Market Flash Report | April 2022

Economic Highlights

United States

- U.S. GDP unexpectedly fell 1.4% in Q1 2022, down sharply from the 7% growth rate reported at the end of 2021. Net exports subtracted a massive 3.2% points from GDP growth, with inventories subtracting an additional 0.8% points. Exports fell by 5.9% annualized while imports increased by 17.7%. The negative contribution from inventories was inevitable after stock building added 5.3% to growth in Q4. The other source of weakness in the first quarter was the public sector, as fiscal support was withdrawn, with government expenditures falling by 2.7%. Positive components of the report included business spending that grew 9.2% and consumer spending which rose 2.7%. The underlying components of the report were fairly solid, but investors should expect volatile inventory and trade numbers moving forward given the state of supply chains and COVID restrictions in key export countries like China. Expectations are currently for 2-2.5% growth in Q2 and 2-3% growth for the full year.

- The Fed hiked rates by 25 bps at its March meeting and they are expected to increase rates by another 50 bps at this week’s May meeting. Markets are forecasting another 125 bps of rate hikes over the next few months to combat out of control inflation. While the Fed needs to act to bring down inflation, we believe they will take a more methodical approach once a few rate hikes are enacted. They want to get rates higher so there is ammunition for a future crisis, but we don’t believe they want to throw the economy into recession. Higher rates will tamp down demand, but it will do nothing to change China’s zero tolerance COVID policy or increase U.S. oil/energy production.

- The decline in the ISM manufacturing index to a 20-month low of 55.4 in April, from 57.1, was mostly due to weakening demand amid a broader slowdown in global manufacturing, rather than a renewed supply crunch. A sharp drop in the employment index to 50.6, from 56.3, was responsible for most of the fall in the headline index. New orders and production softened a bit.

Non-U.S. Developed

- The eurozone economy grew 0.2% Q/Q in Q1 2022, down slightly from the 0.3% rate reported in Q4 2021. Among the Member States for which data are available for Q122, Portugal (+2.6%) recorded the highest increase compared to the previous quarter, followed by Austria (+2.5%) and Latvia (+2.1%). Declines were recorded in Sweden (-0.4%) and in Italy (-0.2%). The Y/Y growth rates were positive for all countries.

- Eurozone economic growth accelerated in April as a rebounding service sector, benefitting from loosened COVID-19 restrictions, helped compensate for a near stalling of manufacturing output. The flash eurozone composite PMI rose from 54.9 in March to

- 55.8 in April. The services component hit an 8-month high while the manufacturing component fell to a 15-month low. While the eurozone economy appears to be on stronger footing to start Q2, it is by no means firing on all cylinders with the manufacturing weakness. Inflation also continues to be a major problem that could start to impact consumer spending and the service sector.

- Japan's government upgraded its view of the economy in April as economists turned more optimistic about the outlook for private consumption following the end of COVID-19 restrictions. The BOJ upgraded its view for economic growth slightly along with its outlook for inflation. The collapse of the the yen towards 2-year lows hurts consumers, but it should benefit export-oriented companies.

Emerging Markets

- China’s economy grew at an annualized clip of 4.8% in Q1, slightly ahead of the 4.4% estimate and down from 2021’s rate. Fixed asset investment for the first quarter rose by 9.3% from a year ago, topping expectations for 8.5% growth. Investment in manufacturing rose by 15.6% in the first quarter from a year ago, and infrastructure saw an 8.5% increase. Retail sales in March fell by a more-than-expected 3.5% Y/Y. With Shanghai and Beijing facing harsh COVID lockdowns/restrictions, China’s economic picture likely worsened in April. One other item to note is the unemployment rate across the country and particularly in large cities which continues to rise. Real estate investment also continues to decline, causing an economic headwind after years of providing a tailwind.

- Unlike the rest of the globe that is tightening monetary policy, China is easing policy to support growth while the government implements its zero tolerance COVID policy. Aa consumers and the real estate sector are challenged, the government will be forced to provide its more traditional set of stimulus tools in the form of infrastructure spending. This does not bode well for an economy looking to transition from manufacturing to services.

- The Caixin China Manufacturing PMI fell to a 26-month low of 46.0 in April of 2022 from March's reading of 48.1. The Caixin China Services PMI plunged to 42.0 in March 2022 from 50.2 in February, the first contraction in seven months and the sharpest fall since February 2020. The official Non-Manufacturing PMI for China sank to 41.9 in April of 2022 from March’s reading of 48.4. This marked the second consecutive month of decline, amid downward pressure from tough COVID-19 measures following outbreaks in many cities, including Shanghai and Beijing. The official manufacturing PMI fell to 47.4 in April from 49.5 in March.

- China’s economy is clearly slowing and struggling with its COVID policy. As the world’s second largest economy, its impact on the global economy is significant. This is especially true for global supply chains that remain severely challenged. As long as major population and production centers are offline in China, supply chain issues should continue.

- According to economists, the Russian economy is forecast to shrink 8.4% in 2022 with inflation soaring to 20.5%. The Russian economy has benefited to some degree by the surprise recovery in the ruble that has allowed central bank policymakers to lower interest rates in response to lower-than-expected inflation. The benchmark interest rate currently sits at 14% and it is expected to decrease to around 10-11% by year end.

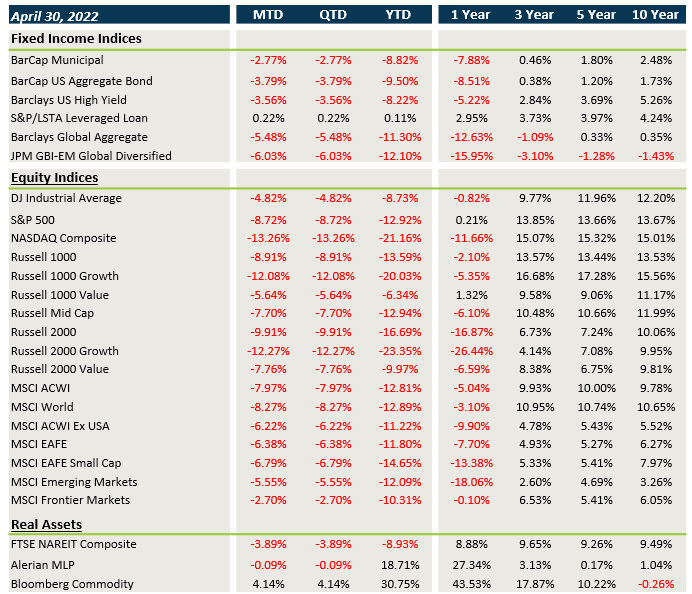

Market Performance (as of 4/30/22)

Fixed Income

- It was another rough month for fixed income with Treasury/.sovereign debt yields moving higher across the board.

- Credit spreads widened in April with risk off sentiment. IG and HY were hit hard while floating rate loans eked out a small gain.

- Bonds outside the U.S. were also hit by the stronger USD.

U.S. Equities

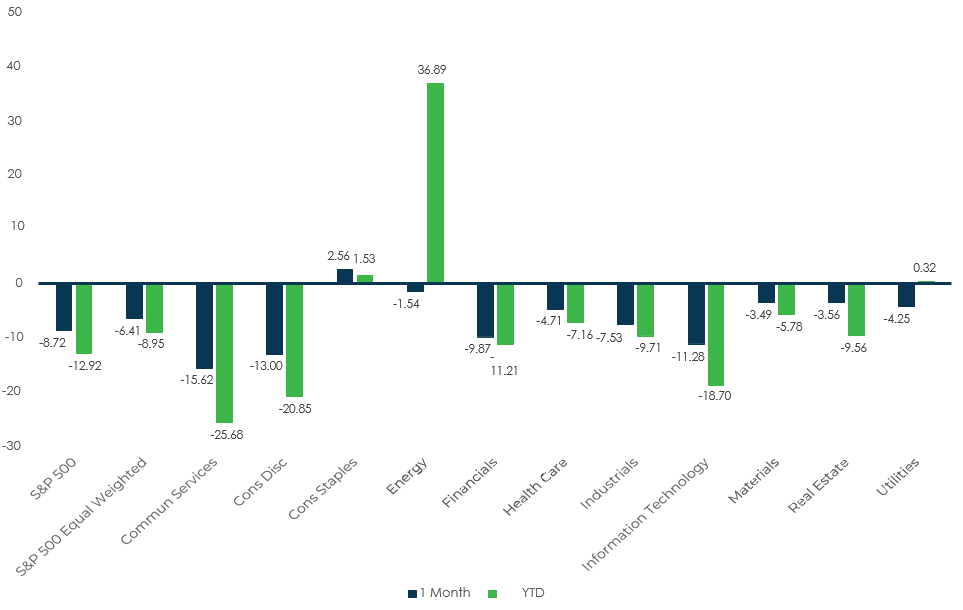

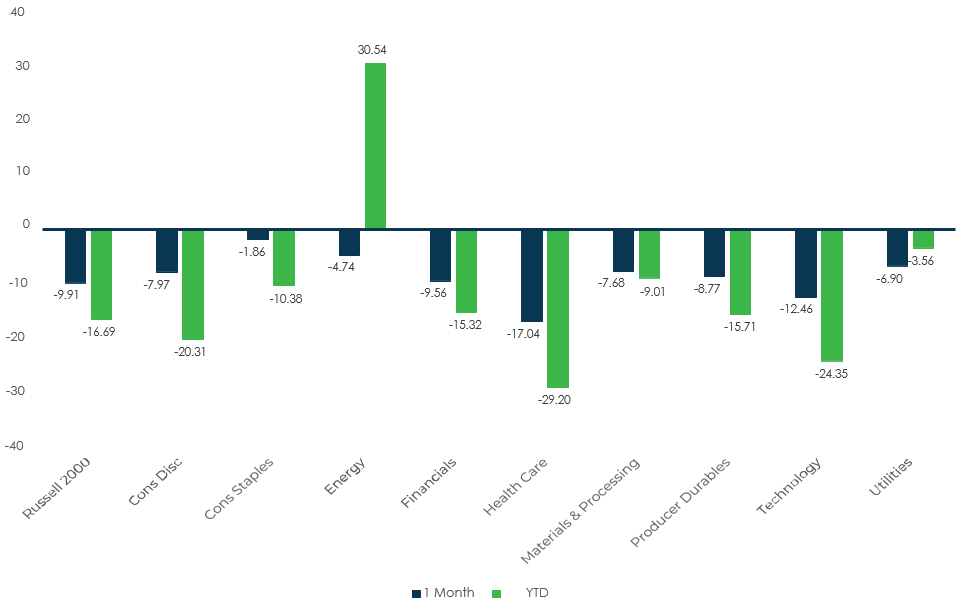

- U.S. equities fell sharply in April led by the Nasdaq/tech/growth.Consumer staples was the only sector that generated positive performance.

- Value trounced growth and the Russell 2000 lagged the Russell 1000.

- The Nasdaq is down 21.2% YTD.

Non-U.S. Equities

- Non-U.S. equities outperformed their U.S. counterparts in April. EAFE markets in particular tend to be value focused so the outperformance is not surprising.

- Outside the U.S., value led growth and large caps slightly beat small caps.

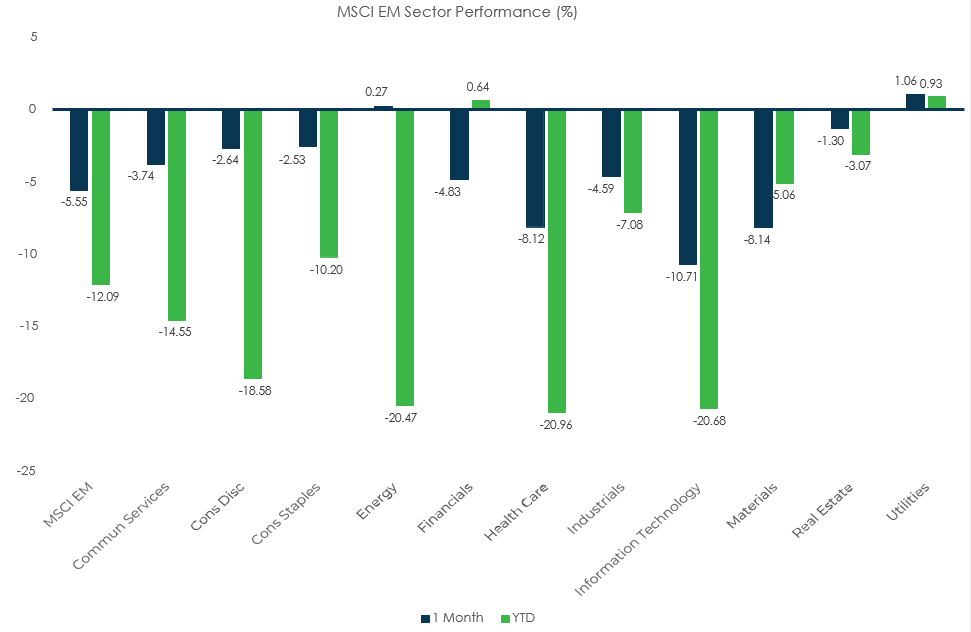

- EMs provide some relative outperformance led by strength in China after months of weakness.

- The strong USD cost investors over 500 bps in EAFE returns and over 200 bps in EM returns.

Sector Performance – S&P 500 (as of 4/30/22)

Sector Performance – Russell 2000 (as of 4/30/22)

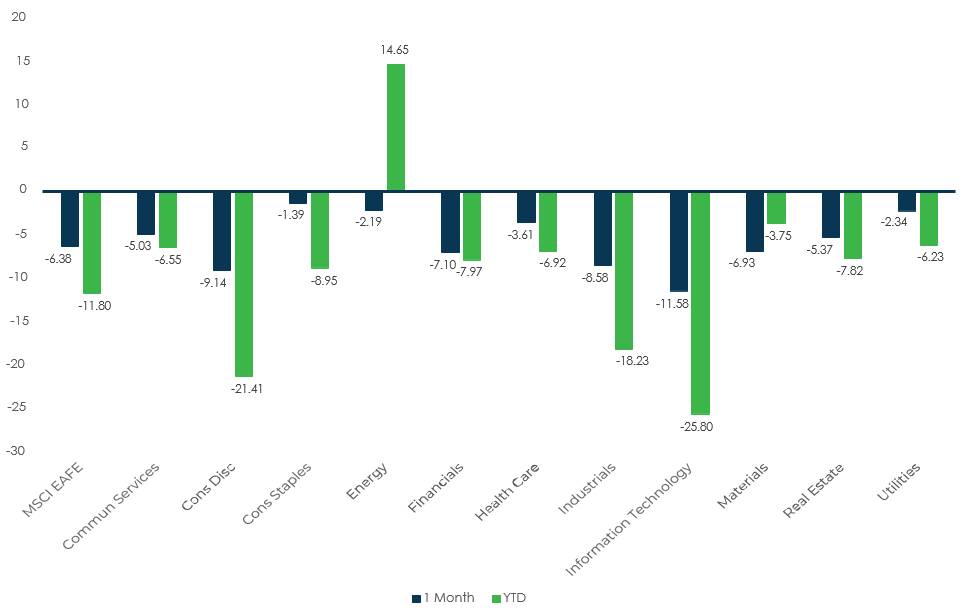

Sector Performance – MSCI EAFE (as of 4/30/22)

Sector Performance – MSCI EM (as of 4/30/22)