Market Flash Report | February 2021

Executive Summary

United States

- The U.S. economy is forecast to grow sharply in 2021 after declining with the COVID pandemic last year. Estimates for Q1 range from +4.5% to +7.1% with the average being +6.1%. Goldman expects GDP to grow 6.9% in 2021 and that is towards the high end of the consensus estimate range.

- The manufacturing and service sectors are very healthy today with PMIs sitting well above the 50 level which separates expansion from contraction. New orders and production are driving activity while some businesses remain concerned about the pandemic/lockdowns and the lack of talented employees available.

- 2021 has been all about interest rates and rising inflation expectations. Although inflation remains contained, expectations have risen over the past 6 months and rates have spiked higher YTD. Equities, especially growth stocks, have been hit hard by the move higher in rates.

Non-U.S. Developed

- The eurozone economy fell around 6.6% in 2020 with the U.K. being harder hit with a decline of nearly 10%. Both economies are projected to rebound 5.1% and 6.3% respectively in 2021. The pace of the rebound will largely depend on the vaccine rollout, containment of new variants and timing of easing restrictions.

- The eurozone composite PMI strengthened a bit in February, but remains below the all-important 50 level. Services have weakened in recent months while manufacturing has rebounded to its highest level in months. Not surprisingly, lockdowns and harsh restrictions have hit consumer spending and the service sector particularly hard recently.

- Japan’s economy contracted nearly 5% last year, but economists expect it to rebound 3.4% in 2021. Japanese companies have become very good at delivering earnings growth in a slow growth environment. Earnings fell 1.6% in 2020, but they are forecast to grow 36% in 2021.

Emerging Markets

- The Chinese economy grew 2.3% in 2020. The country did a great job overall containing COVID and over the second half of the year, retail sales and consumer spending strengthened. Recent data show a slight moderation in the level of growth.

- Economists expect China’s economy will grow over 8-10% in 2021. GDP is forecast to grow 12% in India, 3% in Brazil, 3.5% in Russia and 5% in South Korea.

- EM earnings were quite resilient in 2020, largely due to positive growth in China and other key Asian countries. EM earnings are expected to grow 36.9% in 2021 and 15.2% in 2022.

- The EM growth story is compelling as economic/earnings growth is forecast to be higher than the developed world.

Fixed Income

- Treasury/sovereign debt yields continued their march higher in February. Core/muni bonds lost ground while spread tightening led to gains in riskier credit. The USD also strengthened versus most currencies.

U.S. Equities

- U.S. equities surged higher to start the month, but higher Treasury yields spooked investors and led to selling pressure at the end of the month.

- Small caps continued their dominance of large caps and value handily outperformed growth.

- Large cap growth/technology stocks have exhibited particular weakness over the past few months.

Non-U.S. Equities

- Non-U.S. developed equities ended the month in similar fashion to large cap U.S. equities.

- Outside the U.S., value stocks beat growth stocks and small caps slightly outperformed large caps.

- After outperfoming for most of the month, EMs were hurt by weakness in China/Asia.

- USD strength cost U.S. investors 37 bps in development and 27 bps in EMs.

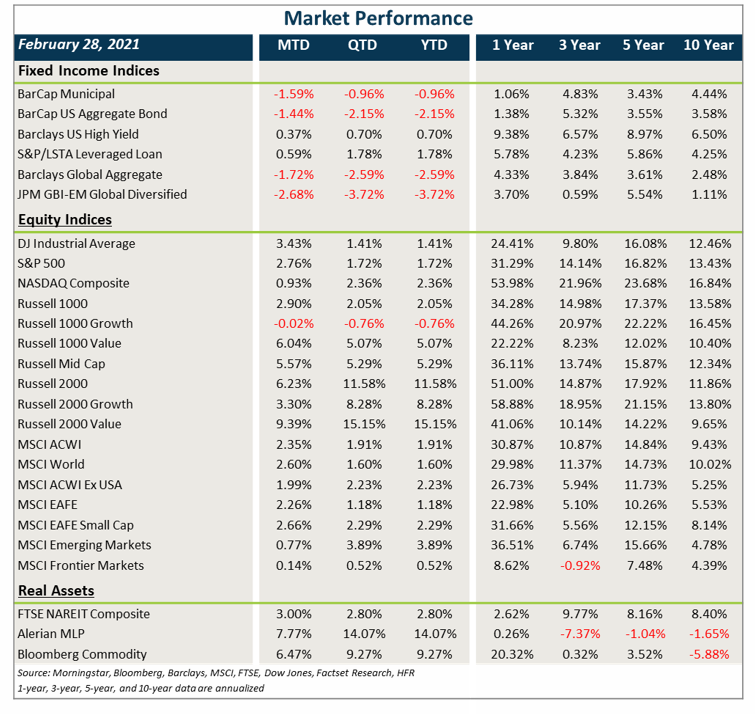

Market Performance (as of 2/28/21)

Sector Performance

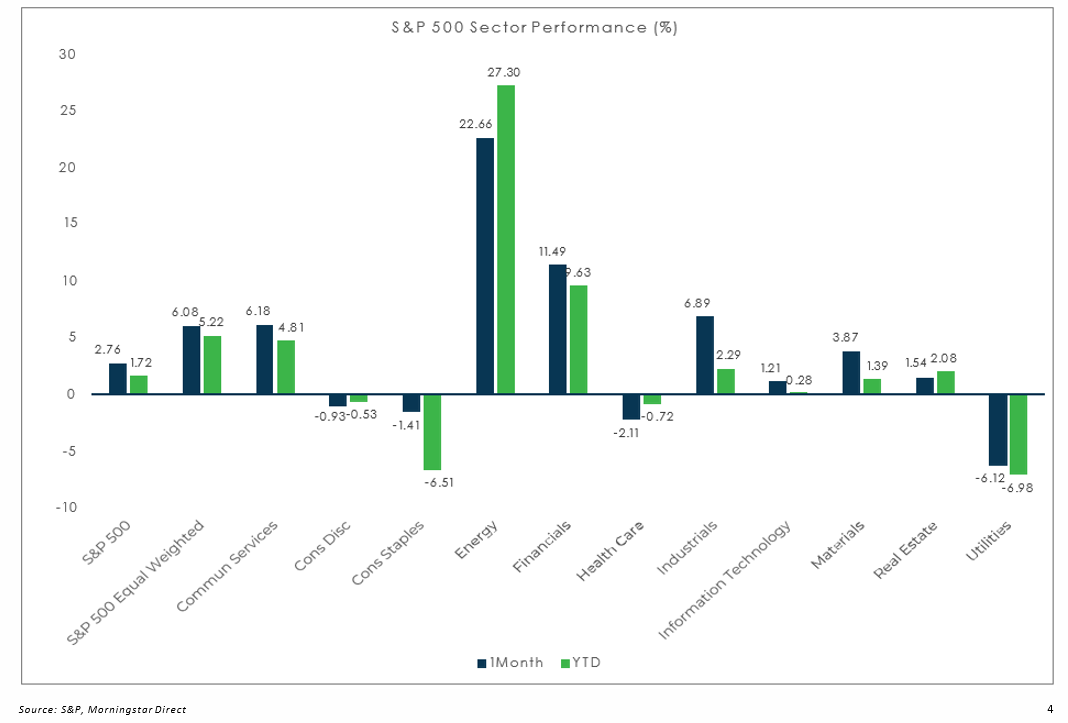

S&P 500 as of February 28, 2021

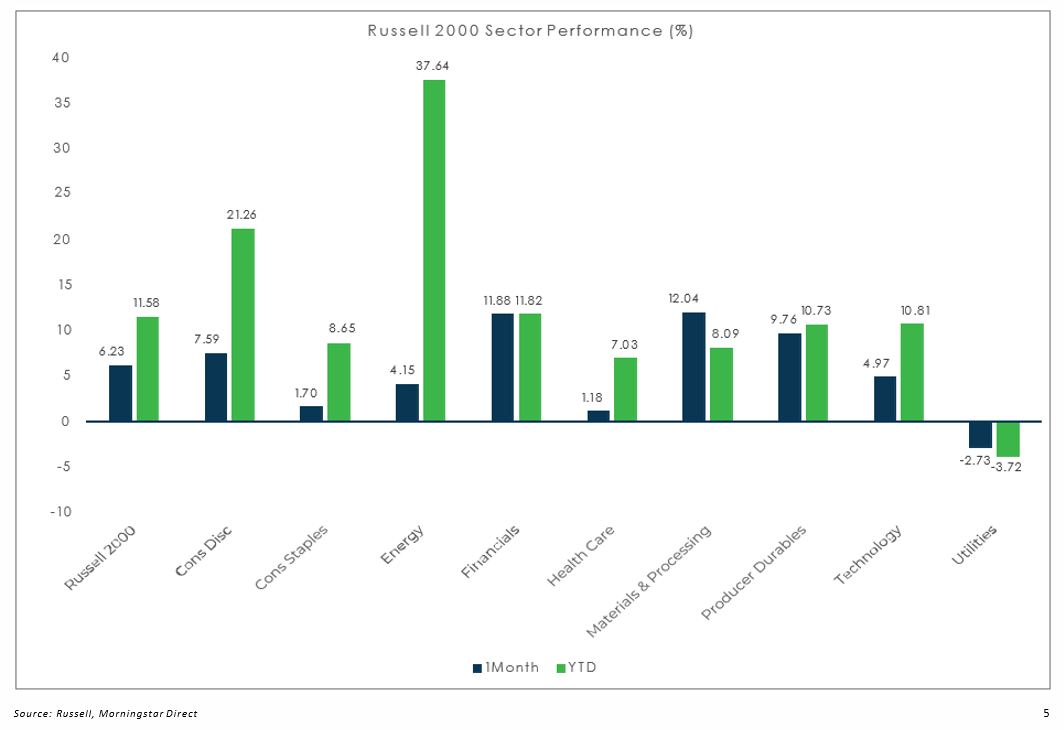

Russell 2000 as of February 28, 2021

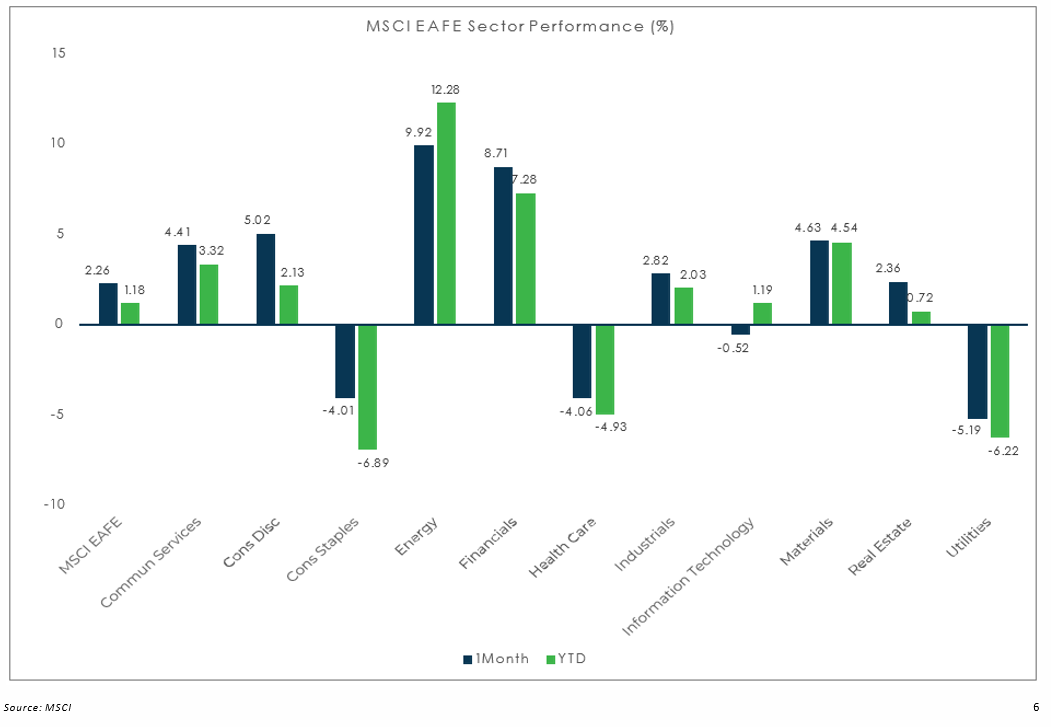

MSCI EAFE as of February 28, 2021

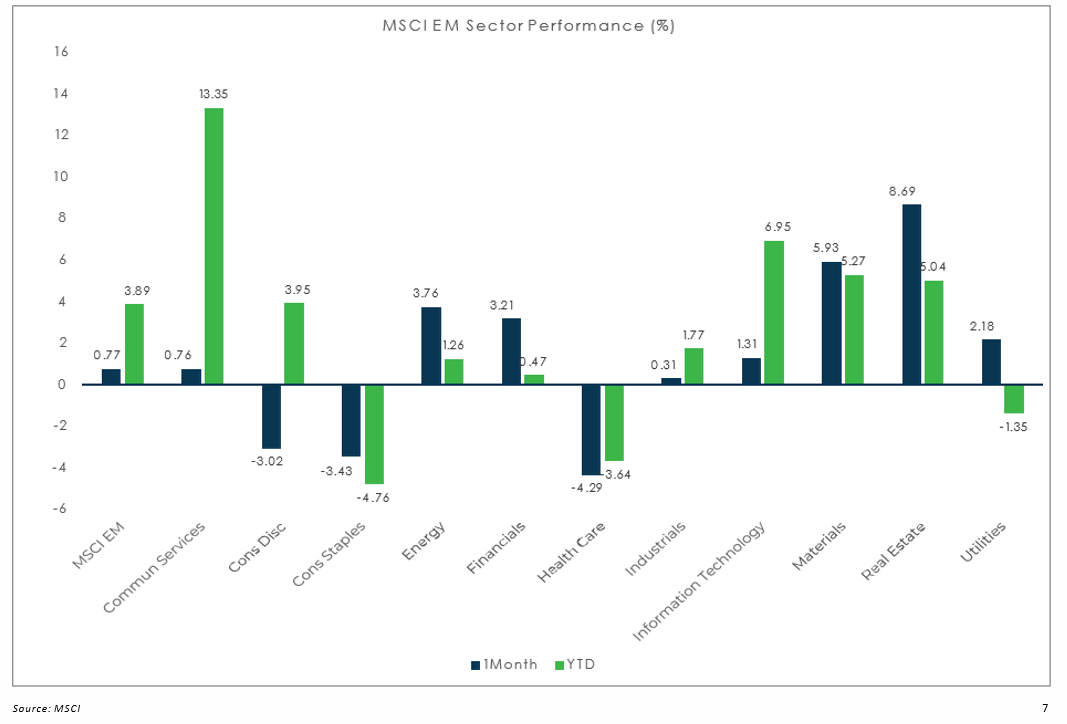

MSCI EM as of February 28, 2021