In the world of investment finance, few institutions are followed more closely than the US Federal Reserve. Although central banks across the globe are vital to global capital markets, the Fed is by far the most influential.

Over the years, investor focus on the Fed has grown significantly, with market participants pouring over every statement made by Fed officials. Especially the Fed Chairman. This Thursday, Federal Reserve Chairman Jerome Powell spoke about changes to the Fed’s monetary policy framework. While the changes have been expected by market participants for some time, Chairman Powell’s comments are going to be a subject of debate for investors across the world.

The Fed’s “Dual Mandate”

Since 1977, the Fed’s primary goal has been to use its monetary policy tools to maintain stable prices and full employment, otherwise known as its “dual mandate”.

To achieve its dual mandate, the Fed has a wide array of policy tools at its disposal. The Fed’s primary tool is what is referred to the “federal funds rate”. The federal funds rate is the interest rate that the Fed will adjust up or down- depending on prevailing economic conditions- to try to manage price levels and employment.

With the federal fund rate near 0% for much of the past 12 years, the Fed has been forced to come up with new and creative monetary policy tools to spark economic growth (currently, the Fed is loath to reduce its federal funds rate below 0%). These “unconventional” monetary policy tools include quantitative easing (i.e. buying bonds) and forward guidance (i.e. clearly communicating future Fed intentions to reduce uncertainty and restore confidence).

The Fed uses its conventional monetary policy tools in a “countercyclical” manner. For example, the Fed will look to raise interest rates when inflation is at (or near) 2% and unemployment is low (or reduce interest rates during periods of high unemployment and inflation is below its 2% target). This exercise is not as simple and straightforward as it may seem due to structural changes that make the determination of “full employment” extremely challenging (a wonky, nuanced topic that we will save for another day). That said, the Fed does appear to be comfortable with its dedication to a 2% long term inflation target.

Why Did the Fed Study Its Monetary Policy Framework?

The primary theory underlying the Fed’s monetary policy is that as unemployment moves lower, workers become more scarce, and wages increase. As wages increase, consumers spend more. As consumers spend more, goods and services become more scarce. And as goods and services become more scarce, prices go up. In other words, low unemployment leads to higher prices. This relationship between employment and inflation was significant for decades, but its explanatory power has diminished in recent years for reasons that economists cannot agree upon.

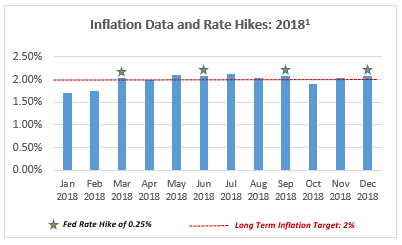

As an example, inflation began to show signs of nearing the Fed’s 2% target in 2018 (and unemployment was near 50 year lows). During this time, the Fed raised rates a total of four times even though inflation never exceeded 2% in a meaningful way. While the decision to raise rates during this will be a subject of debate for years to come, many economists have suggested that the Fed’s rate hikes during a period of moderate inflation was a policy mistake.

Wary of “falling behind the curve”, the Fed decided to review its policy framework to address the relevance of its existing theory and determine if there were any additional methods that could be employed to achieve its dual mandate when rates are as low as they have been.

How is Monetary Policy Changing?

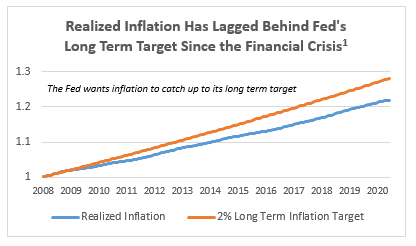

The Federal Reserve is prepared to shift is stance towards inflation. For years, the Fed has targeted a 2% inflation rate….but for years, despite very low unemployment, inflation has fallen short of the 2% target. Even during the recovery from the financial crisis, inflation remained stubbornly below 2% despite unemployment having reached its lowest level in decades.

Following the Fed’s review of its monetary policy, it has decided that it will allow inflation to rise to levels above 2% during periods of economic expansion in order to “catch up” to its long term inflation target. While it is unclear just how much the Fed will allow inflation to rise above its target over the short term, it is important to know that realized inflation undershot the Fed’s inflation target by an average of 0.4% on an annualized basis since 2008. The Fed has been (and will likely continue to be) somewhat vague in just how much inflation it will allow over the short term.

While this may appear to be a small change in monetary policy, the Fed’s willingness to allow inflation to tick above its 2% target could have a meaningful impact on the term structure of interest rates, the value of the US dollar, and the profitability of certain industries and investment asset classes in the quarters ahead.

Impacts for Investors

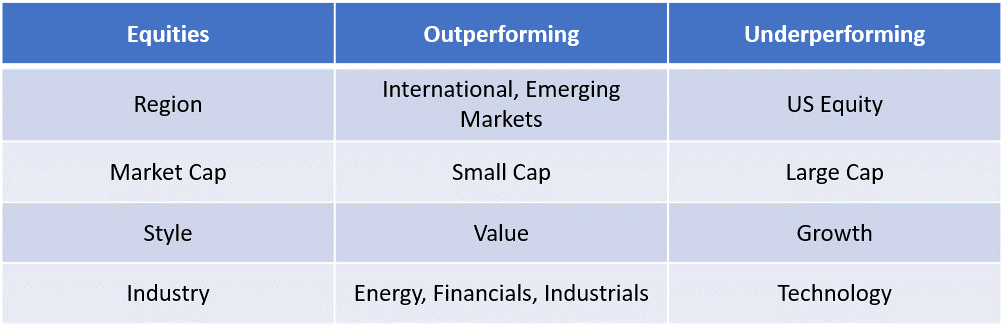

If the Fed allows inflation to “run a little hotter” in the quarters ahead, a number of capital market outcomes become more probable. In particular, higher than expected inflation could lead to a steeper yield curve and a weaker US dollar. Of course, capital markets do not exist in a vacuum, so variables outside the Fed’s control can certainly offset the impact monetary policy may have. That said, the table below lists the asset classes that have historically outperformed (and underperformed) during periods of higher than expected inflation.

In Summary

The Federal Reserve’s change in its monetary policy framework will certainly have an impact on capital markets, but the extent of the impact will likely not be known for some time. If the Federal Reserve is aggressive in letting inflation catch up to its long term 2% target, it is likely some of the asset classes that have struggled since the financial crisis (International and Emerging Market equity, Financials) will benefit at the expense of those that have done very well (US Large Cap, Technology). Of course, a well diversified portfolio should include all of the asset classes in the tables shown above. Tactical investors may consider rebalancing their investment portfolios to get ahead of a potential regime change.