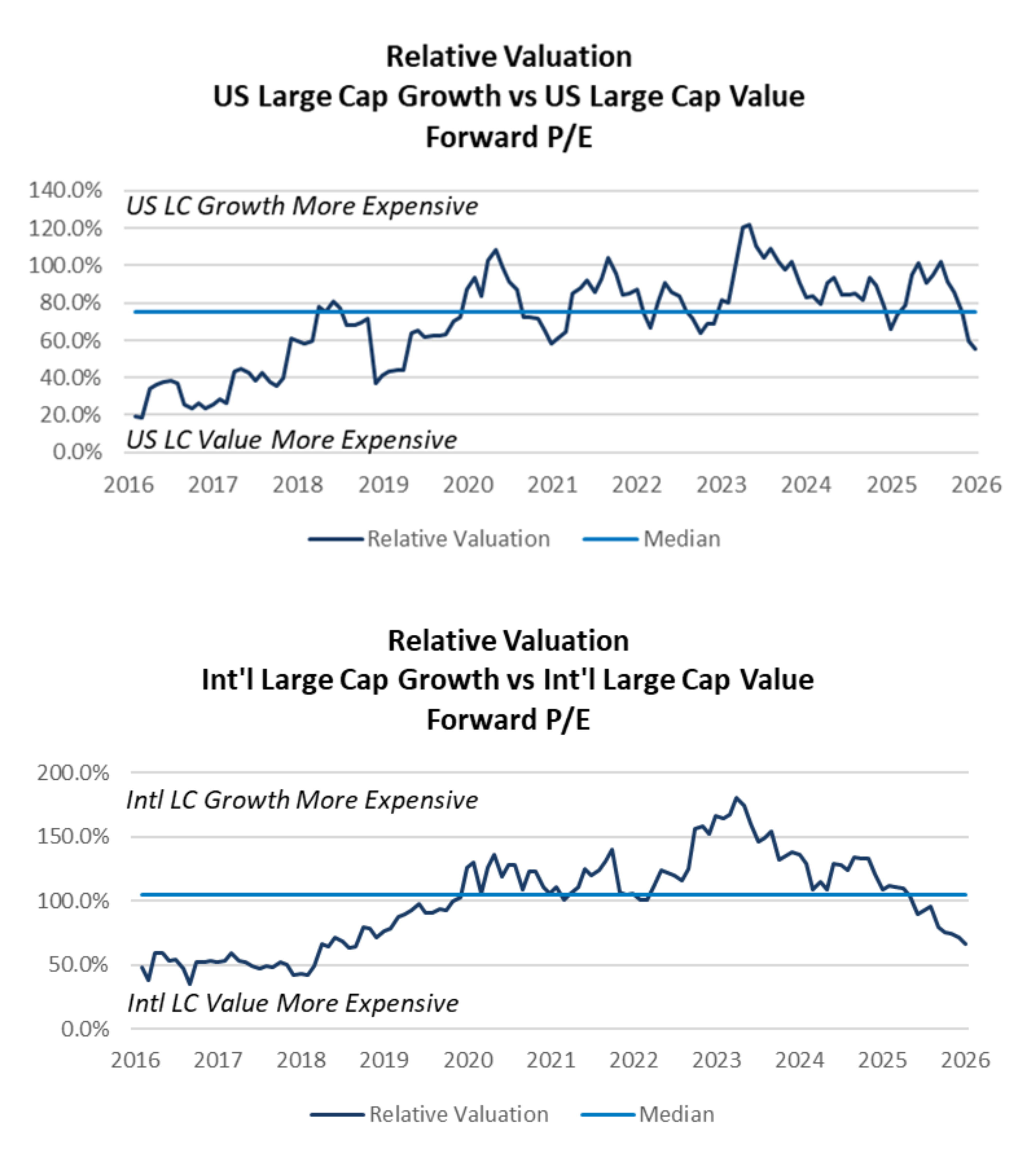

Relative Valuations: Growth vs. Value Comparison

- On a fundamental valuation basis, U.S. value stocks are currently “more expensive” than U.S. growth stocks.

- Growth stocks in the U.S. experienced meaningful declines in fundamental valuation measures during the first quarter of 2026.

- On a fundamental valuation basis, international value stocks are currently “more expensive” than international growth stocks.

- International value stock valuations have increased recently as investors homed in on low multiples, higher earnings expectations and thematic rotations out of growth equities.

- Takeaway

- While growth now appears more attractive for the first time since 2022, we continue to advocate for a tilt towards the more defensive value factor in the face of near-term global uncertainty.

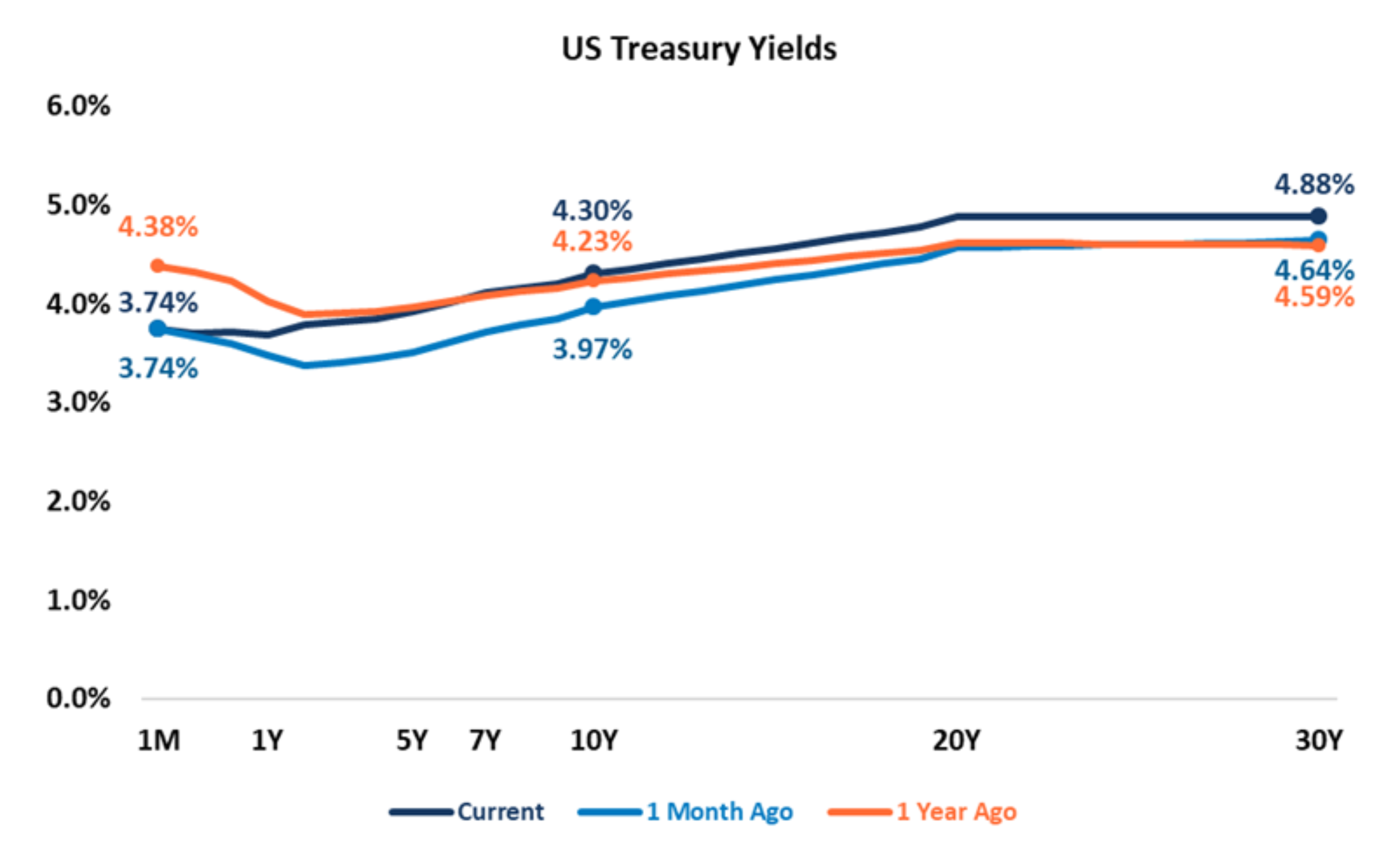

Fixed Income: Treasuries

- Yields across the U.S. Treasury yield curve shifted higher in Q1 due to uncertainty over inflation and growth expectations.

- Longer-term Treasury yields moved the most due to concerns over inflation and fiscal policy.

- With expectations for further rate cuts now not expected until 2027, the inversion of the yield curve at the short end will likely continue.

- Long-term yields could move higher in 2026, should concerns over U.S. debt and deficits escalate or geopolitical and inflation uncertainties increase.

- Takeaways

- Any shift in expectations for the path of rate cuts or changing developments out of the Middle East could lead to increased volatility in rates throughout the remainder of 2026.

- Any “good news” to calm the markets could be met with a sharp drop in longer-term rates, but the number of unknown variables makes it difficult to predict.

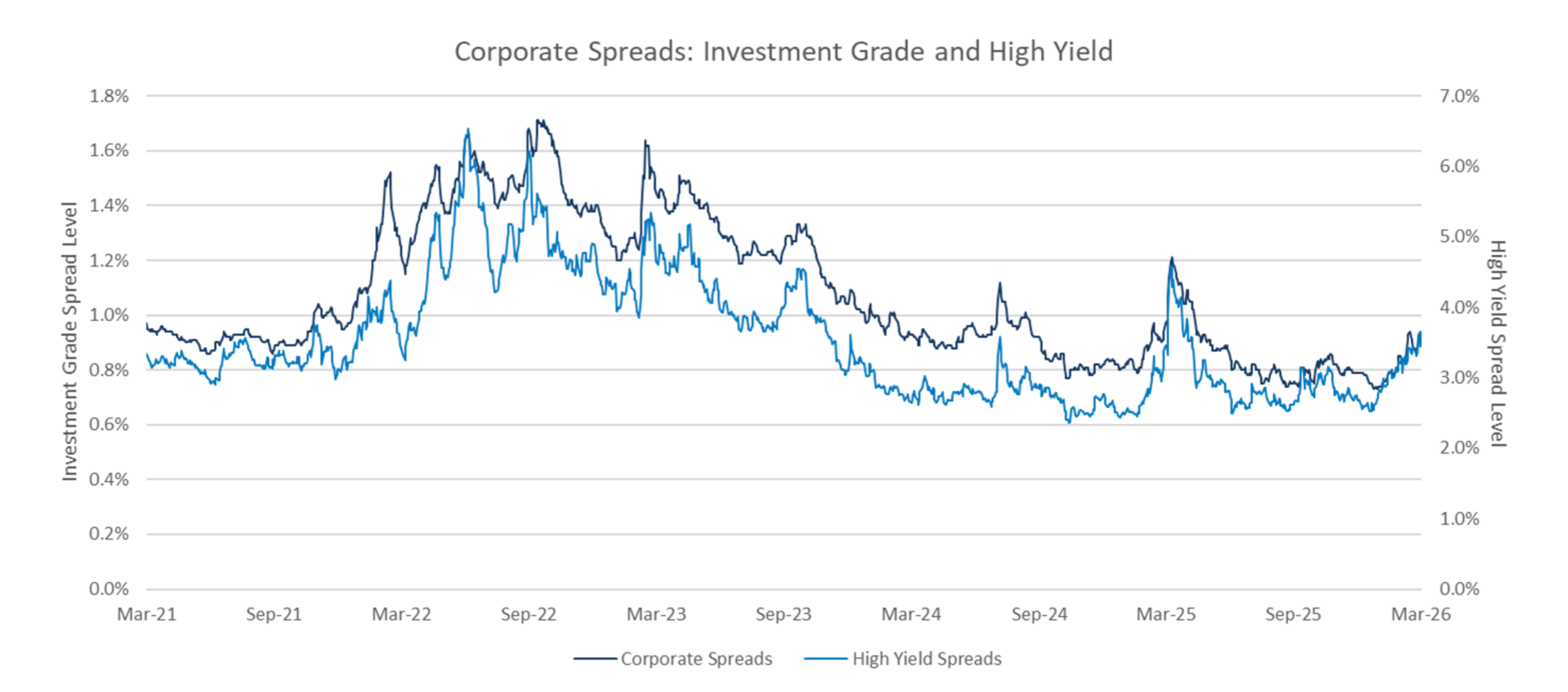

Fixed Income: Credit Spreads

- Starting 2026 near multi-year lows, credit spreads widened in Q1 due to a variety of factors: greater new issuance, policy uncertainty and macro shocks.

- High-yield spreads were more vulnerable than investment grade to market factors because of already rich valuations and limited spread compensation. Rather than a recessionary scare, this appears to be more of a repricing of historically tight spreads after a strong run of demand following the April 2, 2025 volatility shock.

- Takeaway

- Credit valuations have become increasingly more attractive as spreads have widened towards their long-term averages.

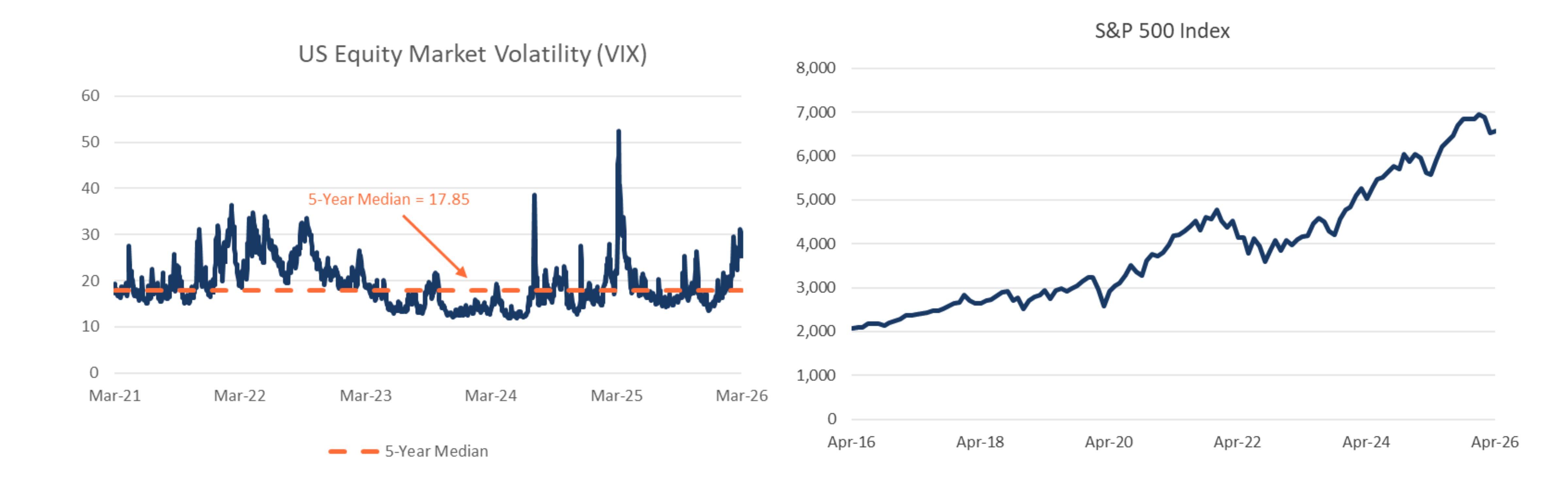

Staying Invested Through Volatility

- Rising volatility levels often reflect fear first and fundamentals later, leading to a poor timing tool for exiting long-term equity holdings.

- Volatility is currently elevated as markets are repricing geopolitical risk, policy uncertainty and valuations all at once.

- The current setup argues for sticking to a disciplined investment strategy rather than letting headlines and emotions drive decisions.

- Takeaway

- As painful as market volatility can be, equity market selloffs are normal, and investors are rewarded for patience.

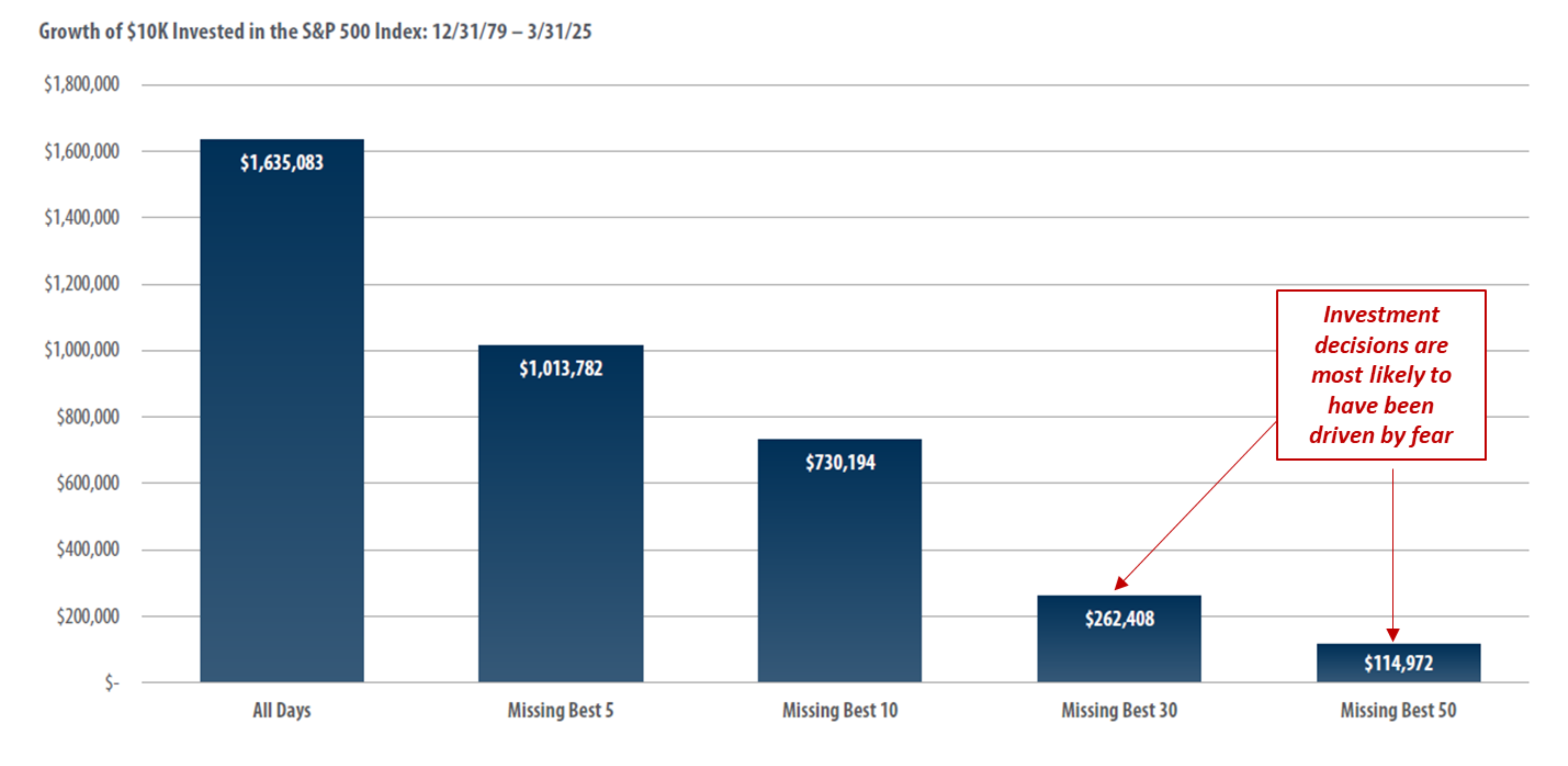

Long-Term Investors Should Stay Invested

- The chart highlights how a $10k investment in the S&P 500 would grow over the next 45 years.

- If the investor missed the best 30 days of market performance, the investment portfolio would be worth more than $1.3M less than if the investor had stayed in the market.

- Takeaways

- The market’s best performance days typically occur during periods of elevated volatility.

- Regardless of what may be in store for the macroeconomy and capital markets, long-term investors should avoid the temptation to exit out of markets during periods of elevated uncertainty.

- Riding out market volatility is the best way to build wealth over the long term.

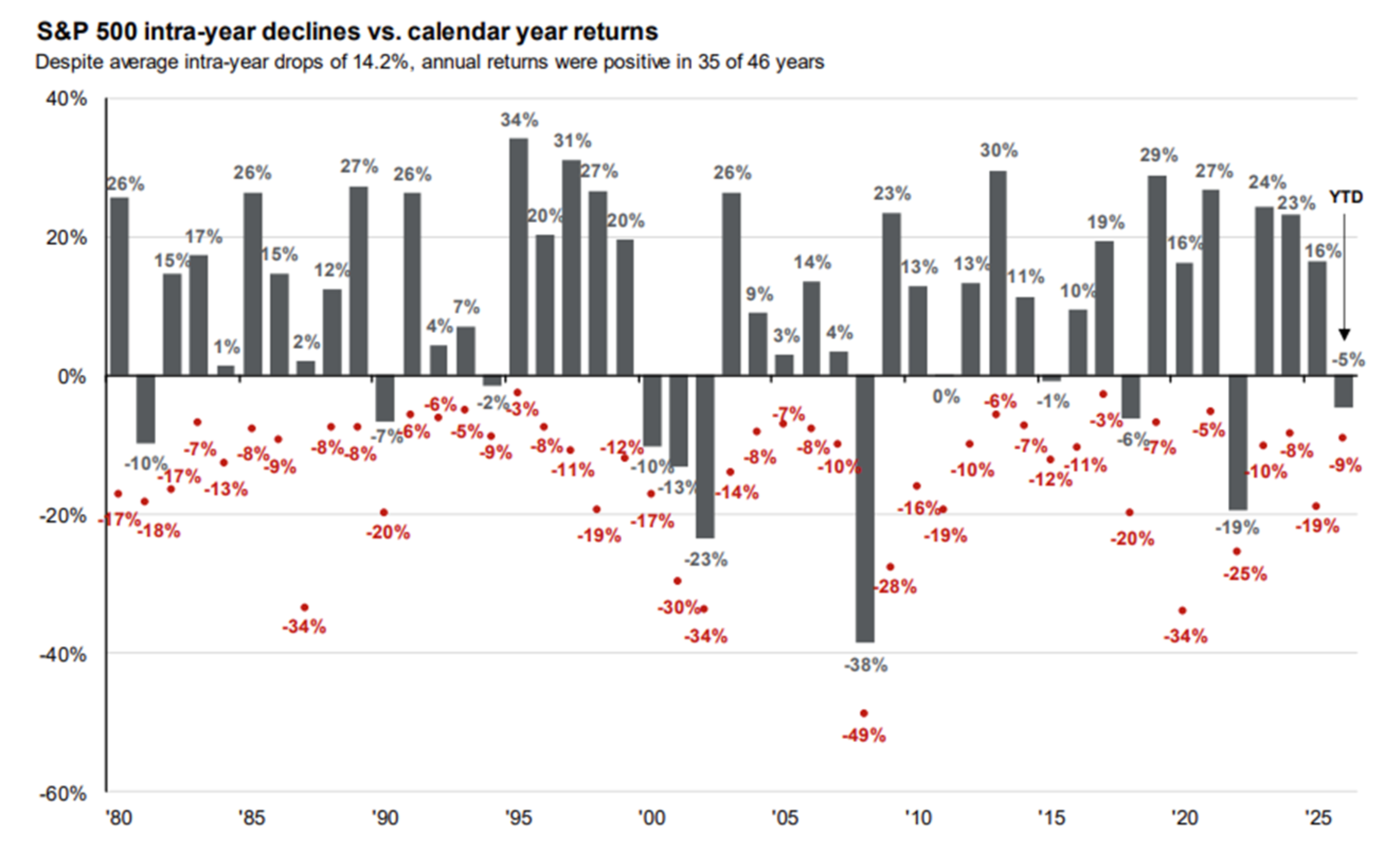

Equity Market Volatility

- The chart illustrates annual S&P 500 performance since 1980 (shown in columns above) and the intra-year declines during each year (shown by the red dots).

- Ex: In 2020, the S&P 500 experienced an intra-year decline of -34% before finishing up 16% for the year.

- Over the past 46 years, the S&P 500 has experienced an average intra-year decline of 14%. Despite that, the S&P 500 had positive annual performance in 34 of the last 46 years.

- Takeaway

- As painful as market volatility can be, equity market selloffs are normal, and investors are rewarded for patience.

Playbook Summary

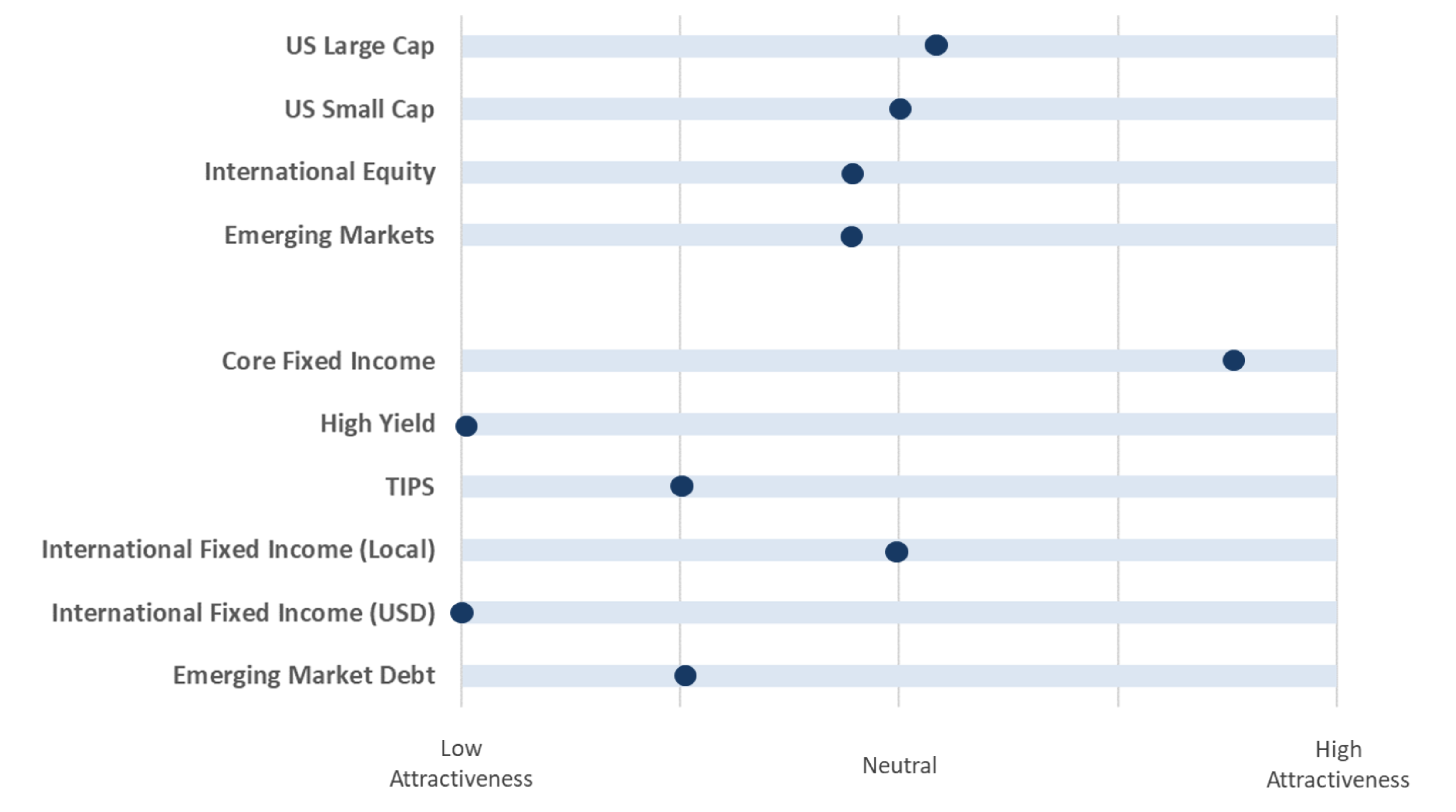

- The above table indicates where each major investment asset class falls on the distribution of attractiveness (from low to high). This table is meant to provide a standardized and comparable view of the level of opportunity in each asset class category.

- In subsequent quarters, we will discuss any movement along the scale for each asset class and the driving forces behind the change in outlook.

Disclosures

Investment services offered by Enterprise Bank & Trust are not deposits, obligations, or guaranteed by the bank or its affiliates. The information provided represents the opinions of Enterprise Bank & Trust and is not intended to forecast future events or guarantee future results. Past performance does not guarantee future returns. This information is for educational purposes only. Investors should consult with their investment professionals for advice concerning their particular situation.

Investments are: *Not FDIC insured *May lose value *Not financial institution guaranteed *Not a deposit *Not insured by any federal government agency.