Market Flash Report | December 2023

Economic Highlights

United States

- U.S. employers added 199,000 new jobs to the economy in November, slightly ahead of the 190,000 estimate. The unemployment rate declined to 3.7% and the broader U6 unemployment rate fell from 7.2% to 7%. Average hourly earnings, a key inflation indicator, increased by 0.4% M/M and 4% Y/Y. While job gains were solid last month, sizable numbers came from government hiring and workers returning to work from recent strikes. Experts expect hiring to slow in 2024 with economic growth. Q3 GDP growth was strong, but the Atlanta Federal Reserve currently pins Q4 growth at just 1.2%. Consumer spending will be the key driver to monitor, as it grew 3.6% in Q3 and accounts for nearly 70% of the U.S. economy.

- Inflation slowed to a 3.1% annualized rate in November, down slightly from the prior month. Core CPI remained flat at 4% for the second straight month. Energy prices fell 2.3%, food prices rose 0.2%, used car prices increased 1.6%, and the all-important shelter component rose 0.4%. While inflation has not yet hit the Fed’s target level, it continues to trend lower and is below the rate of wage growth. Futures markets believe the Fed is finished raising rates and actually expect 5 rate cuts in 2024.

- Manufacturing activity in the U.S. contracted at a slightly slower pace in December based on the latest Institute of Supply Management (ISM) Manufacturing Purchasing Managers’ Index (PMI) reading. The headline figure of 47.4 was up from 46.7 in November and led by strength in production, which rebounded back above 50. Employment also improved, but new orders and prices both weakened. Survey responses were mixed depending on the business and industry. Overall, it appears as if optimism remains in place, fueled by lower inflation and interest rates.

- U.S. existing home sales expanded by 0.8% M/M in November, while new home sales declined 12.2%. Despite optimism for future homebuying as mortgage rates decline, elevated rates may continue to affect home buyers in the near term.

Non-U.S. Developed

- Manufacturing in the eurozone remained in contraction in December 2023 with PMIs reflecting steep declines in output and employment, but an easing of the decreases in demand and purchasing. Some of the manufacturing sector sub-indices suggested that the worst of the industry’s slump had passed, with contraction in new orders and purchasing activity slowing. The Hamburg Commercial Bank (HCOB) Eurozone Manufacturing PMI rose slightly to 44.4 from 44.2 in November to reach a 7-month high.

- Inflation in the eurozone fell from 2.9% in October to 2.4% in November, the lowest reading since July 2021. Annual core inflation, which excludes prices for energy, food, alcohol and tobacco, was confirmed at 3.6%, the lowest reading since April 2022. Inflation is likely to pick up on account of an upward base effect for the cost of energy.

- In the U.K., the economy contracted 0.1% Q/Q in Q3, but headline inflation fell faster than anticipated at an annualized rate of 3.9%.

- With Japan’s larger-than-expected contraction in Q3 economic growth, inflation also declined to its lowest level since July 2022. Headline inflation fell from 3.3% in October to 2.8% in November. Core inflation declined to a 16-month low of 2.5%.

Emerging Markets

- While China’s official manufacturing PMI softened in December from 49.4 to 49.0, the smaller-company focused Caixin Manufacturing PMI strengthened from 50.7 to 50.8. Both readings are fairly weak and signal that more monetary policy support may be necessary to revive the Chinese economy.

- China’s service sector sits in better shape based on the latest PMI readings. The smaller-company focused Caixin Services PMI rose from 50.4 in October to 51.5 in November. The official Non-Manufacturing PMI for China edged up to 50.4 in December 2023 from November's 11-month low of 50.2.

- With inflation under control in China and perhaps deflation taking hold, Chinese policymakers are uniquely positioned to provide additional stimulus measures to support the sluggish economy. Growth has slowed in recent years as the country grapples with its failed COVID-19 reopening and weak external demand.

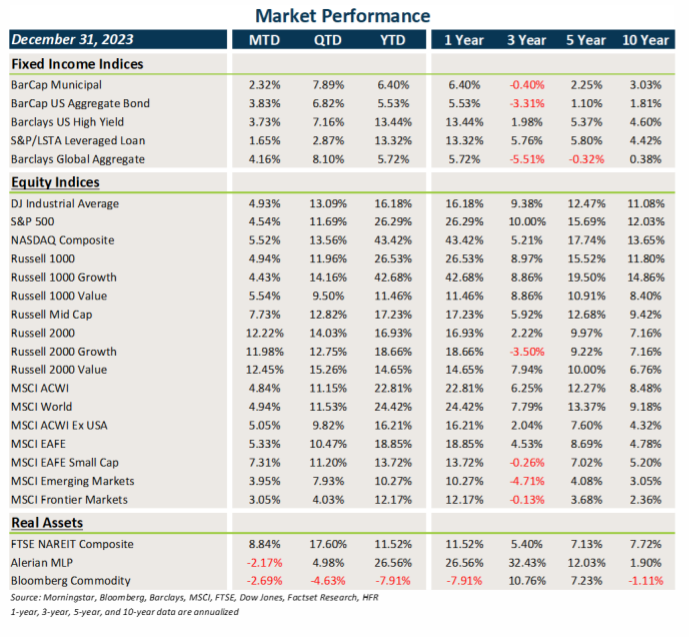

Market Performance (as of 12/31/23)

Fixed Income

- Treasury and other sovereign debt yields continued their trek lower in December, leading to another month of strong gains in fixed income.

- Core fixed income and municipal bonds posted very outsized gains last month.

- Credit performed well in December, but shockingly lagged the BarCap Agg Index.

- USD weakness boosted non-U.S. returns.

U.S. Equities

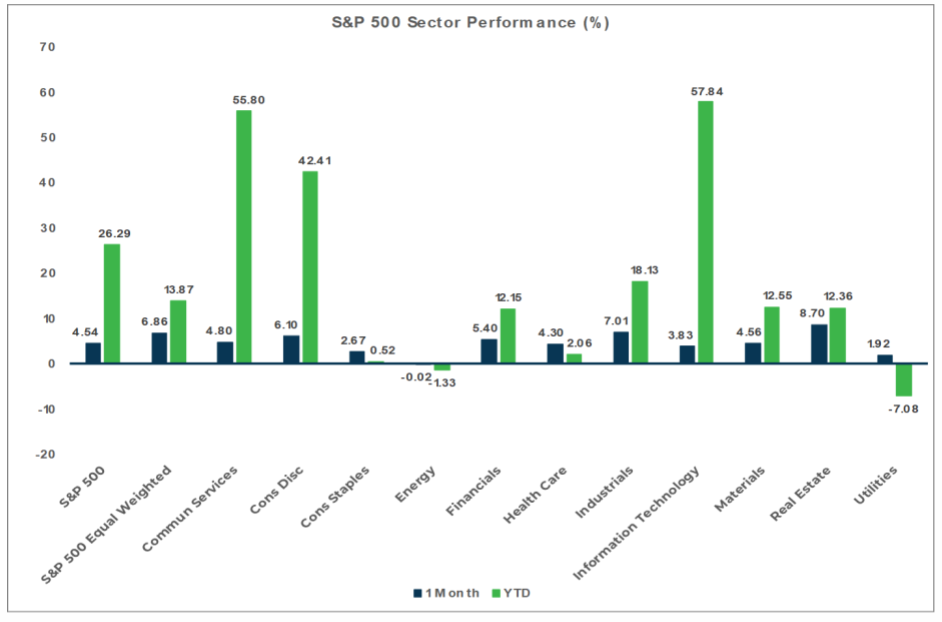

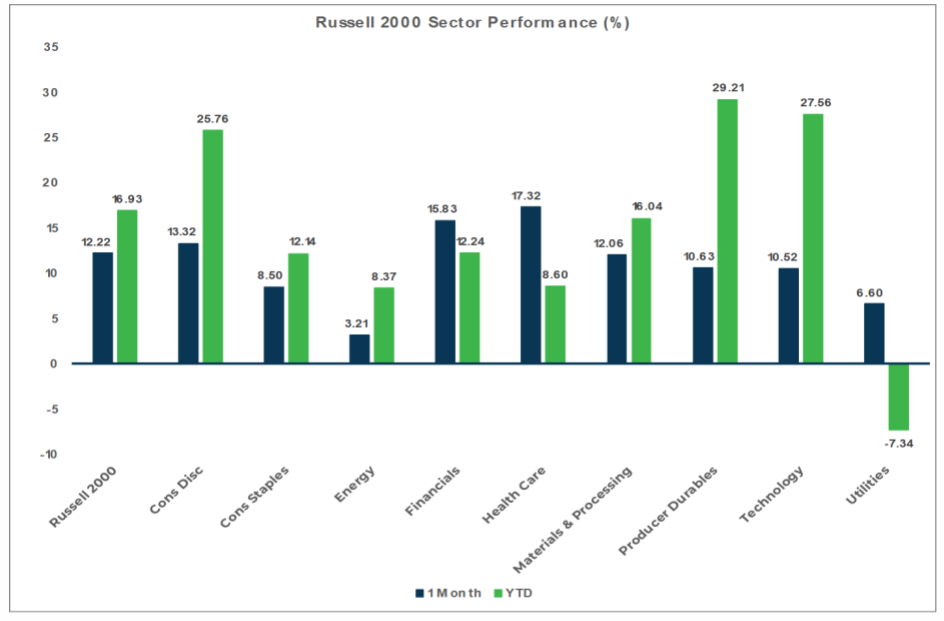

- U.S. equities posted solid gains in December, led by small cap and value stocks.

- The broad market rally in December was fueled by the surge in small cap stocks that finally outperformed large caps.

- Value beat growth across the entire market cap spectrum last month.

Non-U.S. Equities

- Non-U.S. equities saw a boost from lower interest rates across the globe and the weaker USD.

- Similar to what occurred in the U.S., small caps outperformed large caps.

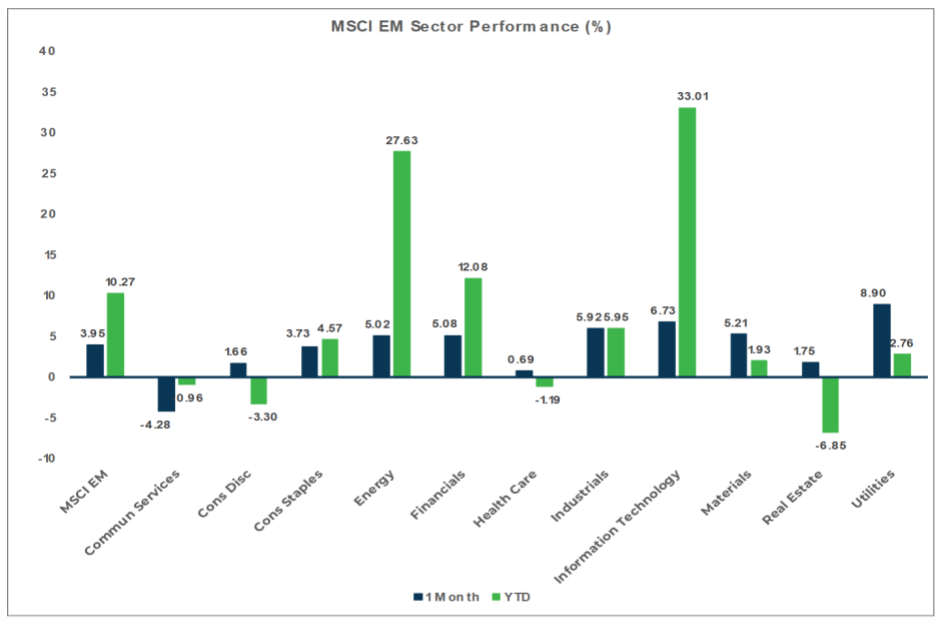

- Growth beat value outside the U.S. in December and emerging markets (EM) lagged developed markets.

- Weakness in China continued to weigh on EM equities last month.

Sector Performance - S&P 500 (as of 12/31/23)

Sector Performance - Russell 2000 (as of 12/31/23)

Sector Performance - MSCI EAFE (as of 12/31/23)

Sector Performance - MSCI EM (as of 12/31/23)