Market Flash Report | February 2022

Economic Highlights

United States

- The U.S. economy grew at a slightly faster 7% annual pace in the fourth quarter, updated figures show, as Americans boosted spending and businesses rebuilt their stockpile of goods after inventories had fallen to very low levels. Consumer spending rose 3.1% Y/Y and inventory restocking was revised slightly lower. The most notable change in Q4 GDP was a somewhat larger increase in business investment, especially housing. Residential spending rose 1% instead of declining 0.8% as initially reported. The increase in outlays on equipment was also raised to 3.1% from 2%. Government spending fell and the rate of inflation also rose at the fastest pace since 1982. Current estimates show GDP rising less than 2% in Q1 2022.

- U.S. labor markets sent mixed signals for January with private payrolls badly missing expectations in the ADP report while the Nonfarm payroll report surpassed expectations. The January ADP Employment Report missed consensus expectations for an increase and instead showed 301,000 jobs cut in private payrolls. Nonfarm payrolls grew sharply by 467,000, drastically outpacing the consensus estimate of 125,000. The labor force participation rate also inched up 0.3% to 62.2%, the highest print since the start of the pandemic. Additionally, January’s average hourly wages increased 5.7% Y/Y and the unemployment rate ticked back up to 4%.

- The manufacturing sector in the U.S. softened a bit last month with the ISM Manufacturing Index falling to 57.6 from 58.8 in December. New orders weakened modestly while production and employment strengthened. The ISM Services PMI fell from

- 62.3. in December to 59.9 in January. Business activity and employment were weak components of the report.

- Inflation hit a more than 40-year high in January based on the CPI/PCE gauges, but fiscal policy became more uncertain with hostilities breaking out between Russia and the Ukraine. Prior to the Russian invasion, seven rate hikes were expected, but the number has fallen to just four as of 3/1/2022. There is also currently no chance of a 50 bps move at the upcoming March meeting.

Non-U.S. Developed

- The eurozone composite PMI increased from 52.3 in January to 55.8 in February. Eurozone business activity growth accelerated sharply in February as COVID-19 containment measures were relaxed. Future expectations, new orders and jobs growth also improved. Growth picked up especially in the service sector, though manufacturers also reported improved production gains as a result of rising demand and fewer supply bottlenecks. Based on this report, it appears that the eurozone regained some lost economic momentum early in 2022.

- The world's third-largest economy, Japan, expanded at an annualized rate of 5.4% in Q4 after contracting a revised 2.7% in the previous quarter. The Q4 GDP came in below economists’ expectations for a 5.8% gain. Private consumption increased 2.7% Q/Q and capital expenditures rose 0.4%. The Japanese government expects economic growth to stall or perhaps contract in Q1 due to rising omicron variant cases which will hurt service consumption.

- Japan's recovery continues to lag other advanced economies, forcing the Bank Of Japan to keep monetary policy ultra-loose, even as other central banks eye interest rate hikes.

Emerging Markets

- China’s official services PMI hit 51.6 in February, up from 51.1 in the prior month. China's official manufacturing PMI increased slightly to 50.2 in February from 50.1 in January, largely driven by a jump in new orders. The production and employment sub-indices also continued to expand, albeit at a slower pace.

- The smaller company-focused Caixin China Manufacturing PMI unexpectedly rose to 50.4 in February 2022 from 49.1 in the previous month (which was the lowest reading in 23 months). The improvement came as output expanded for the third time in the past four months, new orders grew the most since last June and buying activity continued to increase. In the meantime, employment dropped for the seventh straight month with the rate of decline easing; while backlogs of work increased amid shortages of employees and rising demand.

- All eyes are on the Russian economy which is the 11th largest in the world at $1.5 trillion. Russia’s central bank has also amassed a war chest of $630 billion in reserves including foreign currencies and gold, a huge sum compared to most other countries. The U.S., Europe and other key partners have levied significant economic sanctions on Russia in response to its invasion of the Ukraine. According to Capital Economics, the sanctions have rendered roughly 50% of Russia’s foreign reserve stockpile useless. In an attempt to shore up the collapsing ruble, the Russian central bank hiked interest rates to 20% to support financial and price stability.

- Russia is also imposing capital controls. The central bank ordered companies to sell foreign currencies on Monday to prop up the ruble as it plunged to a record low against the U.S. dollar. Putin is planning a decree that would temporarily ban foreign companies and investors from selling Russian assets which have become toxic since the invasion. Sanctions have rendered much of Putin’s reserves as useless in the fight to defend the country’s collapsing currency.

- One major problem is that Russian banks only have enough foreign cash on hand to cover roughly 15% of the foreign currency deposits on their books. The central bank would normally supply banks with foreign currency, but with half its war chest out of bounds it may not be able to do that and defend the ruble at the same time. This could lead to significant pressure on the Russian central bank. Assuming the U.S. and Europe don’t crack down further on Russia, the country benefits from oil/gas exports which far exceed imports. These payments into the country are a major source of foreign currency. If investors and businesses try to move large amounts of foreign cash outside the country as the ruble falls, the Russian central bank could be forced to spend a large amount of its reserves.

- As of now, Russian equities and the ruble have collapsed while interest rates have surged higher. Equity markets also had more than $150 billion wiped out in the first week of March. It is important to note that ruble-denominated Bitcoin transactions have also jumped, perhaps explaining the sudden rise in digital assets.

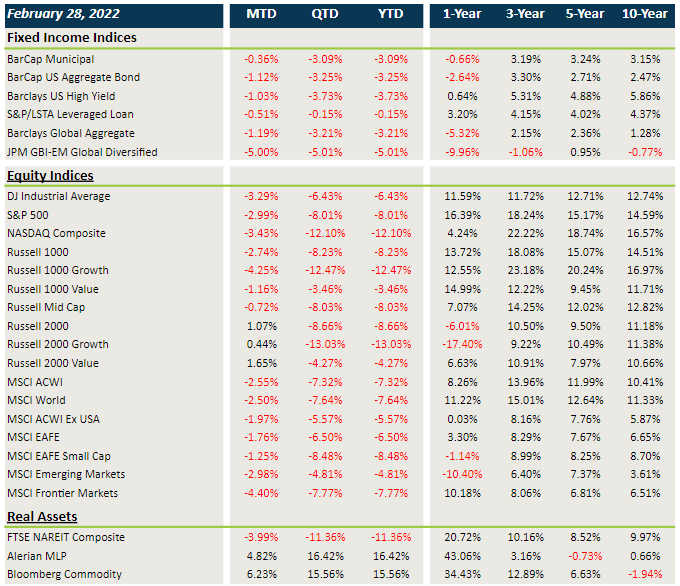

Market Performance (as of 2/28/22)

Fixed Income

- Treasury and sovereign bond yields across the globe continued to move higher in February leading to losses in core fixed income and munis.

- Credit spreads widened last month across the board.

- Floating rate loans were not spared as they experienced negative returns and wider spreads.

U.S. Equities

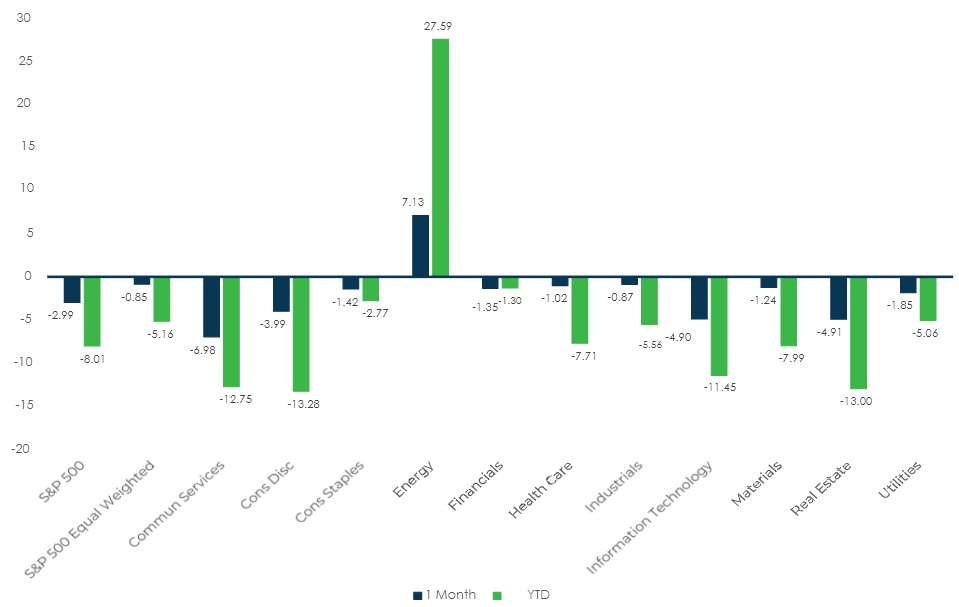

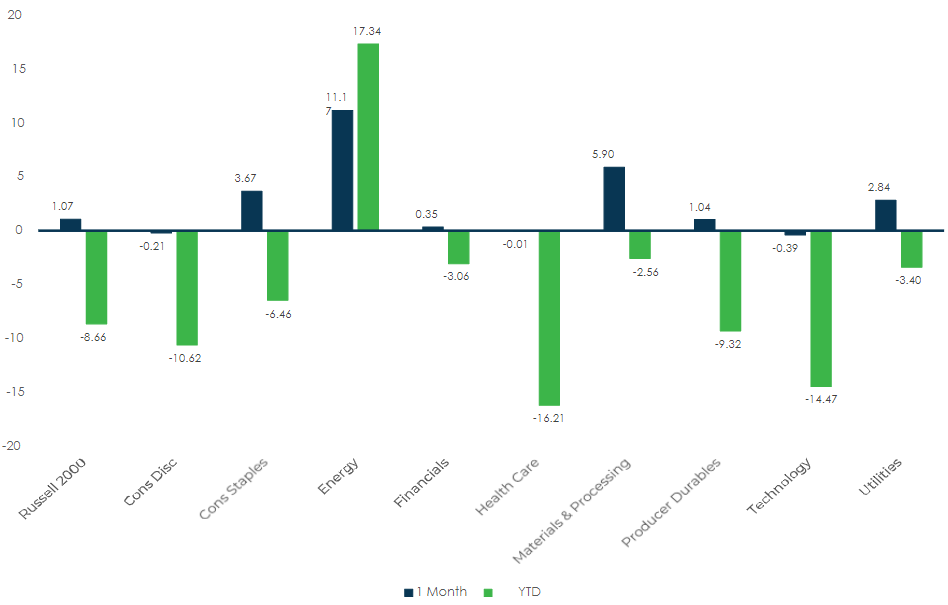

- U.S. equities were mixed versus non-U.S. equities in February.

- Large cap stocks lagged small caps for the first time in a while.

- Value continued to outperform growth with energy being the best performing sector.

Non-U.S. Equities

- Non-U.S. equities generally outperformed the U.S. last month excluding small caps.

- Similar to the U.S., value beat growth and small caps outperformed large caps.

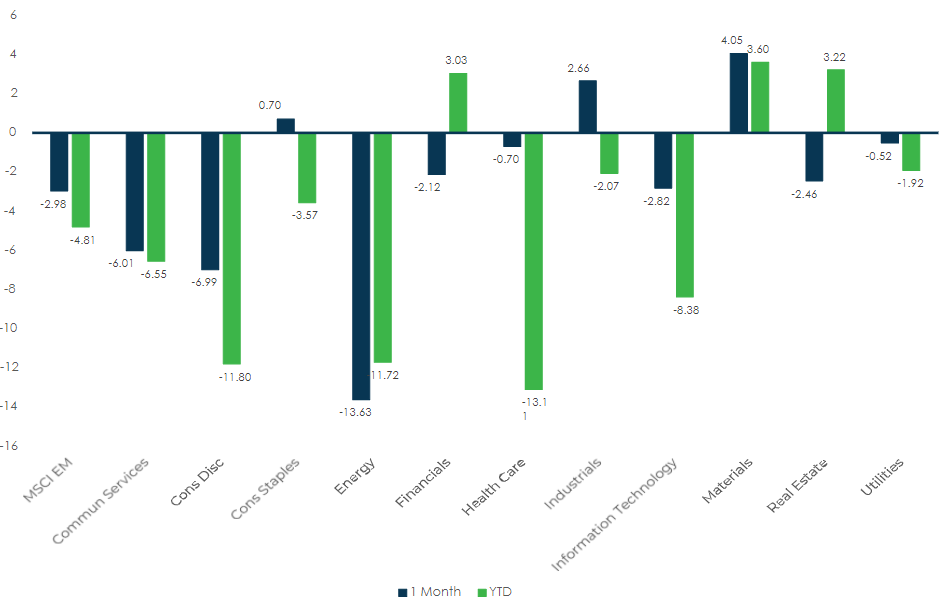

- EMs fell 3% in February, led by extreme weakness in Russia and Eastern Europe.

- Strength of the U.S. dollar hurt EAFE and EM returns last month.

Sector Performance – S&P 500 (as of 2/28/22)

Sector Performance – Russell 2000 (as of 2/28/22)

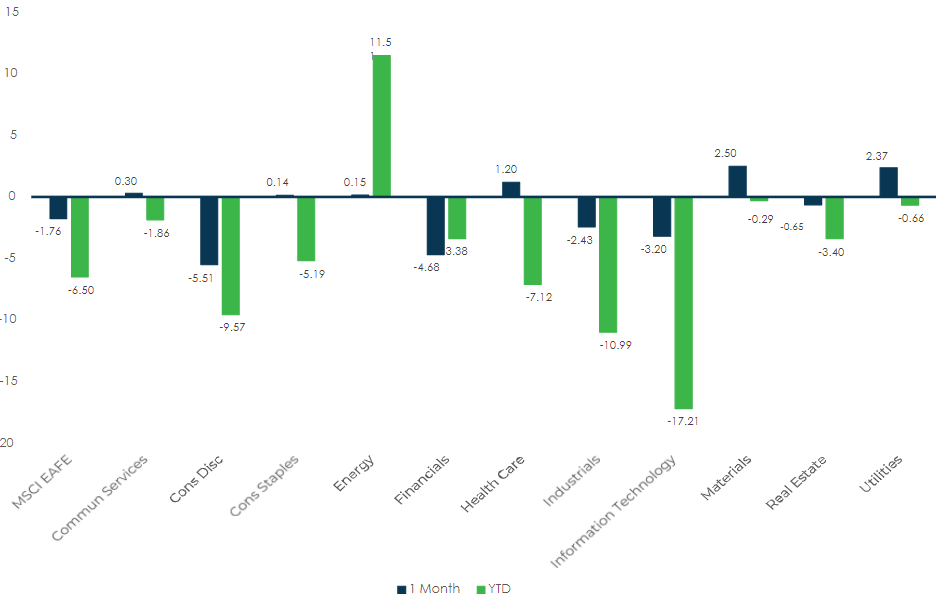

Sector Performance – MSCI EAFE (as of 2/28/22)

Sector Performance – MSCI EM (as of 2/28/22)