Market Flash Report | April 2024

Economic Highlights

United States

- U.S. economic growth slowed in Q1 to a 1.6% annualized rate, below the 2.4% estimate and the higher growth rates posted during the second half of 2023. Consumer spending increased 2.5% in the period, down from a 3.3% gain in Q4 and below the 3% economist estimate. Fixed investment and government spending at the state and local levels helped keep GDP positive on the quarter while a decline in private inventory investment and an increase in imports subtracted. Net exports subtracted 0.86 percentage points from the growth rate while consumer spending contributed 1.68 percentage points.

- The personal consumption expenditures (PCE) price index, a key inflation variable for the Federal Reserve, rose at a 3.4% annualized pace in Q1 2024, its biggest gain in a year and up from 1.8% in Q4 2023. Excluding food and energy, core PCE prices rose at a 3.7% rate, both were well above the Fed’s 2% target. A similarly “hot” consumer price index (CPI) reading last month confirmed that inflation was generally heading in the wrong direction through the first few months of 2024.

- Slowing growth and hotter-than-expected inflation presents a further conundrum for the Fed in terms of monetary policy. While it has attempted to tighten monetary policy over the past 2 years, the surge in fiscal spending has provided a counterbalance. Growth has held up, largely fueled by stimulus and government spending, but inflation has remained sticky. Any rate cuts by the Fed may not occur until the end of 2024 or perhaps Q1 of 2025, but we continue to believe the Fed is data dependent and things can change quickly based on new economic data.

- Retail sales jumped 0.7% in March, well ahead of the 0.3% estimate, but below the upwardly revised 0.9% gain in February. Retail sales ex autos and the control group measure both rose 1.1% in March. Online sales and gas station receipts were the strongest gainers compared to sporting goods, clothing stores and electronics and appliances. New orders for durable goods increased 2.6% (1.3% y/y) during March, after rising 0.7% in February, revised from 1.4%. The March gain in new orders reflected a 23.7% rise in aircraft orders after they increased 13.9% in February.

Non-U.S. Developed

- Business activity in the euro region grew at the fastest rate in nearly a year in April. The improvement indicates that the region continues to pull out of the recent downturn, albeit growing only modestly amid divergent sector performances. Increasingly robust service sector growth was accompanied by signs of a further moderation of the manufacturing downturn. The headline composite PMI hit an 11-month high while the manufacturing PMI softened to a 4-month low. Services continue to buoy the eurozone economy, with expectations for a 0.3% expansion in Q2 growth.

- Inflation in the eurozone eased to 2.4% in March, boosting expectations for interest rate cuts to begin in the summer. The core rate of inflation, excluding energy, food, alcohol and tobacco, cooled from 3.1% to 2.9%, also coming in below expectations. However, inflation in services remained stuck at 4% for a fifth straight month, pointing to continued pressure from wage growth.

- Japan’s core inflation slowed in March due to mild increases in food prices, but remained comfortably above the Bank of Japan’s (BOJ) 2% target. CPI rose 2.6% in March, after increasing 2.8% in February. Core CPI rose 2.9%, marking the first time since November 2022 that it fell below 3%. The BOJ seemed poised to hike rates with this string of higher inflation, but any declines could increase uncertainty.

Emerging Markets

- Growth in China surprisingly accelerated in Q1, driven by external demand. Q1 GDP surged 5.3%, above the 4.6% economist expectation and the 5.2% expansion in the fourth quarter of 2023. Export volume jumped 14% Y/Y in Q1, but property investments in the embattled real estate sector fell 9.5%. The People’s Bank of China has been providing a lot of stimulus and support for the Chinese economy over the past year to combat sluggish growth, deflation and real estate woes.

- Industrial output for March grew 4.5% Y/Y, missing expectations of 6%. Retail sales grew 3.1% Y/Y, lower than expectations of 4.6%. Fixed asset investment grew an annual 4.5% over the first three months of 2024, versus expectations for a 4.1% rise and after expanding 4.2% in the January-February period.

- Economic growth in India surpassed already lofty expectations to end 2023. Its GDP jumped 8.4% in Q4, well ahead of expectations and the 7.6% rise reported in the prior quarter. India is also widely seen as an alternative to China for countries and companies looking to diversify their supply chains, particularly as the relationship between the U.S. and China sours. Prime Minister Narendra Modi’s government has been actively courting multi-national firms to set up factories in the country, as it spends billions to upgrade roads, ports, airports and railways.

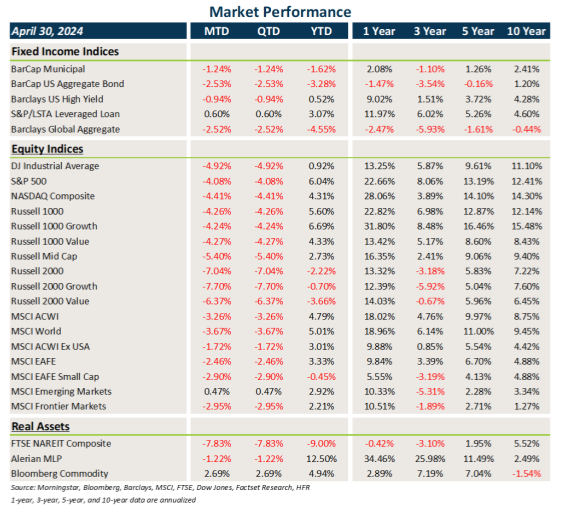

Market Performance (as of 04/30/24)

Fixed Income

- Treasury and other sovereign debt yields surged higher in April, resulting in losses across core fixed income and municipal bonds.

- Credit weathered the backup in rates a bit better, but still lost ground with some spread-widening.

- The short duration properties of floating rates loans provided some protection against losses.

- USD strength was a headwind for non-U.S. assets.

U.S. Equities

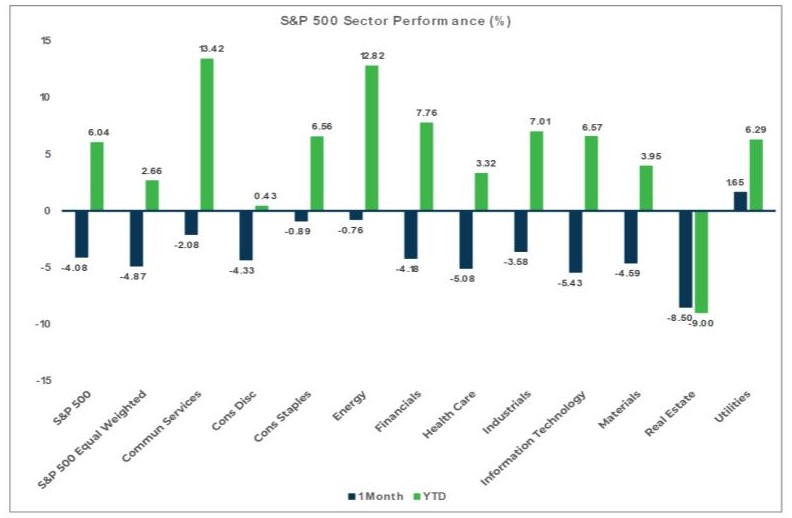

- U.S. equities fell in April, after rallying higher for the past six months.

- Large caps handily outperformed small caps last month, but there was little dispersion between growth and value within large caps.

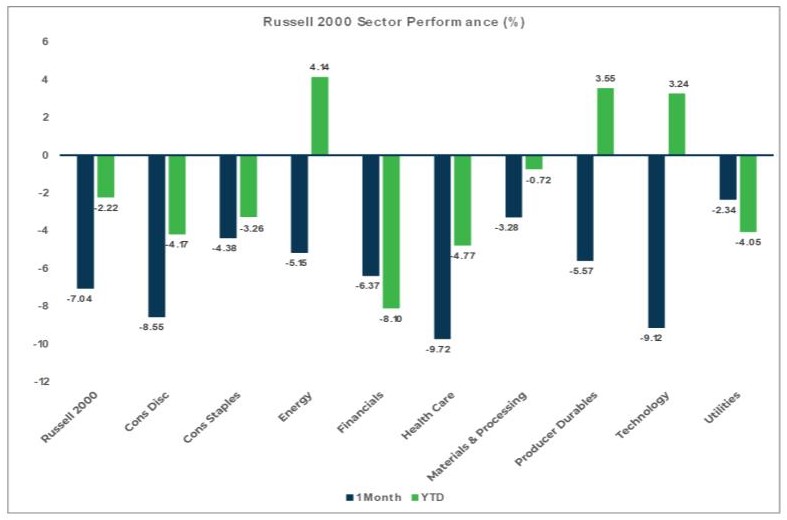

- Small caps were particularly weak in April, with growth losing ground to value.

Non-U.S. Equities

- Non-U.S. equities fell in April, but generally held up better than U.S. equities.

- There was little dispersion between large caps and small caps within EAFE equities.

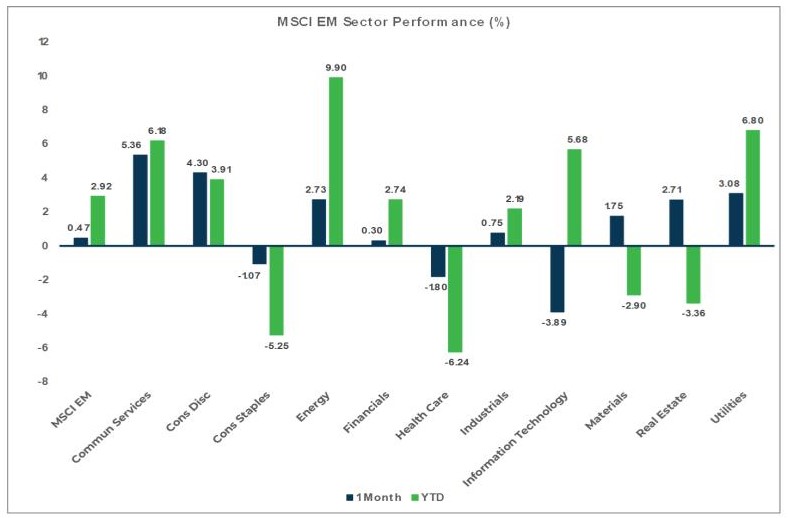

- With positive performance, emerging market equities stood out last month.

- USD strength was a small detractor to non-U.S. equity returns.

Sector Performance - S&P 500 (as of 04/30/24)

Sector Performance - Russell 2000 (as of 04/30/24)

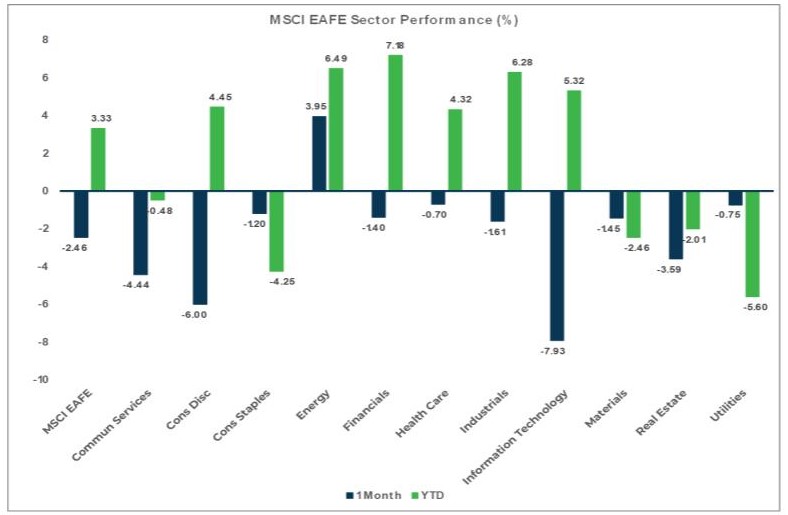

Sector Performance - MSCI EAFE (as of 04/30/24)

Sector Performance - MSCI EM (as of 04/30/24)