Market Flash Report | April 2025

Economic Highlights

United States

- U.S. GDP fell at a 0.3% annualized pace in Q1, largely pushed by a surge in imports ahead of President Donald Trump’s tariffs. Imports soared 41.3%, driven by a 50.9% increase in goods. Imports subtract from GDP, so the contraction in growth may not be viewed as negatively, given the potential for the trend to reverse. This was the first quarter of negative growth since Q1 of 2022. A slowdown in consumer spending (+1.8%) and a sharp decline in federal outlays (-5.1%) also contributed to the weak GDP reading.

- All eyes will be on the April employment report due out on May 2. The ADP Private Sector job growth report showed only 62,000 new jobs being added to the U.S. economy last month, well below the 120,000 estimate and 147,000 March reading. Economists expect job growth of 135,000 and the unemployment rate to hold steady at 4.2% in the official employment report.

- Prices fell more than anticipated in March, with headline Consumer Price Index (CPI) falling to an annualized rate of 2.4%, down from 2.8% in February. Core CPI, which excludes volatile food and energy, fell from 3.1% in February to 2.8% in March. Slumping energy prices helped keep inflation tame as a 6.3% drop in gasoline prices helped drive a 2.4% broader decline in the energy index. Shelter prices gained only 0.2% last month and used car prices declined 0.7%. Food prices rose 0.4% M/M. Rate cut expectations by the Federal Reserve have been all over the place in recent weeks, but as of May 1, markets are pricing in 4-5 rate cuts in 2025 with the first one likely occurring in June.

- Retail sales surged 1.4% in March, ahead of the 1.2% estimate. Excluding autos, the numbers also were stronger than expected, with sales up 0.5% compared with the 0.3% forecast. The retail sales numbers were strong and suggest robust spending ahead of looming tariffs and potential higher prices. Core retail sales grew 0.4% in March, but a slowdown is forecast.

- Durable goods orders surged 9.2% in March, the third straight monthly gain. The sharp uptick was largely driven by a rush in orders for commercial aircraft. Transportation equipment jumped 27%, mainly nondefense aircraft and parts (139%) and motor vehicles and parts (2.3%). Orders for non-defense capital goods excluding aircraft, a closely watched proxy for business spending plans, edged up 0.1%

Non U.S. Developed

- The eurozone flash composite PMI fell to 50.1 in April, slightly below consensus expectations. Services activity fell to 49.7, whereas the manufacturing index edged up to 48.7 despite trade headwinds. Business activity in Germany decreased for the first time in four months and France remained in contraction territory. The rest of the eurozone continued to record solid growth of output. This report points to stagnation although higher defense spending should provide benefits over time.

- Inflation in the eurozone fell slightly in March. CPI fell from 2.3% in February to 2.2% in March, and core CPI declined from 2.6% to 2.4%. The unemployment rate fell to 6.1% in February.

- Trade uncertainty is having an impact on the Japanese economy. The Bank of Japan slashed its GDP growth forecast for the year from 1.1% to 0.5%. Trade uncertainties also provided justification for the BOJ to hold interest rates steady at 0.5%. Japan is currently negotiating a new trade deal with the U.S. after exporting $150B of goods last year.

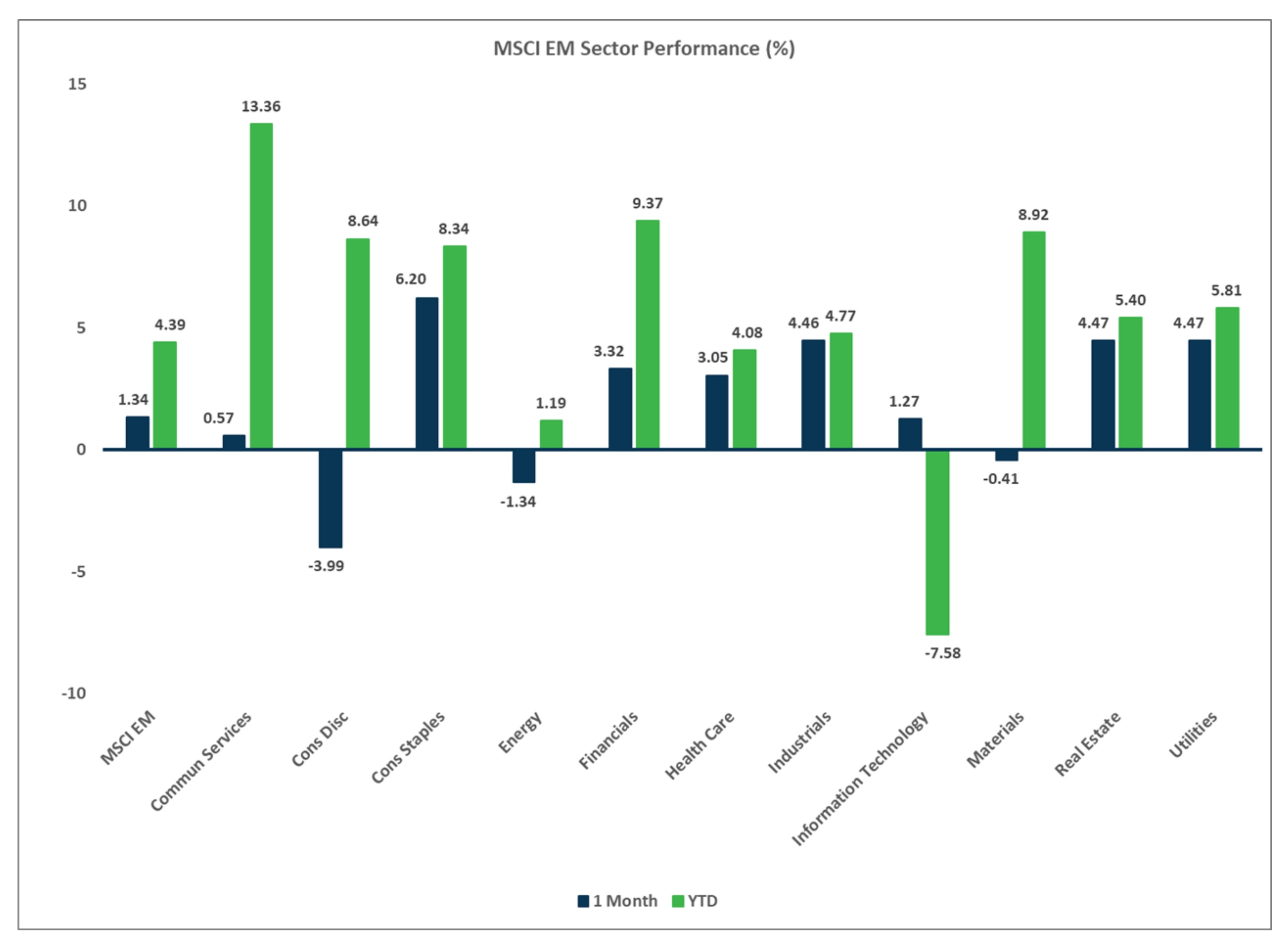

Emerging Markets

- China’s economy is starting to show signs of stress due to the ongoing uncertainty over tariffs and trade policy. The official manufacturing PMI fell back into contraction territory in April, with a reading of 49.0 (down from 50.5 in March). A measure of new export orders plunged, sinking to 44.7 in April, the lowest reading since December 2022. This is perhaps an early sign that trade between the U.S. and China is in danger of drying up, as U.S. importers cancel or delay orders after a rush to bring in goods earlier this year before tariffs came into effect. According to a Goldman Sachs report, one-third of China’s 2024 growth came from exports and an estimated 10-20 million manufacturing workers are dependent on U.S. trade/exports.

- The official China non-manufacturing PMI fell to 50.4 in April from 50.8 in the previous month. Consumer prices in China fell for a second straight month in March, largely due to the ongoing trade uncertainty with the U.S. that could exert further downward pressure on prices. CPI fell 0.1% Y/Y in March after declining 0.7% in February. Core inflation, which excludes volatile food and fuel prices, rose 0.5% in March, rebounding from a 0.1% decrease in February.

- The International Monetary Fund (IMF) lowered its 2025 forecast for global growth from 3.3% to 2.8%. They also lowered their GDP growth forecast for 2026 to 3%. U.S. economic growth will come in at just 1.8% this year, down sharply from its previous forecast of 2.7%. China is also forecast to grow more slowly because of U.S. tariffs. The IMF now expects it will expand 4% this year, down from the previous estimate of 4.5%. The eurozone is expected to grow 0.8% in 2025 while Japan’s rate of growth was slashed to just 0.6%.

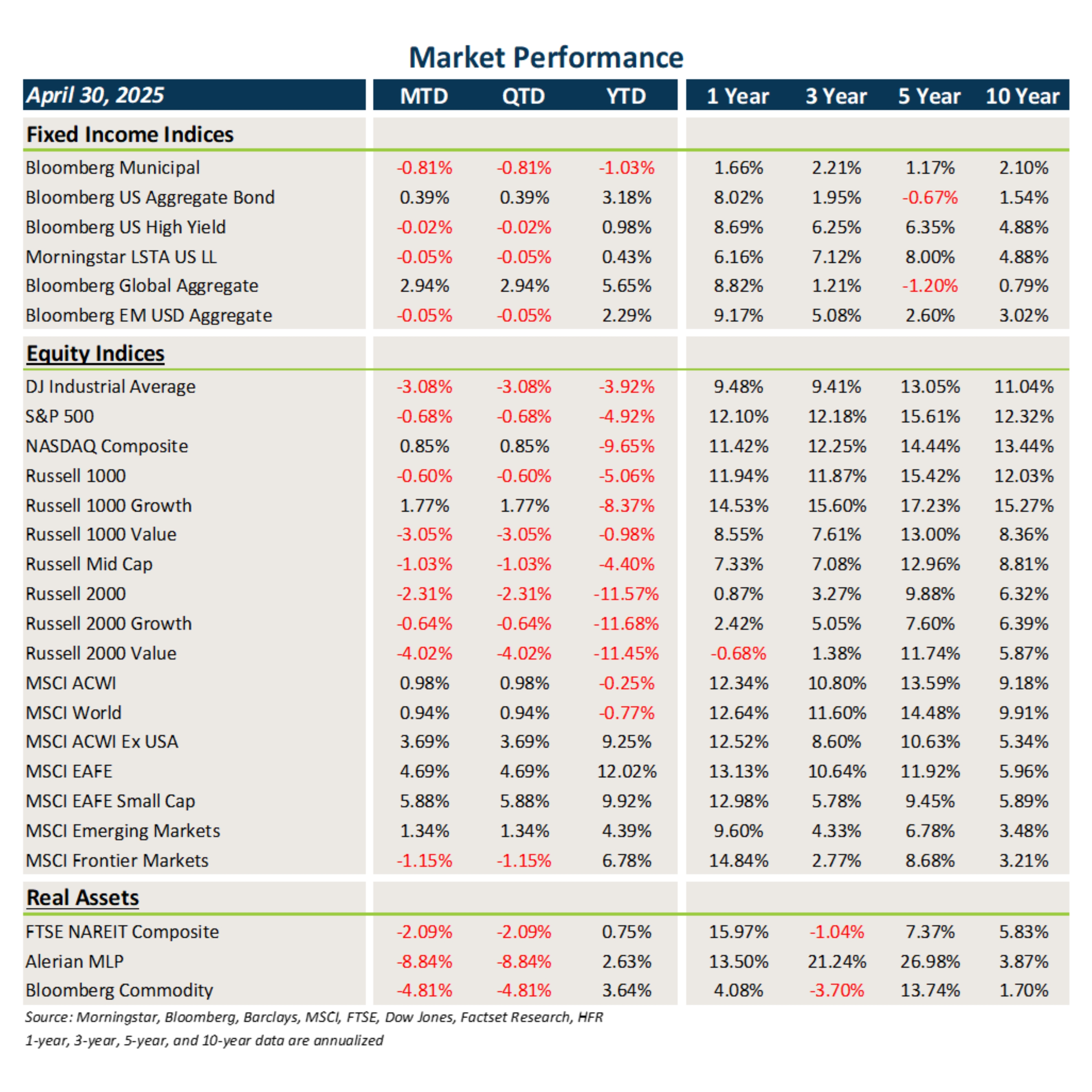

Fixed Income

- Treasury and other sovereign debt yields trended lower in April, leading to gains in core fixed income. Munis continued to suffer losses due to technical headwinds like higher issuance.

- Credit spreads were volatile throughout April, ultimately leading to modest losses in high- yield bonds, loans and earnest money deposits.

- Bonds outside the U.S. benefited from the sharp decline in the USD.

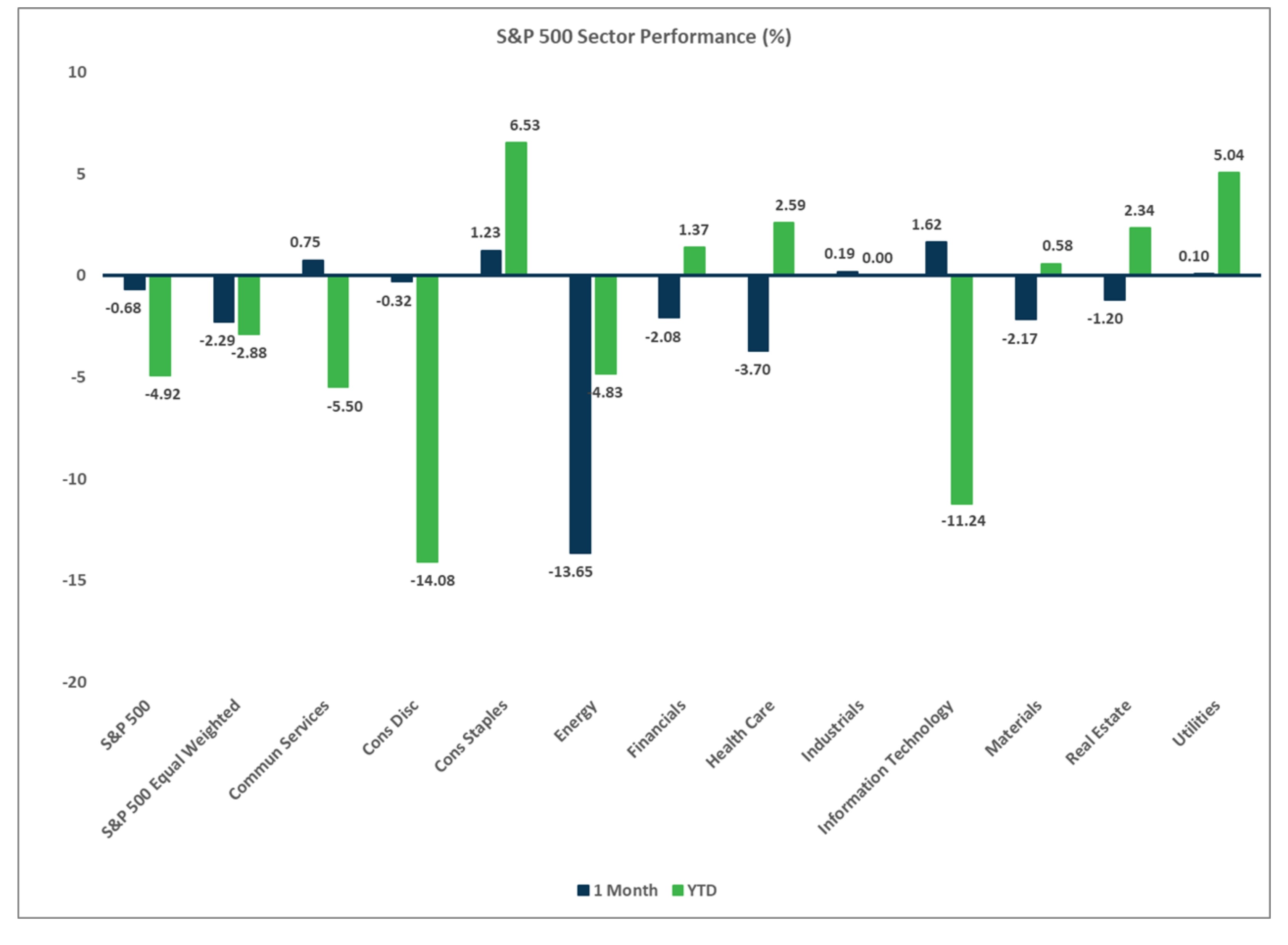

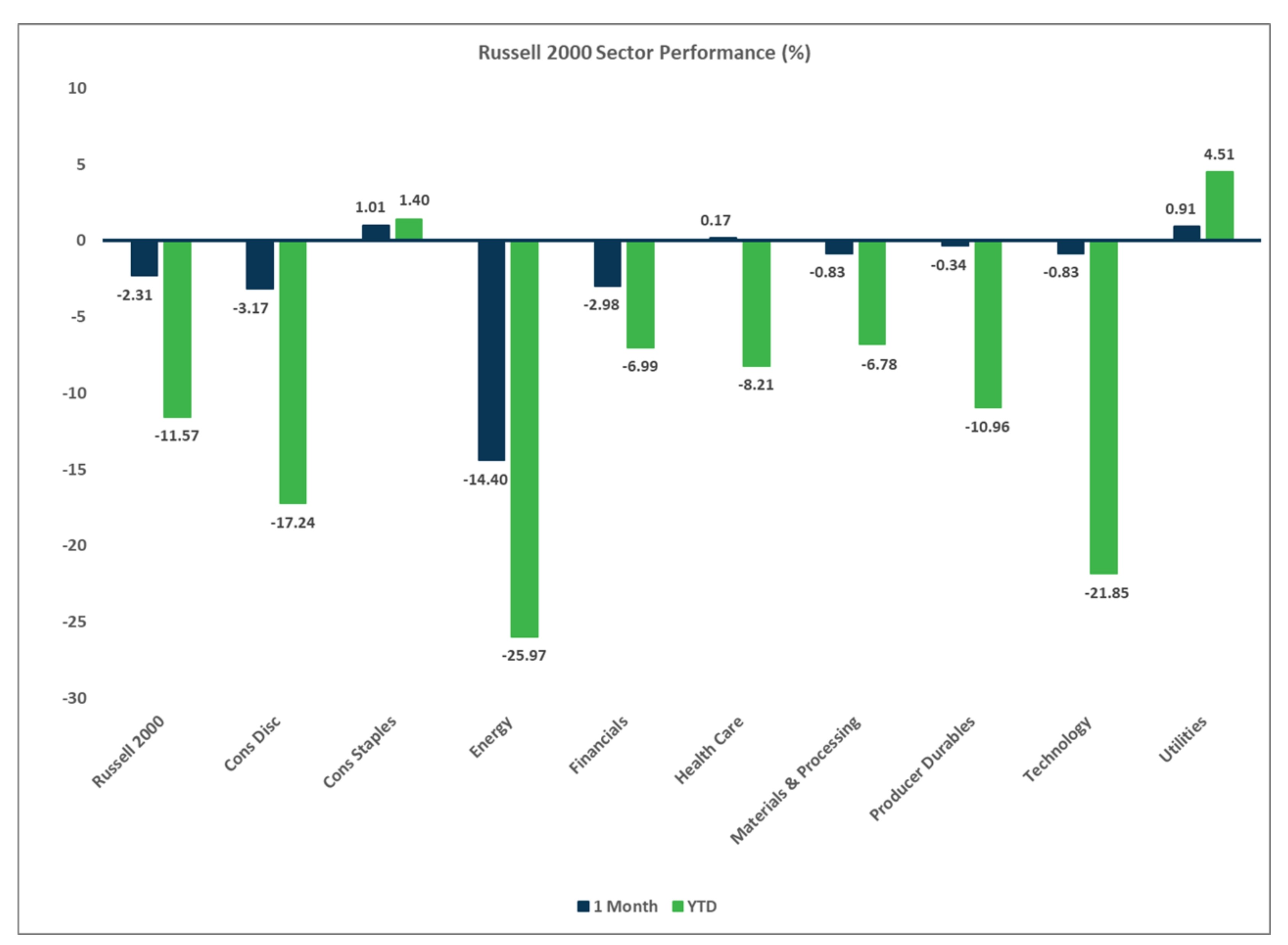

U.S. Equities

- U.S. equities faced extreme volatility and weakness after “Liberation Day,” but most losses were recouped during the last two weeks of April.

- Growth ended up beating value across all market capitalizations and small caps lagged large caps.

- Although there has been a lot of noise and anxiety in financial markets this year, it is important to note that the S&P 500 is only down 4.9% YTD.

Non U.S. Equities

- Developed markets outside the U.S. posted solid gains in April, fueled by defense stocks and financials.

- Unlike what occurred in the U.S., small caps beat large caps within EAFE markets. Growth managed to outperform value in April.

- Emerging Market (EM) equities underperformed last month due to weakness in China.

- USD weakness added 466 bps to EAFE returns and 152 bps to EM returns.

Sector Performance - S&P 500 (as of 04/30/25)

Sector Performance - Russell 2000 (as of 04/30/25)

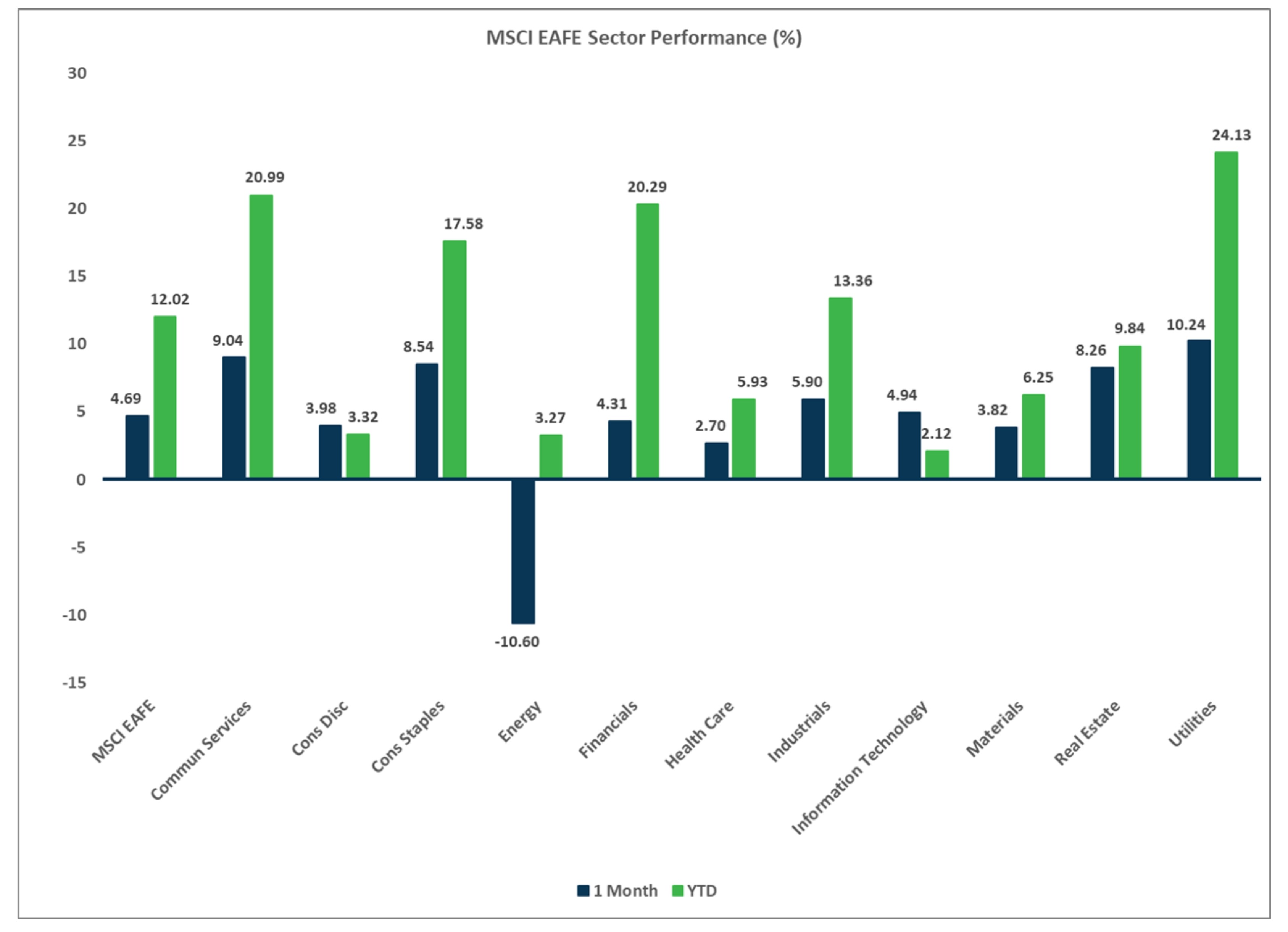

Sector Performance - MSCI EAFE (as of 04/30/25)

Sector Performance - MSCI EAFE (as of 04/30/25)