Market Flash Report | August 2022

Economic Highlights

United States

- Hiring in July was far better than expected, defying multiple other signs that economic recovery has been losing steam. Nonfarm payrolls rose 528,000 for the month and the unemployment rate was 3.5%, easily topping estimates of 258,000 and 3.6%, respectively. The unemployment rate is now back to its pre-pandemic level and tied for the lowest since 1969. Wage growth also surged higher, as average hourly earnings jumped 0.5% for the month and 5.2% from the same time a year ago. The August ADP report showed that private payrolls grew much less than expected. The ADP report is volatile, but could spell trouble for August’s labor market report.

- The U.S. economy contracted for the second straight quarter during Q2, hitting a widely accepted rule of thumb for recession. GDP fell at an annualized rate of 0.6% for Q2, according to the second estimate, below the forecast for a 0.3% gain and a 1.6% decline in the first quarter. The decline in GDP came from a broad swath of factors, including decreases in inventories, residential and nonresidential investment, and government spending at the federal, state and local levels.

- The PCE index came in with a Y/Y rise of 6.3% in July, down from 6.8% in June. The index actually fell 0.1% M/M. The core PCE index, which excludes volatile food and energy prices, showed a 4.6% rise Y/Y and a gain of 0.1% M/M in July, coming in softer than forecasts on both counts. Headline CPI rose 8.5% Y/Y based on the July report with Core CPI increasing 5.9%. While both PCE and CPI inflation came in below expectations, the readings remain well above the Federal Reserve’s 2% target.

- Jerome Powell’s Jackson Hole remarks hammered equity and fixed income markets that were expecting a more dovish tone. Powell reinforced the Fed’s stance that it will do whatever it takes to crush inflation, even if it means causing pain for consumers and the U.S. economy. Interest rates have been on the rise in recent days as market and Fed rate hike expectations have moved more in-line. The Fed has raised rates 225 bps YTD and additional rate hikes are on the way. It needs to see signs of slowing in rent and wage growth before taking its foot off the gas. While the Fed continues to talk tough, we continue to believe future monetary policy action will be data dependent.

Non-U.S. Developed

- August saw a second successive monthly reduction in business activity across the euro area, according to early PMI survey indicators, amid further decline in new orders. Cost of living pressures sapped demand in the service sector, leaving activity only just inside growth territory, while manufacturing remained in a downturn midway through the third quarter of the year. The eurozone composite PMI dropped to 49.2 in August from 49.9 in July. The latest PMI data for the eurozone points to an economy in contraction during the third quarter of the year.

- After growing just 0.1% during Q1, the Japanese economy grew at an annualized rate of 2.2% in Q2. The growth was driven largely by a 1.1% rise in private consumption, which accounts for more than half of Japan’s GDP. Japan still faces uncertainty over rising COVID-19 cases, inflation, supply chain constraints and slowing global growth. Although the economy posted solid growth during Q2, Japan’s COVID-19 recovery has largely lagged other developed countries. Weak consumption has been the primary culprit of the weaker growth. The Bank of Japan has been a global outlier with its ultra accommodative monetary policy which differs from most other countries tightening policy to combat surging inflation.

Emerging Markets

- China's factory activity extended declines in August as new COVID-19 infections, the worst heatwaves in decades and an embattled property sector weighed on production. The official manufacturing PMI rose to 49.4 in August from 49.0 in July. The PMI shows the world's second-largest economy is struggling to emerge from the sluggish growth seen in Q2. The smaller company focused Caixin Manufacturing PMI also slid to 49.5 in August from 50.4 in July. Demand remained bleak, with sub-indexes of new orders and new export orders returning to contraction following two months of expansion.

- China's economy narrowly escaped contraction last quarter due to widespread COVID-19 lockdowns, and economists say its nascent recovery is in danger of fizzling out amid fresh virus flare-ups and a deep crisis in the property sector. The country's cabinet rolled out a package of new economic stimulus measures the last week of August, including billions of dollars worth of policy financing, to lift the faltering economy. The central bank also cut three key lending rates in August in a bid to lower financing costs for companies and individuals. But, as long as the country maintains its strict COVID-19 policies, many analysts expect growth to remain subdued and have been cutting growth forecasts for this year and next.

- India’s economy expanded at the fastest clip in a year, fueled by domestic demand that may moderate in the face of rising borrowing costs and a global slowdown. GDP rose 13.5% Y/Y in Q2, the quickest pace since the 20.1% growth in the same quarter last year. Business investment increased 20.1% Y/Y during Q2 and private consumption surged 25.9%. Similar to most other economies around the world, India is dealing with high inflation and rising rates. India’s central bank has raised rates three times over the past few months and higher borrowing costs are likely to impact GDP growth in future quarters.

- After six months of war with Ukraine, Russia’s economy appears to be outperforming expectations. During the early days of the war, economists expected the Russian economy to contract more than 12% due to punishing sanctions. Forecasts today suggest that the Russian economy will only shrink 4-4.5% in 2022 with inflation topping 13%. GDP is projected to decline 2.7% in 2023.

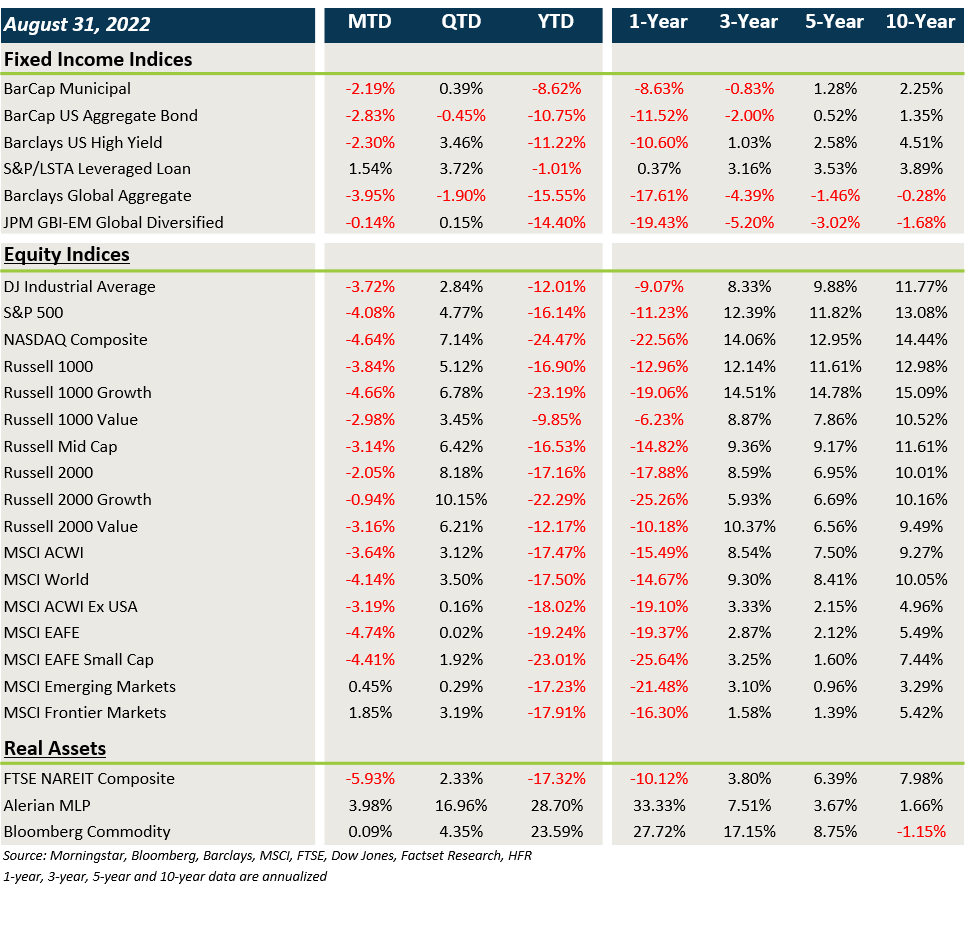

Market Performance (as of 8/31/22)

Fixed Income

- In August, yields surged higher during the second half of the month due to fears of a more hawkish Federal Reserve, fighting sticky inflation. Core fixed income and munis were hit hard.

- IG and HY spreads widened out last month while floating rate loans provided a buffer against higher rates.

- Non-U.S. fixed income was hurt by rising rates and the stronger USD. EMD provided some relative outperformance.

U.S. Equities

- After starting out positive, U.S. equities fell during the second half of August.

- Large caps lagged small caps.

- Large cap growth trailed large cap value, but small cap growth outpaced small cap value.

Non-U.S. Equities

- Non-U.S. equities trailed their U.S. counterparts last month, led by particular weakness in Europe.

- Large caps in EAFE markets beat small caps and EM small caps handily outperformed EM large caps.

- EMs provided strong relative outperformance in August led by a rebound in China and Latin America.

Sector Performance

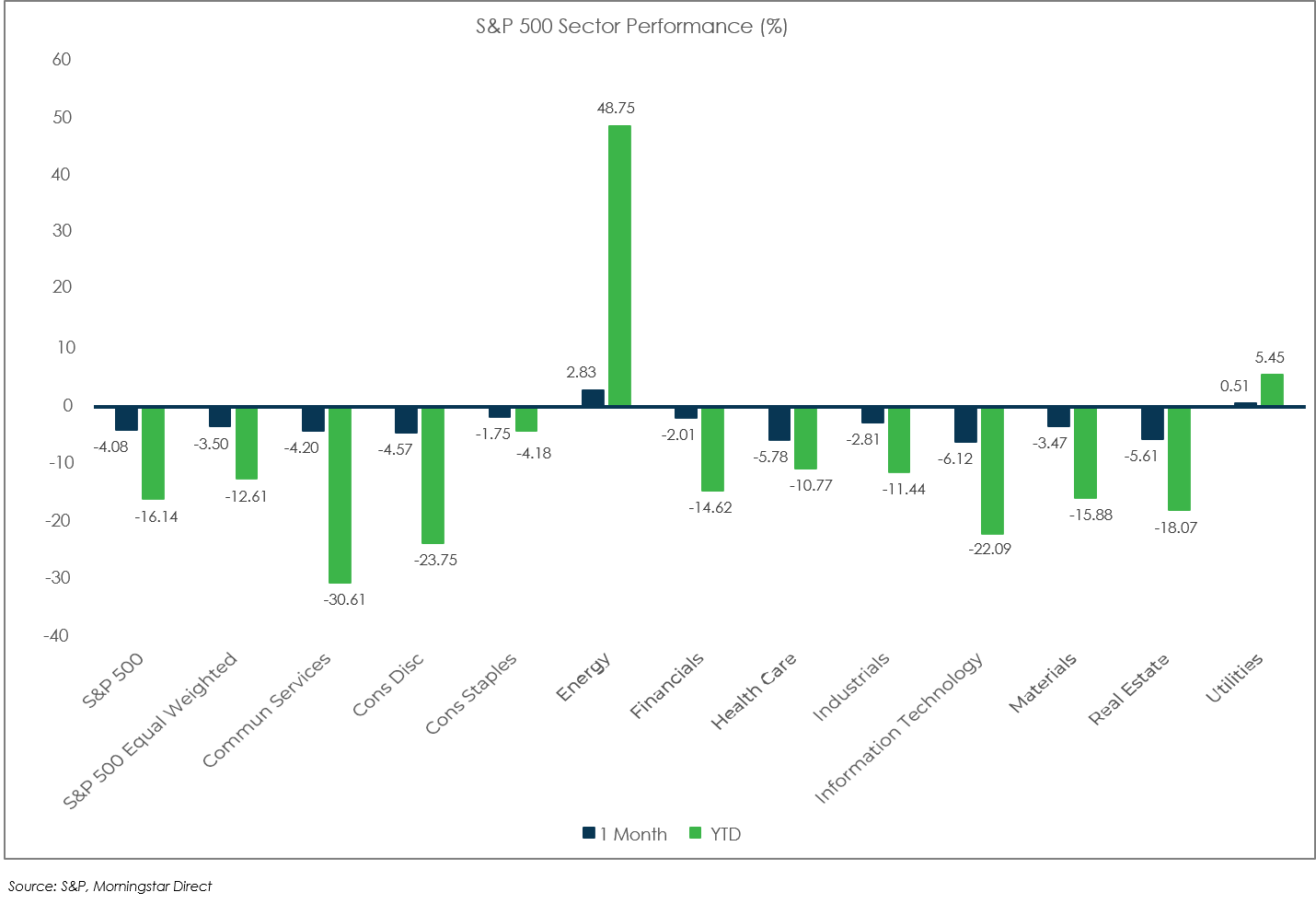

S&P 500 (as of August 31, 2022)

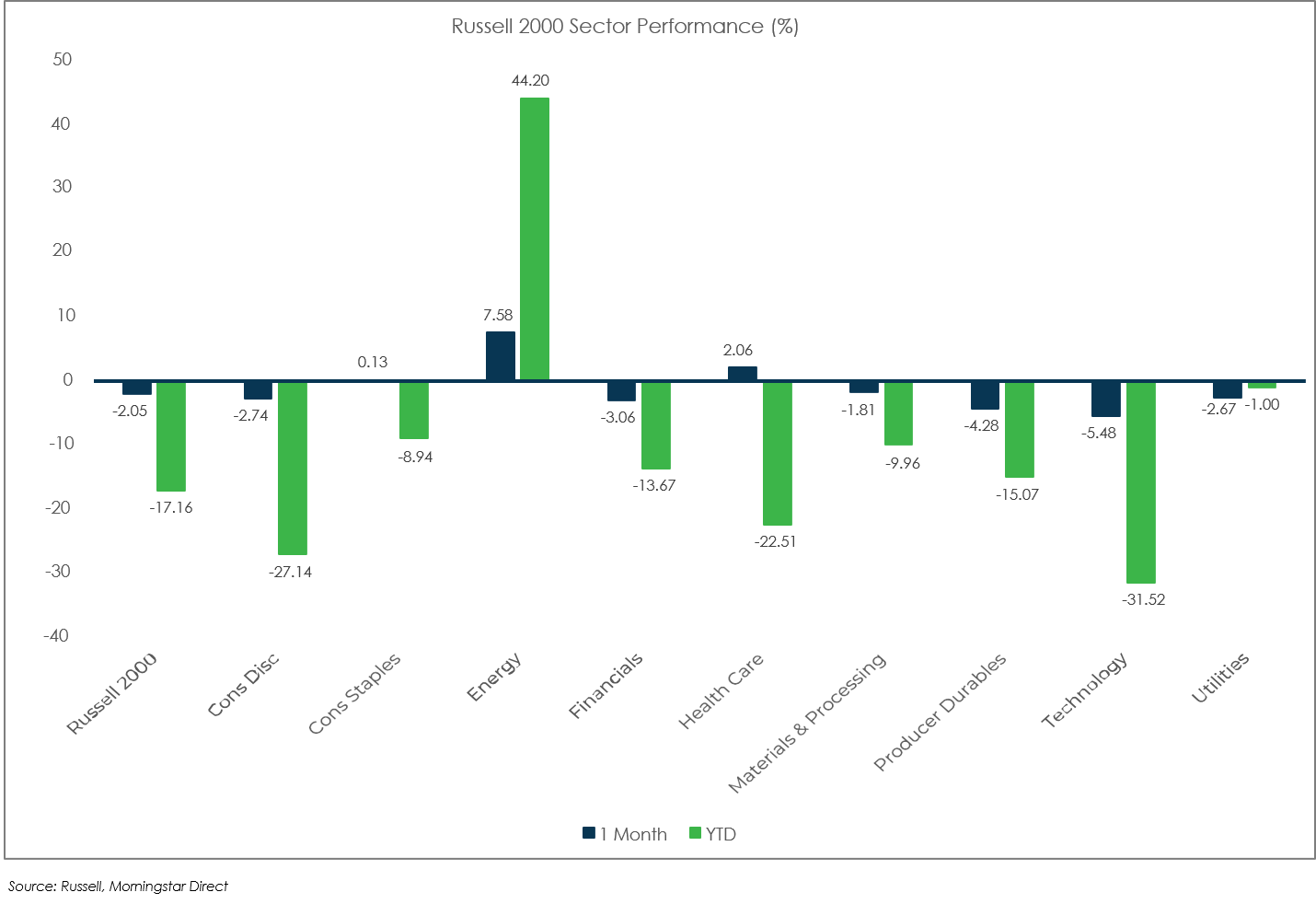

Russell 2000 (as of August 31, 2022)

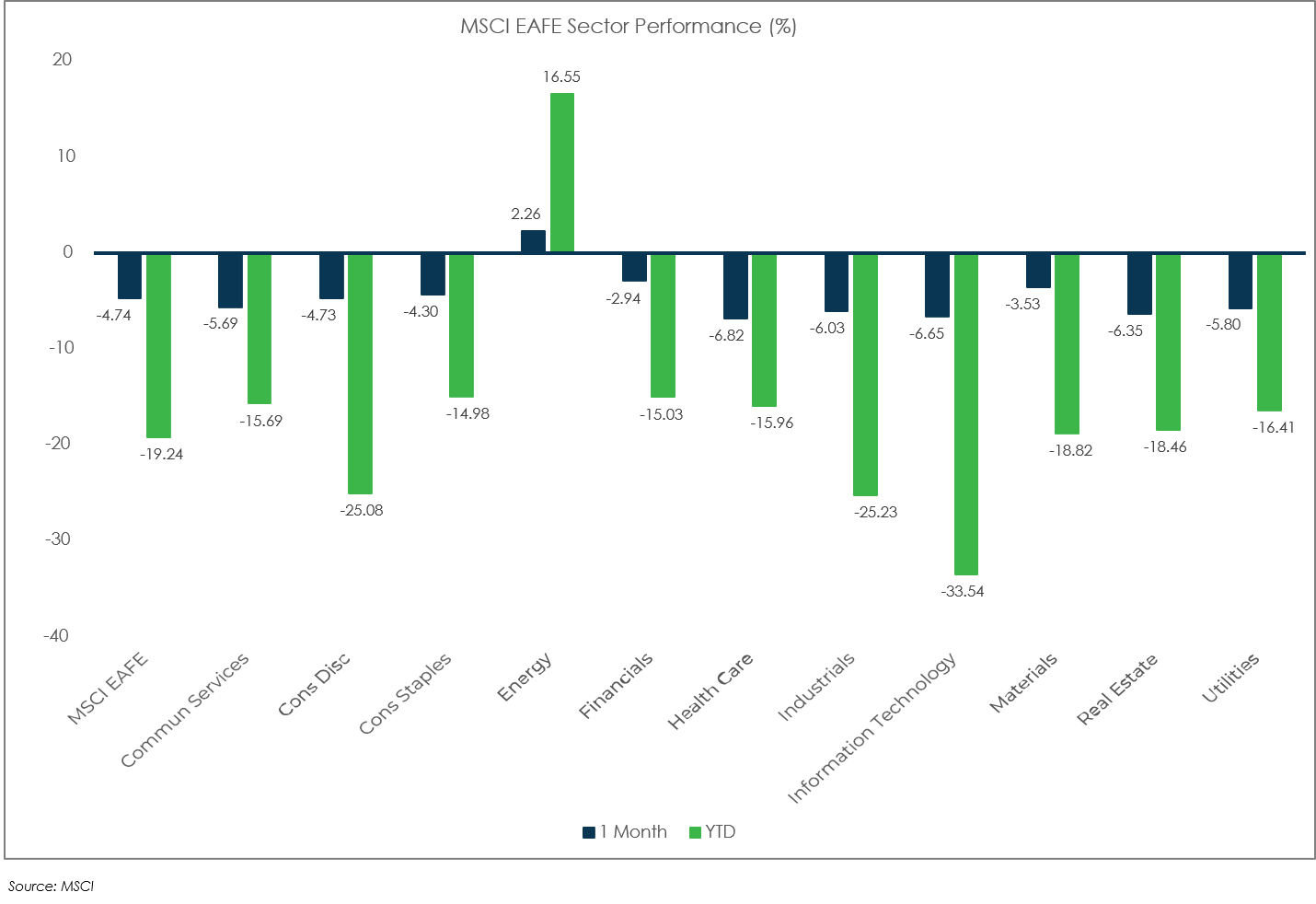

MSCI EAFE (as of August 31, 2022)

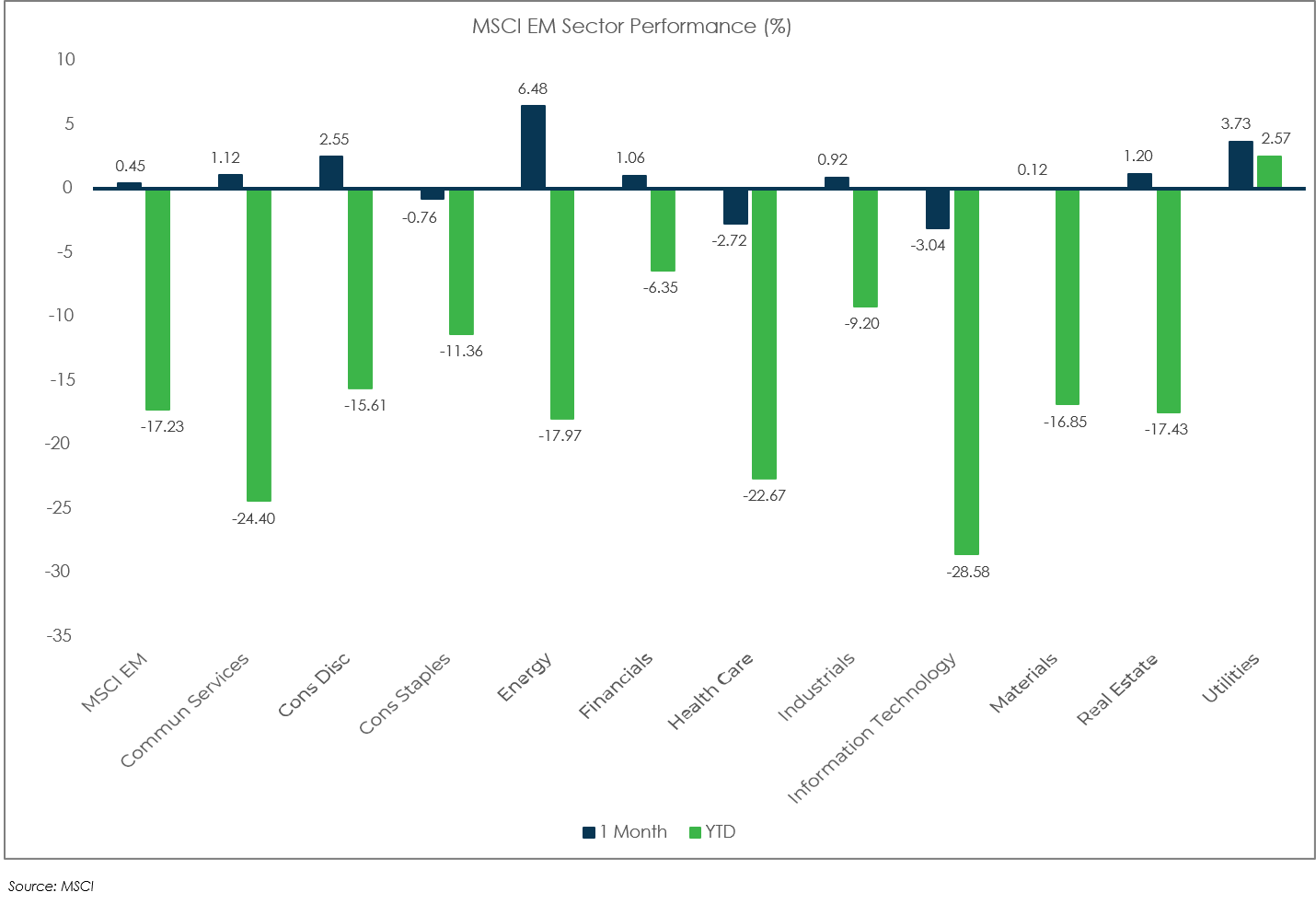

MSCI EM (as of August 31, 2022)