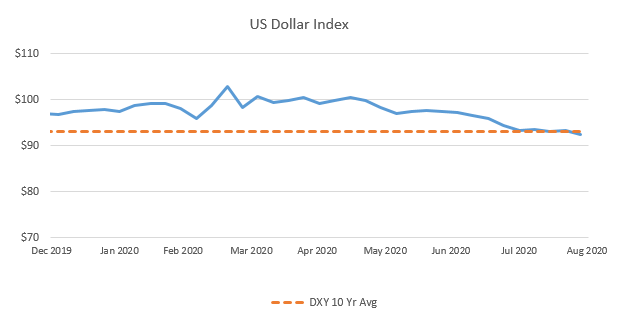

US Dollar Valuation

As the market value of many risky financial assets have exploded higher over the past five months, the value of the US dollar has simultaneously declined to multi-year lows. While the value of the dollar remains near its longer term average, the recent decline has been breathtaking and surprising to many.

Typically, the dollar strengthens during periods of elevated uncertainty. But this has not been the case following the height of this year’s market panic. Year to date, the US Dollar Index, which measures the strength of the US Dollar relative to a basket of major currencies, has declined more than 4% through August 31. This decline has taken place during one of the most uncertain economic backdrops the world has seen since the Great Depression.

Why has the dollar declined so much in such a short period?

As is the case with many investment assets, demand for the US dollar is largely based on expectations for interest rates, expectations for inflation, and expectations for economic growth. Furthermore, it is the relative growth rate of these variables that have historically had the most influence on demand for the dollar. To get a true sense as to how the dollar may move in the future, investors compare how these important macroeconomic variables may change in the US to how the same variables may change in other countries.

In short, the recent weakness of the US dollar can be attributed to the following expectations:

- Investors expect stronger inflation growth in the US compared to other countries.

- Investors expect lower interest rate growth in the US compared to other countries.

- Investors expect lower rates of economic growth in the US compared to other countries.

Explanation of expected relative growth rate

Dollar valuation is a very complicated subject, and relative growth rate expectations are tough to explain in written form. A simple scenario may help make this concept a little easier to comprehend.

Remembering that higher rates of inflation tend to decrease the value of a currency (all else equal), consider the following hypothetical example…

- The rate of inflation in the US is expected to be 2% in a year. The rate of inflation in the United Kingdom (UK) is also expected to be 2% in a year.

- The current rate of inflation in the US is 1.0%. The current rate of inflation in the UK is 1.5%.

In this example, an investor can say the following…

- Although inflation is expected to be 2% in both the US and the UK, it is the US dollar that would be expected to decline in value relative to the Pound.

- The dollar would be expected to decline because its expected growth rate of inflation is higher than the expected growth rate of inflation in the UK. Inflation is expected to have a 100% growth rate in the US (an increase from 1% to 2% = 100% growth). Inflation is expected to have a 33% growth rate in the UK (an increase from 1.5% to 2%).

In other words, the investor will expect that the US dollar will decline in value relative to the UK pound since the growth of inflation will be three times higher than the growth rate of inflation in the UK. (US inflation growth rate 100% / UK inflation growth rate 33%= 3).

Why might dollar weakness continue?

There are major reasons why investors expect the relative growth rates of important economic variables to continue to put pressure on the US dollar over the next couple of years.

- Why will inflation increase more rapidly in the US than in other countries?

- Total stimulus in the US has dwarfed the support provided by central banks and governments in other countries. Assuming unemployment in the US continues to improve and consumption remains strong, more money will be chasing after a smaller supply of goods and services.

- For the time being, the Federal Reserve will not hike interest rates if inflation ticks marginally above its 2% long term target.

- Why will interest rates not grow as fast in the US?

- The Federal Reserve has indicated a strong commitment to keep short term interest rates at 0% for an indefinite period of time. Many developed countries have negative interest rates. With signs of economic improvement, foreign central banks may be quick to raise their policy rates to get back to 0%.

- The Fed has committed to use quantitative easing in an effort to support liquidity and economic activity. Quantitative easing is the process whereby the Fed buys Treasury bonds (and others fixed income instruments) in an effort to keep yields low.

- Why will economic growth lag that other counties?

- Some countries have done a better job of containing growth of the virus and are currently operating closer to full economic capacity compared to the US. Asian countries, in particular, fall into this category.

- Some countries are expected to have economic growth that mirrors what is expected in the US, but are starting from a lower base. In other words, these countries are currently trailing the US in economic activity, but are expected to “catch up” to the US economic growth in the next year or two.

What asset classes and sectors will benefit the most from weaker dollar?

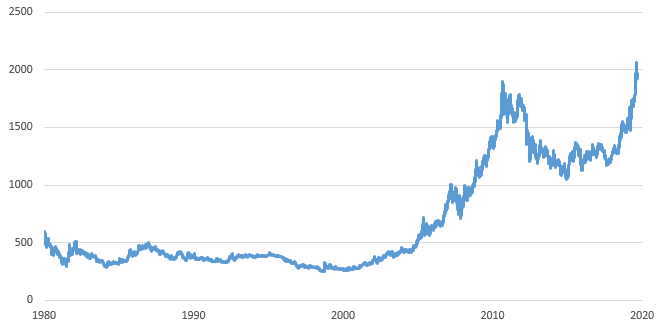

Much has been made of gold’s run-up in 2020. The asset has posted very strong returns year to date (up more than 25%), with much of the run-up taking place since equity markets hit lows in late March. But gold is considered a “safe-haven asset”, or one that has greater demand during periods of uncertainty. While gold is one of the better hedges against dollar depreciation, investors should recall that gold has a number of flaws. These include:

- Gold is a “store of value” and does not produce income like a bond does.

- Gold is not a “productive asset” and will not provide an opportunity for growth like equities do.

- Gold can be just as volatile as equities are, but has historically posted annualized returns that are similar to cash.

Gold Spot Price

Furthermore, gold has recently breached its all-time high. Considering that gold is not a “productive asset” and does not produce income, it is probable that the upside from its current level is not as high as many may believe.

Although the asset class may have more room to run, investors looking to hedge against dollar weakness have other investment options that do have the ability to produce income, provide opportunities for growth, or both.

Asset classes that outperform during periods of dollar weakness?

In general, commodities have historically been the strongest outperformer during periods of dollar weakness. In addition to precious metals like gold, agricultural and energy based commodities typically perform well as the dollar falls in value. But, investors should remember that commodities are not the only way to take advantage of a weaker dollar. The table below highlights asset classes that typically outperform during a period of sustained dollar weakness.

In summary…

Like most investment assets, the US dollar goes through cycles of relative strength and relative weakness. Also like most investment assets, relative value is often based on the expected growth rates of important macroeconomic variables.

Since the financial crisis, the dollar has been relatively strong compared to most currencies. The dollar is one of the major currencies that is considered a “safe haven” and will strengthen if global economic growth expectations decline. But, if global growth continues to move in the right direction, the dollar may continue its current downward trend. There are many investment assets that will outperform as the dollar weakens, all of which should be included in a well-diversified portfolio.