Market Flash Report | December 2022

Economic Highlights

United States

- The November employment report was red hot with job growth and wage growth exceeding expectations. Employers added 263,000 new jobs to the U.S. economy, well ahead of the 200,000 estimate. The unemployment rate held steady at 3.7% and the broader U6 unemployment rate fell slightly to 6.7%. The real problem was the surge in wages, which rose 0.6% M/M or 5.1% Y/Y. Both figures were well ahead of estimates. The “hotter” than expected jobs report will potentially bring more hawkish Federal Reserve policy back into play after markets began pricing in an end to the current policy tightening cycle. After raising rates by another 50 bps at its December meeting, the Fed now expects the terminal rate to be around 5.1%.

- Headline CPI came in below expectations with a gain of 0.1% M/M and 7.1% Y/Y. Core CPI rose 0.2% M/M and 6% Y/Y, also below expectations. Inflation is clearly starting to cool, but there is still concern over rising shelter costs and high/sticky wage growth. Markets initially rallied on the news, but reversed course as investors grew more cautious over the increase in services inflation. Goods inflation has fallen over the past few months, but services inflation continues to remain high including shelter costs that, significantly, are reported with a lag.

- Retail sales surged by 1.3% in October as consumers continue to spend despite inflation. Consumer spending increased on items such as gas, groceries, furniture and cars, but shoppers pulled back on spending at electronics and appliance stores, sporting goods retailers and department stores. Consumer spending has remained resilient despite 40-year high inflation, but at some point, the $1.5T in aggregate excess savings will either run out or consumers will tighten their belts.

- Durable goods orders in the U.S. jumped 1% M/M in October, following a downwardly revised 0.3% increase in September. Excluding the volatile transportation sector, durable goods orders rose 0.5% and the core component that relates to GDP business spending increased 0.7%. The Atlanta Fed’ GDPNow model is forecasting 3.4% growth in Q4 while the consensus amongst economists sits in the 2-2.5% range.

Non-U.S. Developed

- The eurozone downturn extended into its sixth successive month in December, according to flash PMI data. The rate of decline of business activity moderated for a second month running amid a reduced rate of loss of orders, improving supply conditions, lower price pressures and an uplift in business confidence. While any recession may be mild, the further fall in business activity in December signals the strong possibility of a downturn. Q4 data is tracking at a quarterly rate consistent with GDP of 0-0.2%.

- Bank of Japan Gov. Haruhiko Kuroda shocked markets in late December by doubling a cap on 10-year JGB yields. The BOJ will now allow Japan’s 10-year bond yields to rise to around 0.5%, up from the previous limit of 0.25%. The central bank kept its 10- year yield target unchanged at around 0% and left its short-term interest rate at -0.1%. It also said it would significantly increase its bond purchases to ¥9 trillion ($67.5 billion) per month compared with the currently planned ¥7.3 trillion. Many economists interpreted the move as laying the preliminary groundwork for exiting a decade of extraordinary stimulus policy. The surprise decision sent bond yields surging higher and the yen strengthened significantly versus other major currencies.

Emerging Markets

- China’s economy showed further signs of slowing in December. The official manufacturing PMI declined from 48 in November to 47 in December. The drop was the biggest since the early days of the COVID-19 pandemic in February 2020. China recently reopened its economy and while that is positive for the economic backdrop, COVID-19 infections have surged across the country. Although the worst may be in the rearview mirror for the Chinese economy, manufacturing may continue to face headwinds with the rest of the world slowing. Workers may be back in the factories, but new orders are slowing due to weakness in other developed and emerging nations.

- Similar to the manufacturing sector, the official service sector PMI fell sharply from 46.7 in November to 41.6 in December. Not surprisingly with COVID-19 surging across the country, demand for products and services slowed sharply last month. It is important to note that the smaller-company focused Caixin PMIs also demonstrated weakness in both manufacturing and services.

- India’s economy is posting the fastest growth among major economies, putting it on track to become the world’s third largest before the end of the decade, according to financial forecasts from Morgan Stanley, IMF and S&P. India is expected to grow by nearly 7% in 2022 despite the economic turbulence created by Russia’s war in Ukraine. That momentum is likely to continue, helping it overtake Japan and Germany to become the world’s third-largest economy by 2028. India benefits from having a relatively shielded economy that tends to weather external turbulence better than others along with the need to maintain a high level of growth to raise 1.4 billion people out of poverty.

Market Performance (as of 12/31/22)

Fixed Income

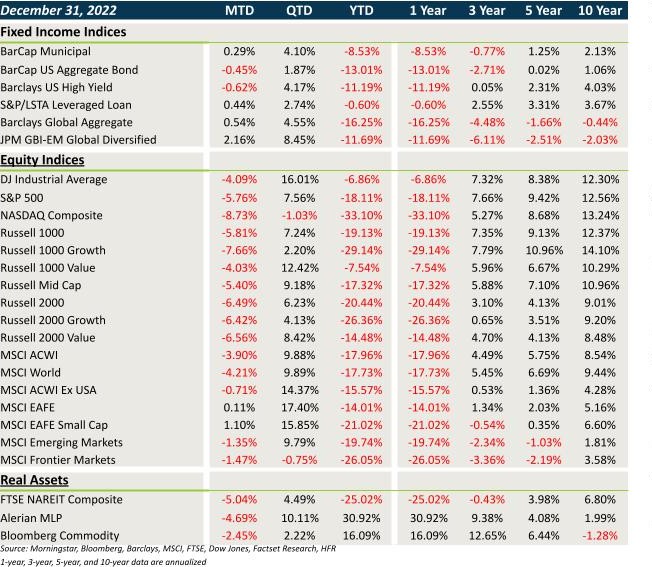

- Yields across the globe moved higher to end 2022. This led to losses in traditional core fixed income.

- Munis bucked the trend due to favorable technicals coming back into the market.

- HY lagged while other credit/spread sectors eked out small gains.

- USD weakness provided another significant boost for non-U.S. assets.

U.S. Equities

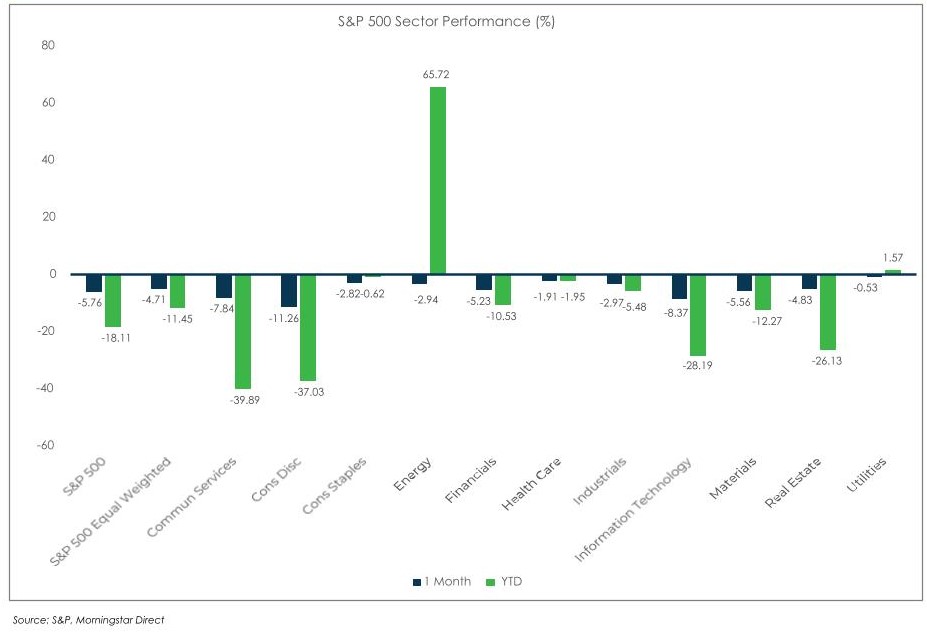

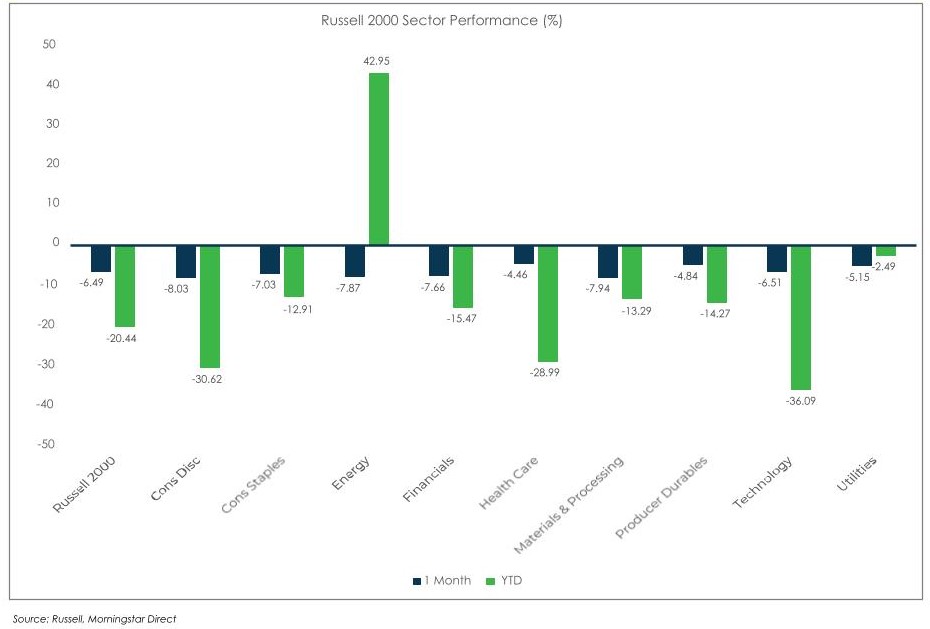

- U.S. equities exhibited weakness to end the year, led down by tech/growth stocks and small caps.

- Large caps beat small caps and value led growth within large caps. There was little dispersion between SCV and SCG last month.

- The S&P 500 ended 2022 down 18.1%.

Non-U.S. Equities

- Non-U.S. equities provided relative outperformance versus U.S. equities in December. The EAFE Index gained 0.1%.

- Value beat growth across developed market equities.

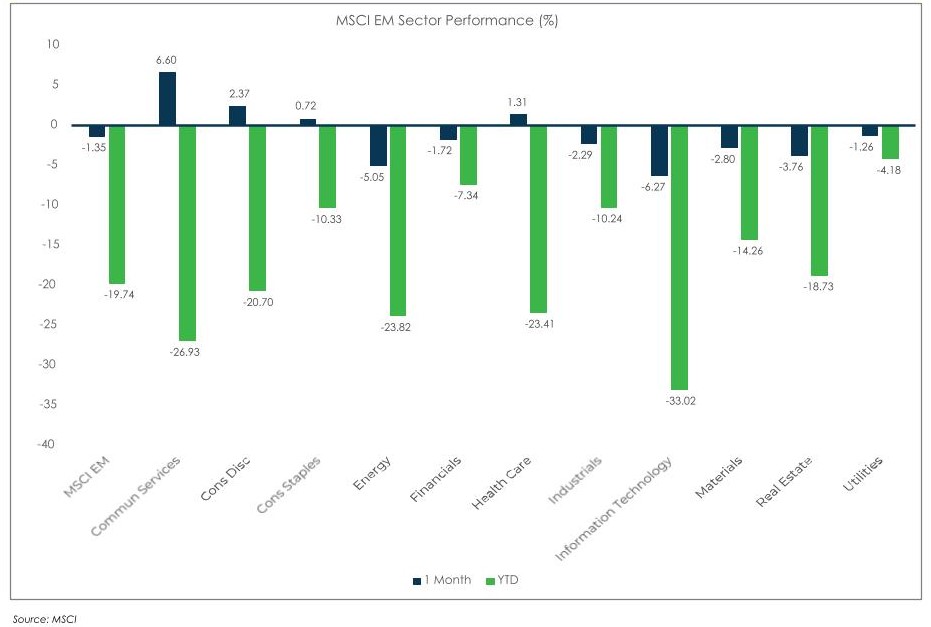

- EMs fell slightly last month, with broad weakness in Asia and LatAm being offset by the strong rebound in China.

- The weaker USD boosted EAFE returns by 310 bps and EM returns by 60 bps.

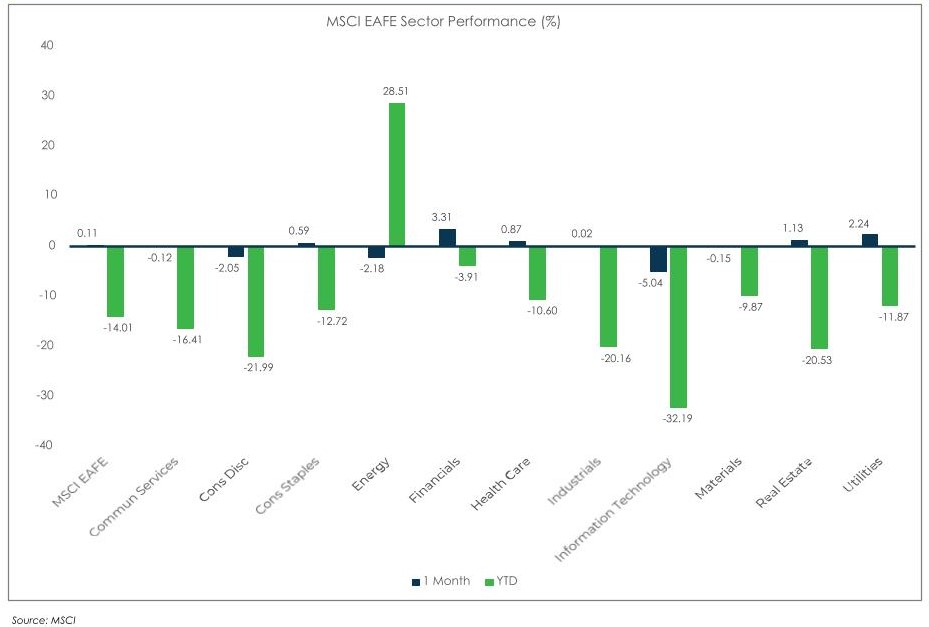

Sector Performance

S&P 500 (as of November 30, 2022)

Russell 2000 (as of November 30, 2022)

MSCI EAFE (as of November 30, 2022)

MSCI EM (as of November 30, 2022)