November 2025 Market Update

Economic Highlights

United States

- Retail sales in the U.S. went up 0.2% M/M in September 2025, the smallest increase in four months, following a 0.6% rise in August. Sales rose the most at miscellaneous store retailers (2.9%) and gasoline stations (2%). Sales excluding food services, auto dealers, building materials stores and gasoline stations, which are used to calculate GDP, declined 0.1%, following a 0.6% gain in August.

- New orders for key U.S.-manufactured capital goods surged in September and shipments of these goods increased at a solid pace, highlighting the likely acceleration in economic growth during Q3. Excluding the volatile transportation sector, new orders rose 0.6% in September after a 0.5% gain in August. Non-defense capital goods orders excluding aircraft, a closely watched proxy for business spending, jumped 0.9% after an upwardly revised 0.9% increase in August.

- While the CPI report for October was canceled by the Trump Administration, the Bureau of Labor Statistics did release its October PPI report. PPI rose 0.3% M/M in October after falling 0.1% in the previous month. Year-over-year, producer/wholesale prices increased 2.7%.

- Consumer confidence in the U.S. fell sharply last month as more households expect to be worse off in the future. The actual reading of 88.7 was well below the 93.5 forecast and the 95.5 reading from October. Again, most of the weakness came from the Expectations Index, which dropped 8.6 points to 63.2. It is important to note that a level of 80 or below for the Expectations Index historically signals a recession within the next year, and the index has been below 80 since February 2025.

Non-U.S. Developed

- Eurozone manufacturing activity slipped back into contraction territory in November on weakening demand that forced firms to cut jobs at the quickest rate in seven months. The HCOB Eurozone Manufacturing PMI fell to 49.6 in November from 50.0 in October. New orders declined after stagnating in October. Export orders fell for the fifth consecutive month, highlighting persistent challenges in international markets. The current picture of the eurozone is sobering, as the manufacturing sector is unable to break out of stagnation and is even tending towards contraction. In Germany and France, PMI readings fell to nine-month lows of 48.2 and 47.8, respectively. Meanwhile, six other monitored countries reported growth, with Ireland leading at 52.8, followed by Greece at 52.7.

- Japan’s inflation held steady in November and industrial output unexpectedly rose, keeping the Bank of Japan on track to consider an interest rate hike in December or January. Core CPI rose at an annualized rate of 2.8%, well ahead of the BOJ’s 2% target. Industrial production also beat expectations on a rebound in autos. The main concern today is wage growth in Japan because it needs to keep pace with rising prices and affordability. Any monetary tightening by the BOJ could have an adverse impact on affordability.

Emerging Markets

- China’s factory activity unexpectedly contracted in November, according to the RatingDog China General Manufacturing PMI, which showed that soft domestic demand continued to cast a pall over the world’s second-largest economy. The headline reading of 49.9 in November was down from 50.6 in October. This private PMI survey has typically painted a better picture than the official polls because it focuses on export-oriented manufacturers. The private survey also tends to focus on smaller businesses, as opposed to the official PMI survey that focuses on larger companies.

- The official China manufacturing PMI showed China’s factory activity shrank for an eighth month in November, coming in at 49.2, a slight improvement from 49.0 in the prior month. New orders were weak in November, although there was a notable pickup in new export orders.

- Perhaps of greater importance was the contraction (first time since December 2022) in the official non-manufacturing PMI, which comprises construction and services. The headline reading declined to 49.5 in November, signaling weak domestic demand and softness in real estate.

- Industrial output expanded 4.9% in October from a year earlier, while growth in retail sales slowed for a fifth straight month to 2.9%. Both marked their weakest levels since August 2024. Signaling further economic malaise, China’s exports in October unexpectedly contracted for the first time in nearly two years, dropping 1.1% year on year, as businesses’ front-loading momentum tapered off.

- The latest economic data suggested that China’s growth is likely to decelerate further to below 4.5% in Q4 from the 4.8% expansion in Q3.

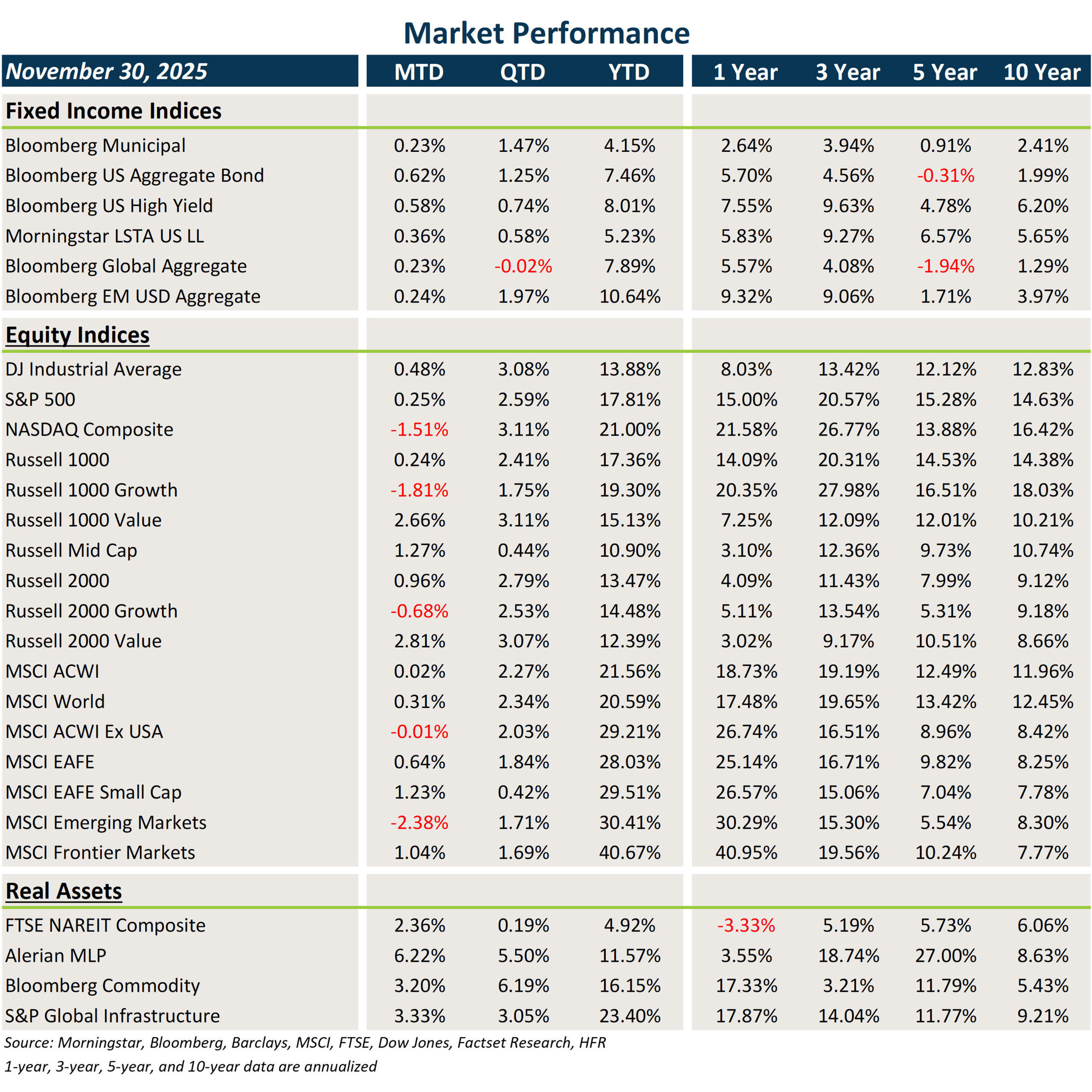

Market Performance (as of 11/30/25)

Fixed Income

- Fixed income across the globe benefited from lower interest rates and modest spread tightening in November.

- Core fixed income and municipal bonds gained ground, along with all credit sectors that benefited from coupon clipping at higher starting yields.

- Bonds outside the U.S. saw an added boost from a slightly weaker U.S. dollar during November.

U.S. Equities

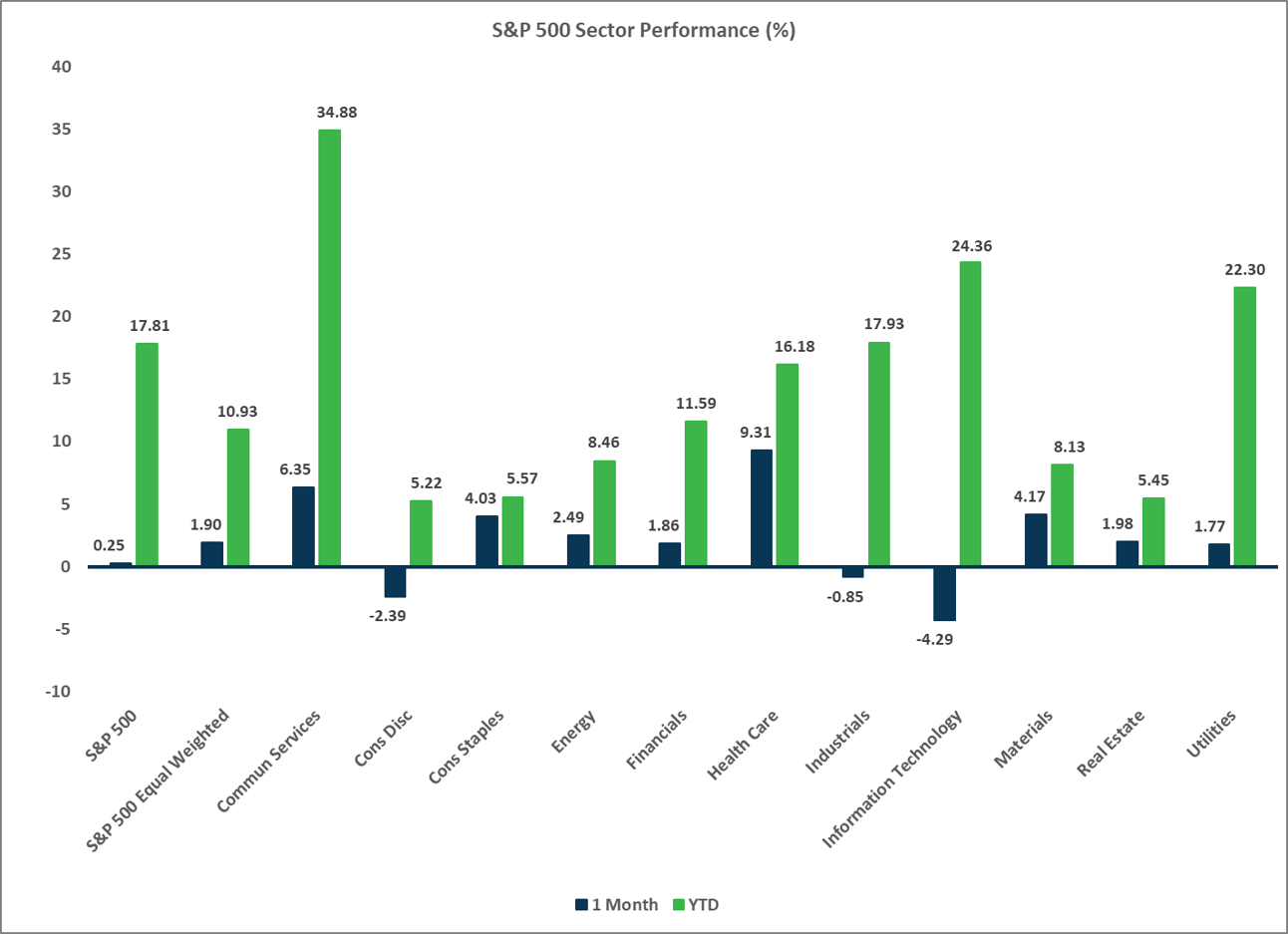

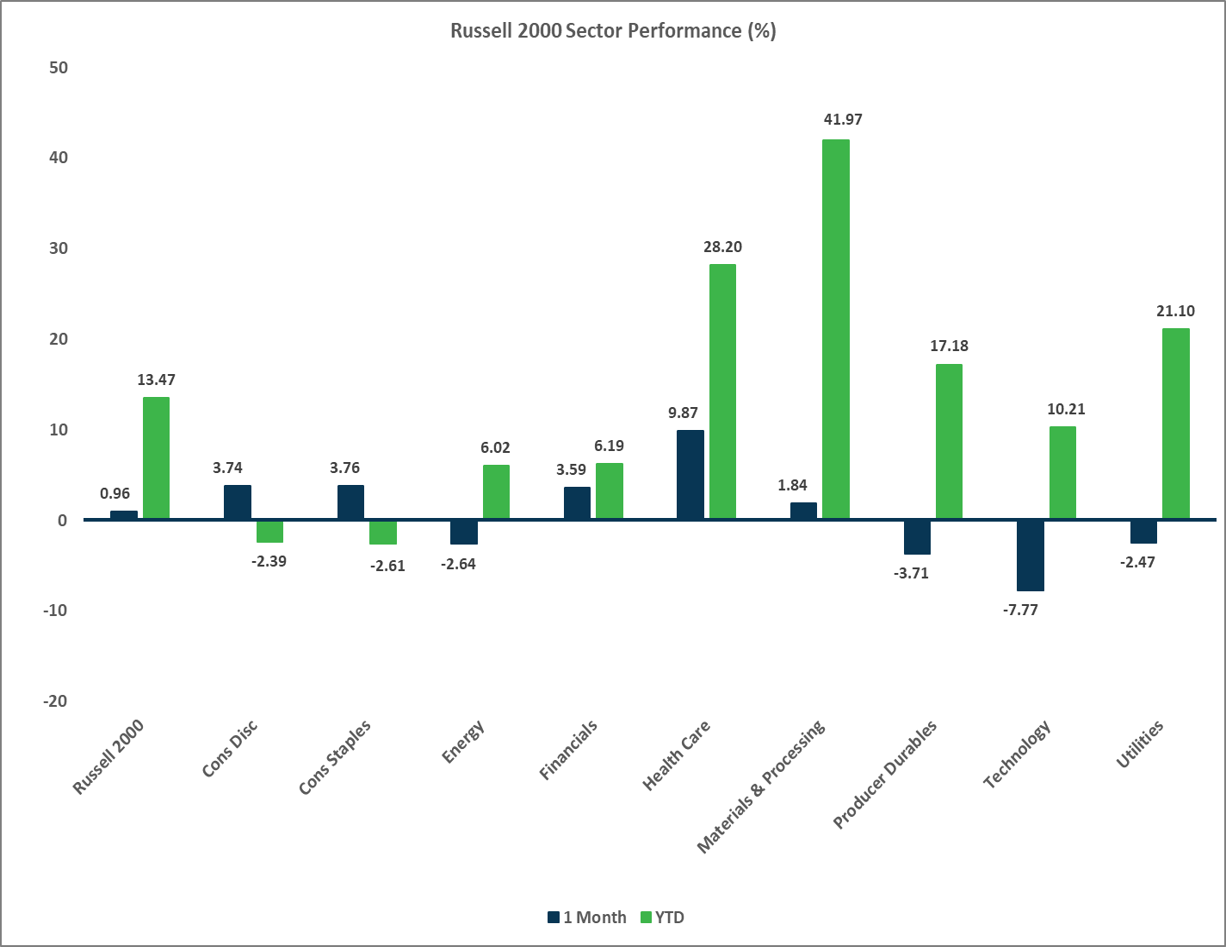

- U.S. equities eked out small gains last month, led by small caps and value stocks.

- U.S. equities lagged other developed markets outside the U.S. in November.

- Small caps beat large caps and value stocks outperformed growth stocks across all market capitalizations.

Non-U.S. Equities

- Stocks outside the U.S. posted modest gains, with some outsized losses from EMs.

- Within EAFE markets, small caps beat large caps and value stocks outpaced growth stocks. Value-driven Europe also outperformed Japan.

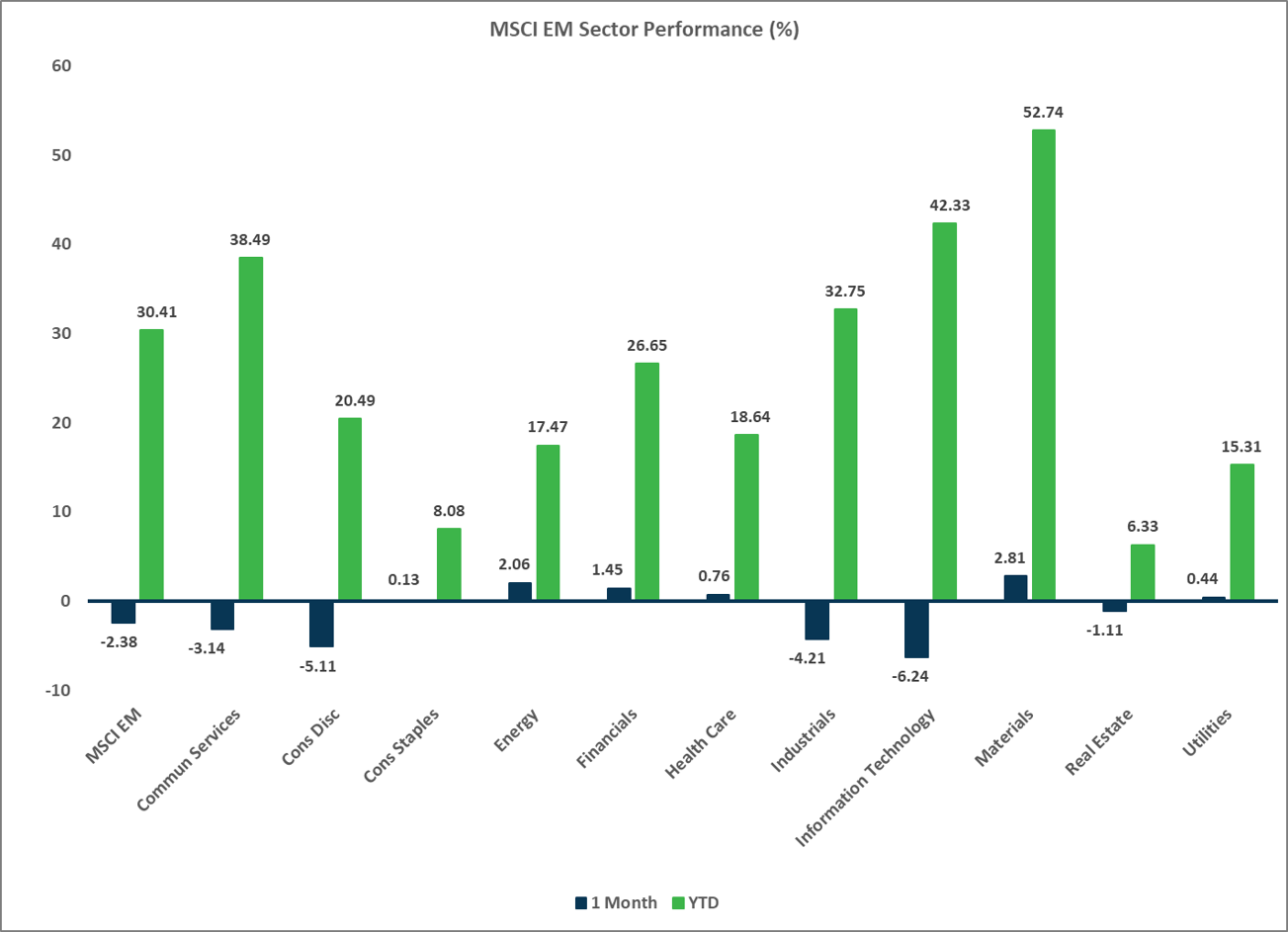

- Within EMs, most of the weakness stemmed from China and other Asian EM countries. EM small caps also fell 1.4%.

- The weaker USD boosted EAFE returns by 7 bps in November, but USD strength versus EM currencies cost EM investors 79 bps.

Sector Performance – S&P 500 (as of 11/30/25)

Sector Performance – Russell 2000 (as of 11/30/25)

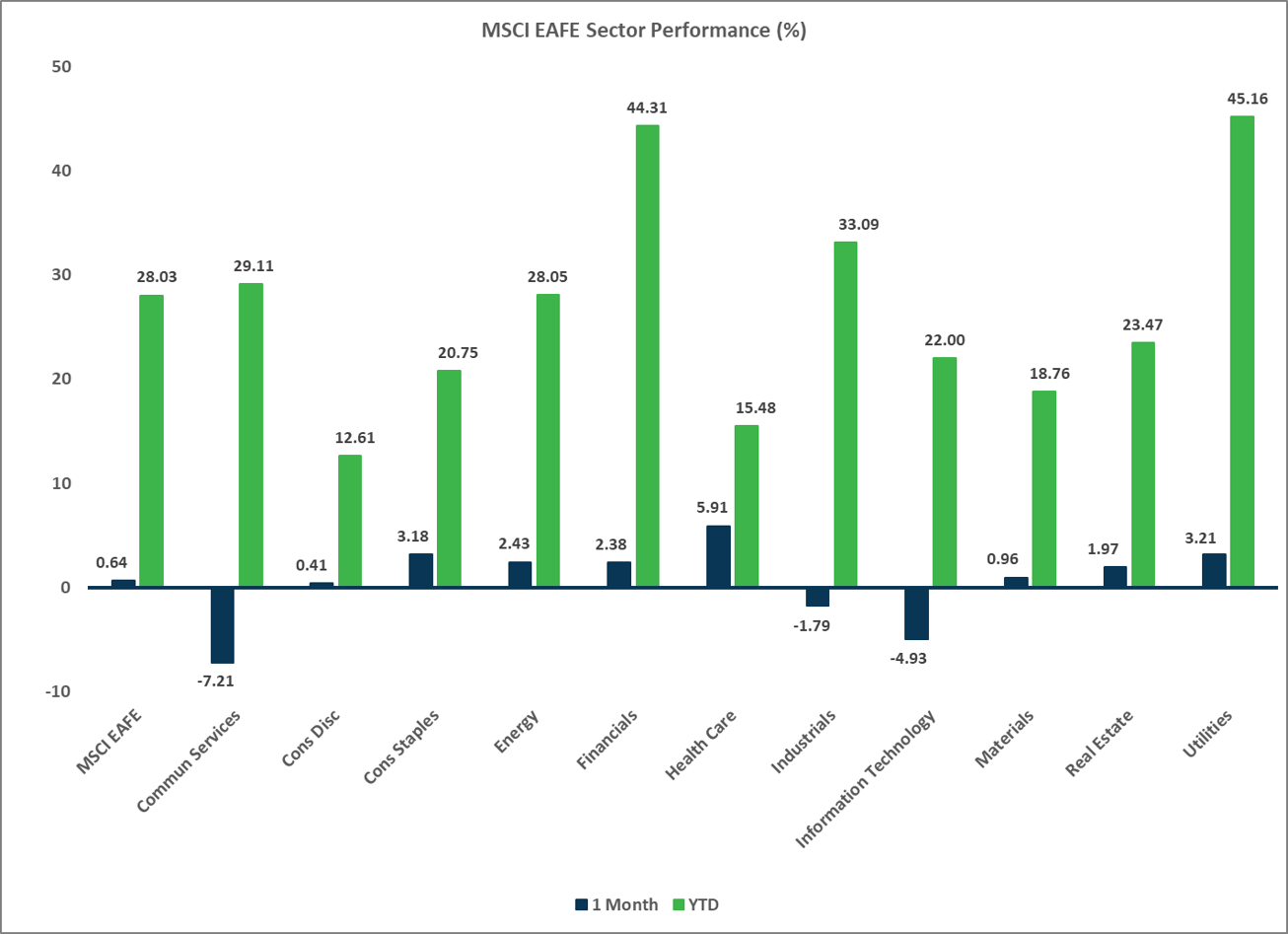

Sector Performance – MSCI EAFE (as of 11/30/25)

Sector Performance – MSCI EM (as of 11/30/25)