Market Flash Report | June 2025

Economic Highlights

United States

- The May employment report was better than anticipated with 137,000 new jobs added to the economy, ahead of the 125,000 estimate. The unemployment rate held steady at 4.2%, and the March and April reports were revised lower by a total of 95,000 jobs. Worker pay grew more than expected, with average hourly earnings up 0.4% during the month and 3.9% from a year ago. The broader U6 unemployment rate was also unchanged at 7.8%. The healthcare sector accounted for nearly half the job growth (+62,000) while the federal government shed 22,000 jobs.

- The Personal Consumption Expenditure (PCE) index, the Federal Reserve’s (the Fed’s) primary inflation reading, rose a seasonally adjusted 0.1% for the month, putting the annual inflation rate at 2.3%. Excluding food and energy, core PCE posted readings of 0.2% and 2.7%, compared with estimates for 0.1% and 2.6%. Consumer spending and income showed further signs of weakening. Spending fell 0.1% M/M while personal income declined 0.4%.

- U.S. retail sales growth slowed sharply in April, as the boost from front-loaded purchases faded. Retail sales rose 0.1% after surging 1.7% in March. Core retail sales declined 0.2% after rising 0.5% in March. Sales fell at auto dealerships and sporting goods stores, but rose at online retail and bars and restaurants. Retail sales grew 5.2% Y/Y in April. Durable goods orders surged 16.5% in May, well ahead of expectations and April’s downward reading. The reason for the stronger-than-expected reading was a substantial increase in transportation equipment. Excluding that, orders were up 0.5%.

- June’s ISM Manufacturing Purchasing Manager’s Index (PMI) edged up to 49.0 from 48.5 in May. Although the production component surged higher, the report showed weakness in new orders and employment. Many companies cited the chaos with tariffs and the Middle East as reasons for recent manufacturing weakness.

Non U.S. Developed

- The eurozone flash composite PMI remained steady at a headline reading of 50.2 in June (unchanged from May). Services hit a two-month high of 50.0, while manufacturing was unchanged at 49.4. Most of the growth over the past few months has come from the manufacturing sector, compared to the service sector which has remained largely stagnant. France deteriorated again, in terms of activity, although Germany rejoined the rest of the eurozone in expansion territory. Current PMIs suggest sluggish growth again for the eurozone economy in Q2.

- Eurozone inflation hit the ECB’s target of 2% in June, up slightly from the 1.9% reading in May. Core inflation, which excludes energy, food, tobacco and alcohol prices, was unchanged at 2.3% in June. Inflation has fallen more in the eurozone compared to the U.S. and this has allowed the ECB to cut rates more aggressively over the past year.

- Business sentiment among large Japanese manufacturers has improved slightly, according to the recent Tankan survey released by Japan’s central bank, although worries persist over President Trump’s tariffs. The U.S. has imposed 25% tariffs on auto imports. Japanese automakers have plants in Mexico, where Trump has announced a separate set of tariffs. The U.S. has also imposed 50% tariffs on steel and aluminum. The BOJ has raised its key borrowing rate from 0.1% at the start of the year to 0.5% today.

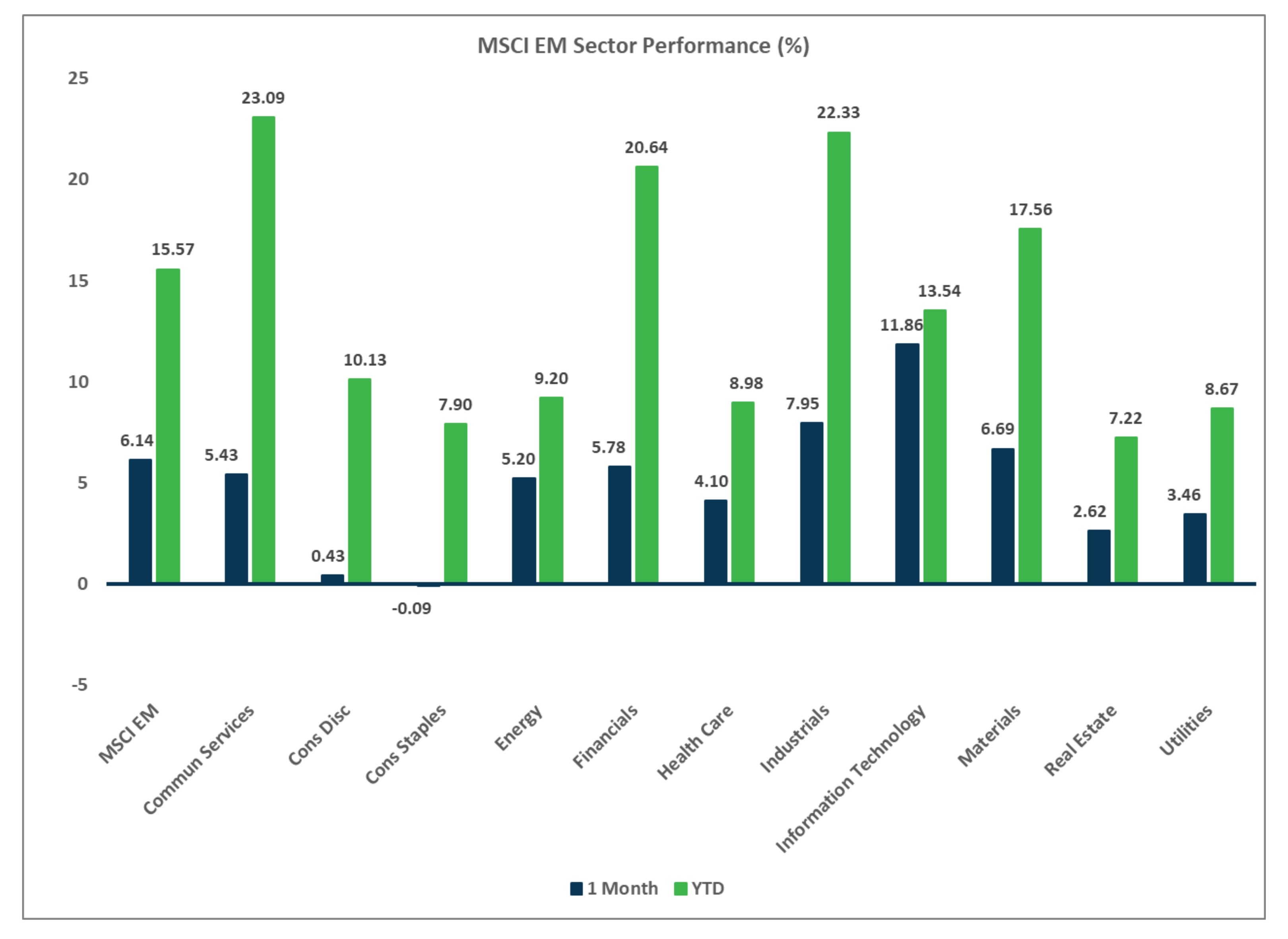

Emerging Markets

- China’s manufacturing sector continues to show a mixed bag based on recent PMI readings. The smaller company focused Caixin/S&P Manufacturing PMI came in at 50.4 in June, up from 48.3 in the previous month. The official manufacturing PMI posted a reading of 49.7 in June, compared to 49.5 in May. Production and new orders strengthened in June while employment at factories and inventories weakened.

- The official non-manufacturing PMI, which includes services and construction, rose to 50.5 in June from 50.3 in May. The services sub-index slipped to 50.1 while construction accelerated to 52.8, driven by infrastructure project spending.

- The PBOC continues to emphasize consumption growth as the key to sustainable economic expansion for China over the long run, but that has failed to materialize in a meaningful way in recent years. Gross Domestic Product (GDP) growth continues to be fueled by infrastructure spending and exports, as opposed to consumer spending. Producer prices are mired in a deflationary spiral that has hurt manufacturers and led to deflation in consumer prices. Additional stimulus appears likely from the Chinese government to boost consumer demand/spending.

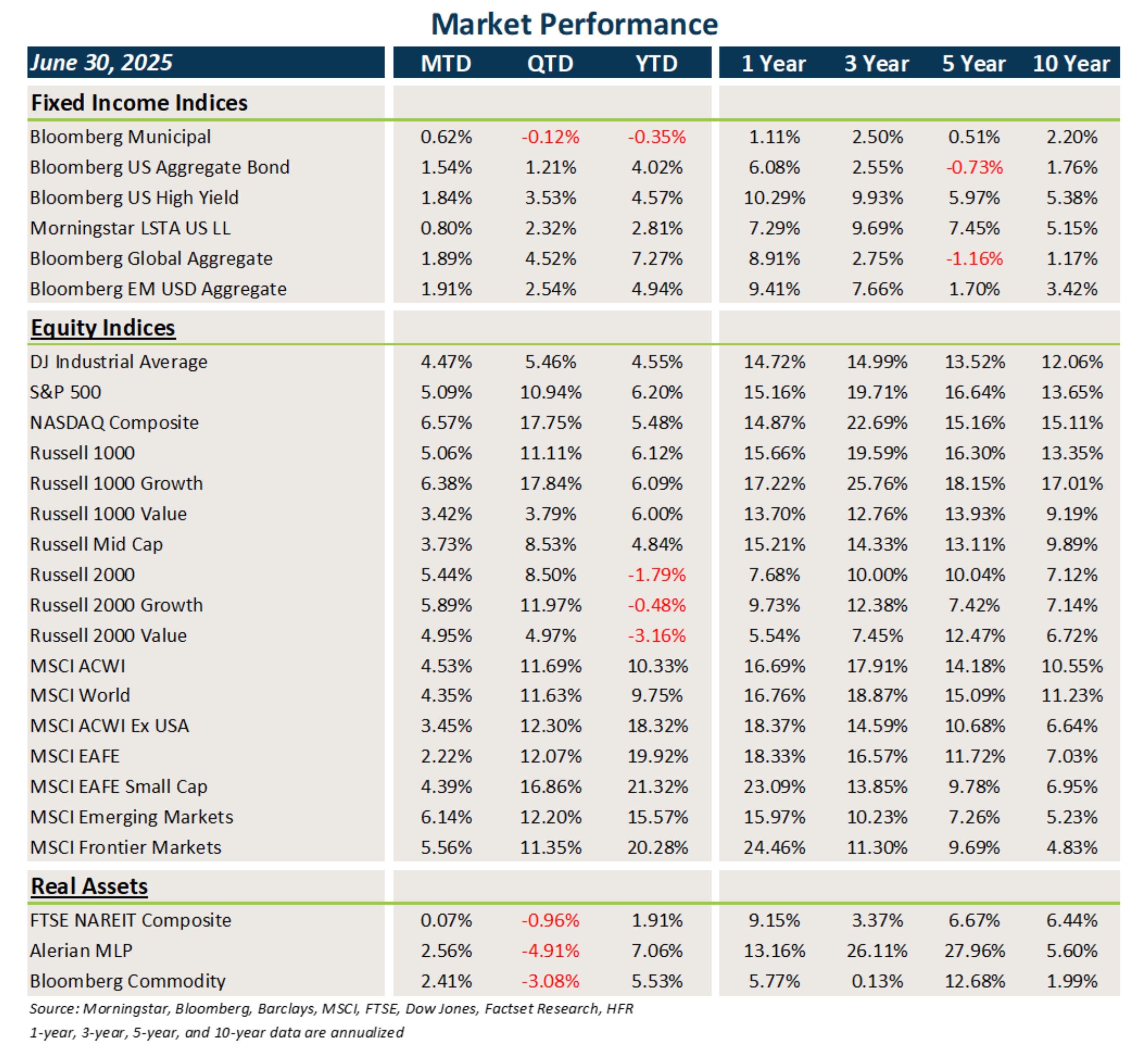

Fixed Income

- Interest rates trended lower throughout June, leading to gains in core fixed income and municipal bonds (munis). After months of poor technicals, munis benefited from better supply-demand characteristics.

- Credit posted another solid month, with investors benefiting from clipping higher coupons.

- The weaker U.S. dollar continued to provide a nice tailwind for non-U.S. assets.

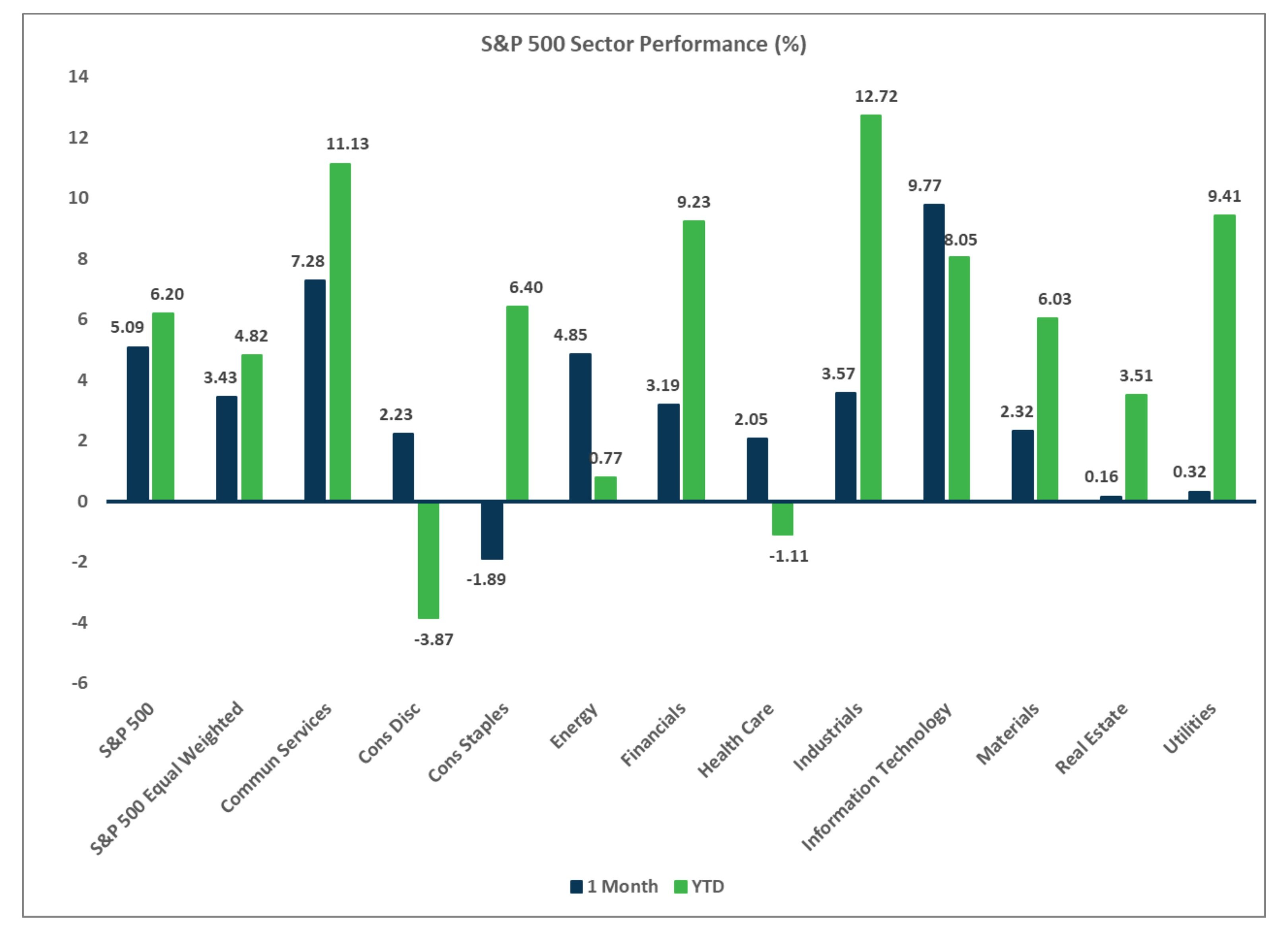

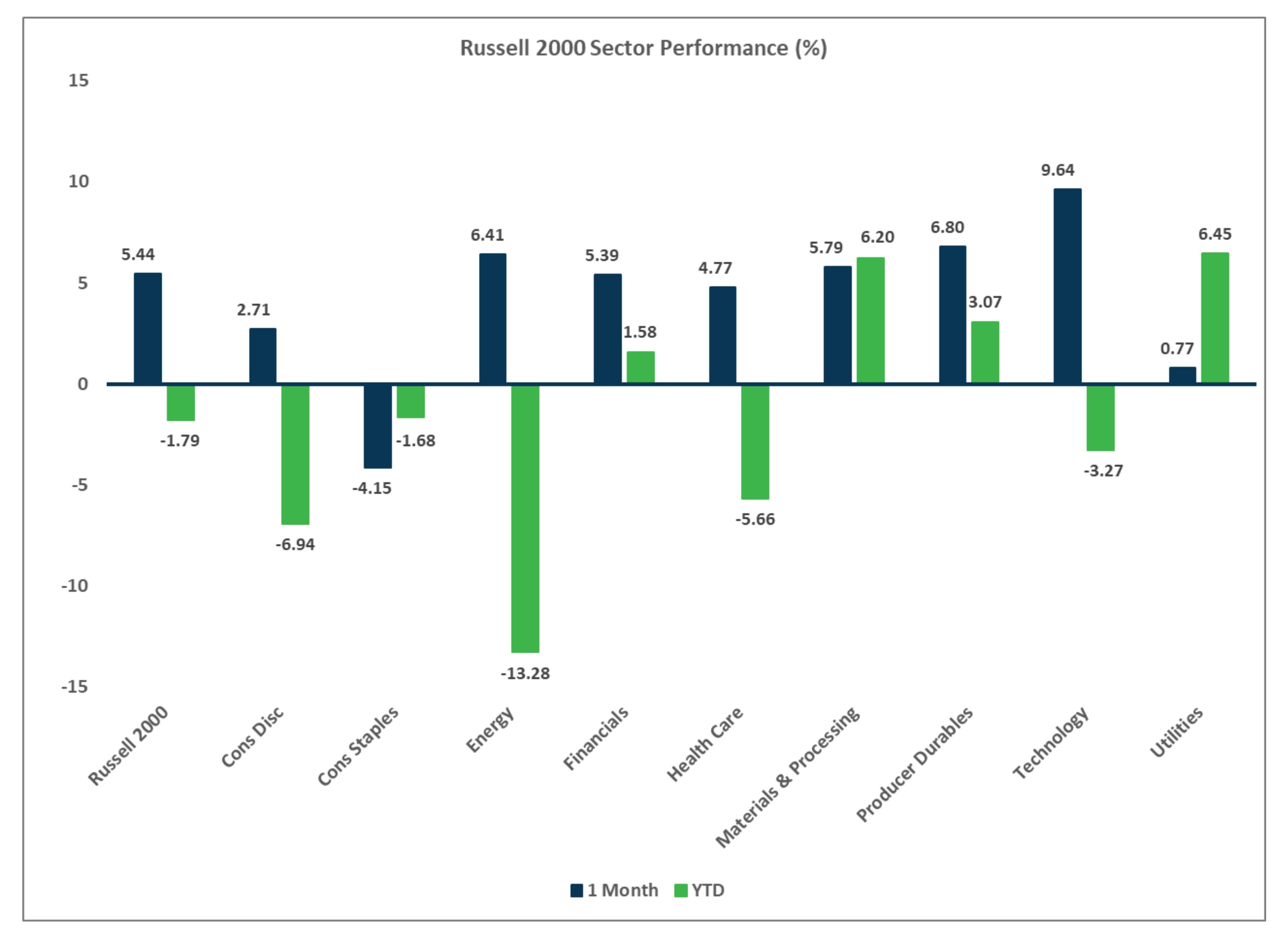

U.S. Equities

- U.S. equities ended June on a high note with strong gains across the board.

- Growth beat value across all market capitalizations and small caps outpaced large caps for the month.

- Volatility has been very high in 2025, but the S&P 500 has managed to gain 6.2% YTD.

Non U.S. Equities

- Developed markets outside the U.S. posted solid returns last month, but underperformed their U.S. counterparts.

- EMs outperformed EAFE equities in June, driven by strong gains in LatAM and Eastern Europe.

- Similar to what occurred in the U.S., small caps outpaced large caps and growth beat value.

Sector Performance - S&P 500 (as of 06/30/25)

Sector Performance - Russell 2000 (as of 06/30/25)

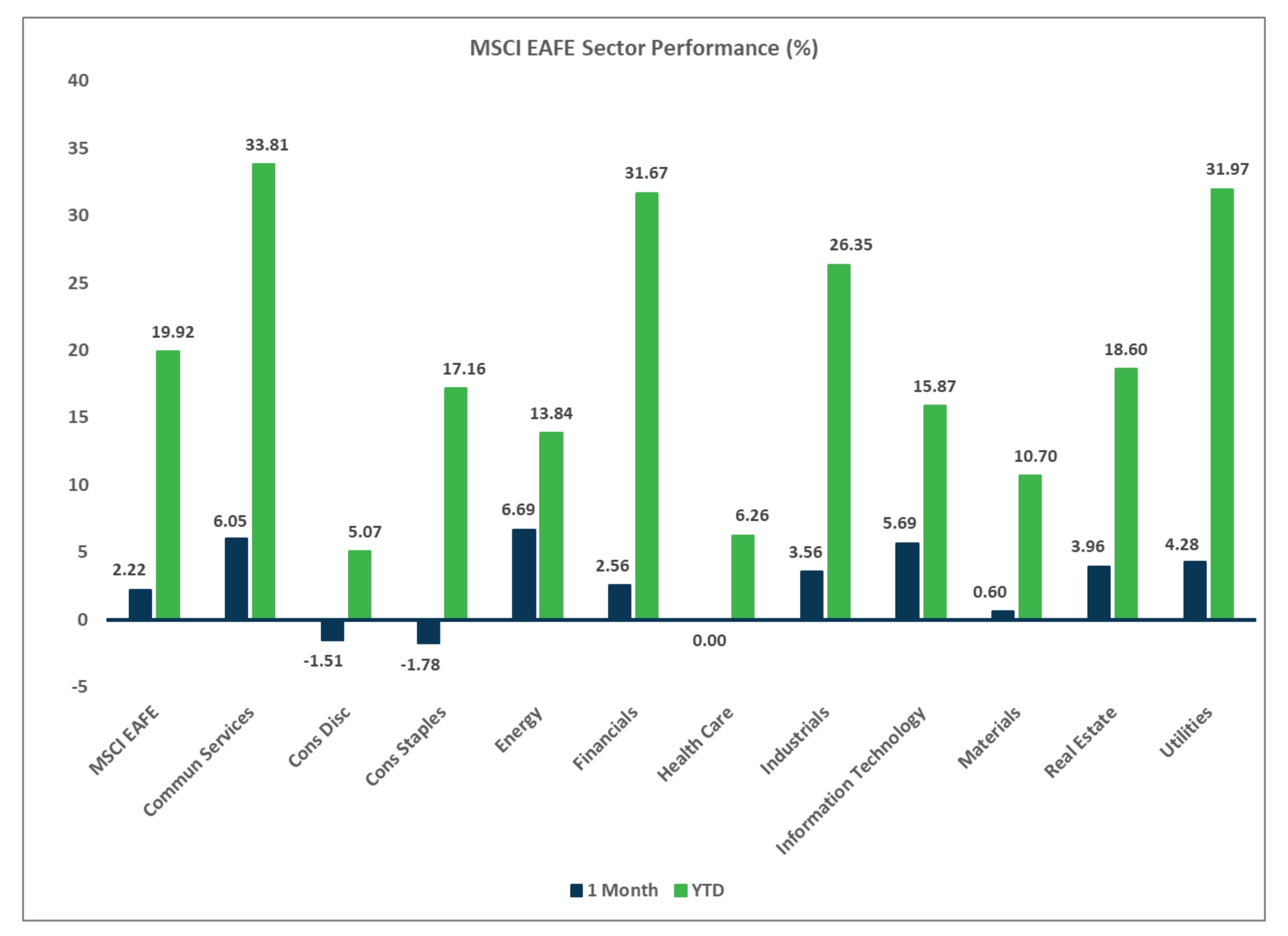

Sector Performance - MSCI EAFE (as of 06/30/25)

Sector Performance - MSCI EAFE (as of 06/30/25)