Market Flash Report | January 2023

Economic Highlights

United States

- Payroll growth decelerated in December but was still better than expected with 223,000 new jobs being added to the economy versus the estimate for 200,000. The unemployment rate fell from 3.7% to 3.5%, and the broader U6 unemployment rate fell to its lowest reading ever at 6.5%. Wage growth was less than expected: an indication that inflation pressures could be weakening. Average hourly earnings rose 0.3% M/M or 4.6% Y/Y. The respective estimates were for growth of 0.4% and 5%.

- All eyes were on the December CPI report, which showed headline inflation fell 0.1% M/M (largest M/M decline since April 2020) while core inflation rose 0.3%. On an annual basis, headline CPI rose 6.5% and core increased 5.7%. Gas prices, which fell 9.4% M/M or 1.5% Y/Y, were the major driver of the decline. PCE inflation rose 5% Y/Y in December and core PCE increased 4.4% (lowest since December 2021). On a M/M basis in December, prices for goods decreased 0.7% and prices for services increased 0.5%.

- U.S. retail sales declined by –1.1% in December after consumer fears of high inflation and a slowing economy made for a lackluster holiday shopping season. While December sales fell more than consensus expectations, November sales were also revised lower from –0.6% to –1.0% M/M. Retail sales during the holidays came in lighter than expected but still grew 6% Y/Y.

- Durable goods orders jumped 5.6% in December, well ahead of the 2.4% expectation. However, orders fell 0.1% when excluding transportation as demand for Boeing passenger planes helped drive the headline number. The surge in transportation orders masked underlying weakness in business spending.

- The Federal Reserve raised rates by another 25 bps at its February 1 meeting, but all projections, including the terminal rate, were unchanged from December. There continues to be a big disconnect between market and Fed terminal rate expectations, and risk assets have rallied sharply over the past month in anticipation of the Fed being near the finish line with its current rate hiking cycle. Chairman Powell indicated that disinflationary pressures are starting to take hold. A soft landing scenario seems increasingly likely.

Non-U.S. Developed

- The start of 2023 saw eurozone business activity rise marginally, according to flash PMI data from S&P Global, showing a tentative return to growth after six successive months of decline. The composite PMI hit a 7-month high at 50.2 while the services PMI hit a 6-month high at 50.7. Manufacturing also hit a 5-month high, but remains in contraction territory at 48.8. A steadying of the eurozone economy at the start of the year adds to evidence that the region might escape a deep recession. The eurozone posted surprise GDP growth of 0.1% Q/Q in Q4, ahead of the -0.1% estimate. GDP grew 1.9% Y/Y, but is expected to slow sharply in 2023.

- Japan’s government cut its monthly economic assessment in January for the first time in 11 months, as trade weakened due to a global economic slowdown. The Cabinet Office said in its latest report Wednesday, February 1 that parts of the economy are showing weakness, while overall it’s picking up moderately. It downgraded its view of exports, imports and bankruptcies. The government also remained cautious over downside risks from the global economic slowdown amid monetary tightening, inflation and financial market fluctuations. One highlight was the robust level of domestic demand/private consumption.

Emerging Markets

- China’s Q4 GDP report was better than expected with 2.9% growth reported versus the estimate of 1.8%. For 2022, the Chinese economy grew 3%, slightly ahead of the 2.8% forecast. While beating downwardly revised expectations, GDP was well below the government’s 5.5% growth target. Economic data showed broad weakness in 2022, but readings such as retail sales, industrial production and fixed asset investment were above forecasts in December. Growth has clearly slowed across China due to their zero-COVID policy, but restrictions have been removed and the PBOC has provided a lot of stimulus. China will announce its 2023 growth target in March and they should be concerned about slowing global growth and weak external demand.

- China’s factory activity bounced back in January and expanded for the first time since September. The official manufacturing PMI rose to 50.1 in January, above the 50-point mark that separates growth from contraction. That’s compared to December’s reading of 47. The official non-manufacturing PMI rose to 54.4, the highest level since June 2022. It was a sharp improvement from a reading of 41.6 from the previous month, backed by a strong recovery in services and construction activities.

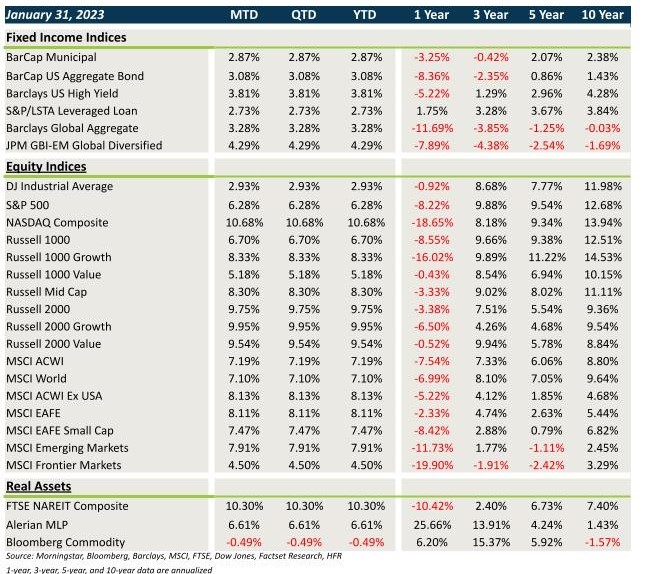

Market Performance (as of 01/31/23)

Fixed Income

- Yields fell sharply across the globe, providing a nice backdrop for fixed income.

- Core fixed income and munis gained ground while spreads tightened in riskier credit.

- USD weakness provided another significant boost for non-U.S. assets.

- After a terrible, outlier year for bonds in 2022, 2023 is off to a much better start.

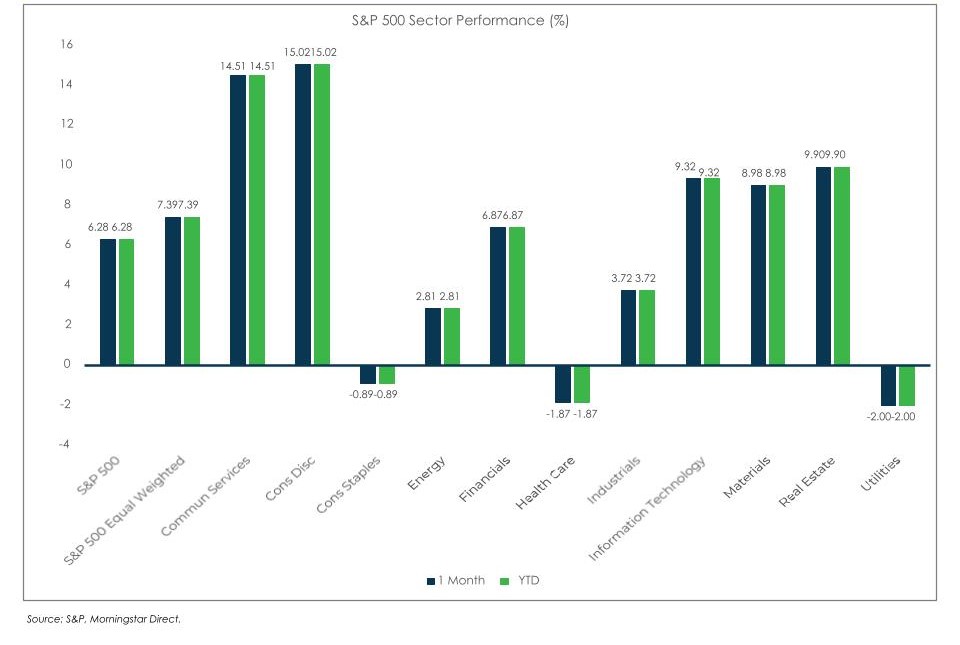

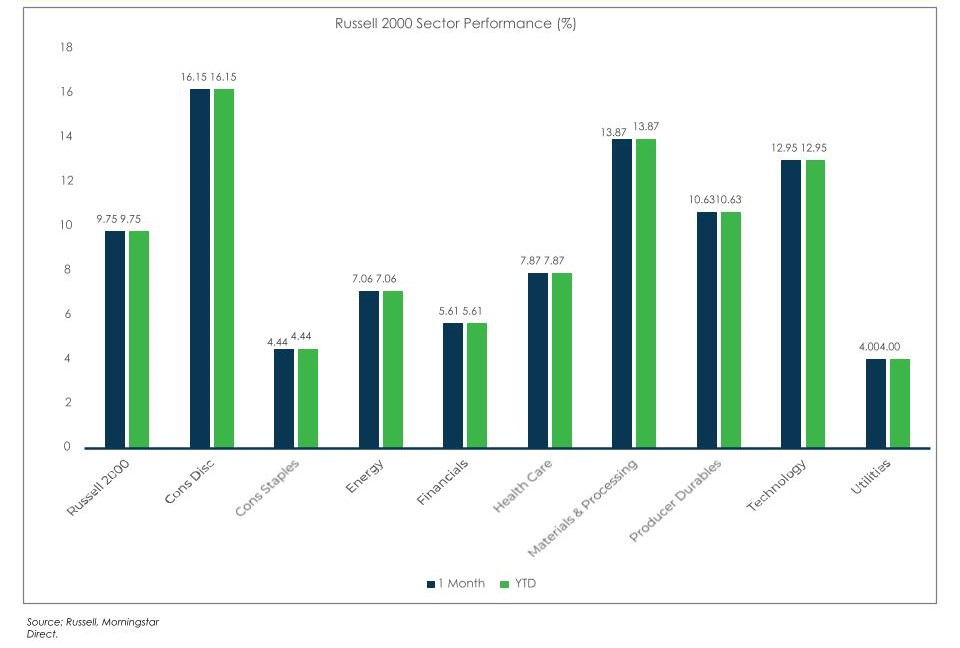

U.S. Equities

- Equities and other risk assets were off to the races as the calendar flipped to January.

- U.S. equities rose across all areas, led by tech/growth stocks and small caps.

- Growth beat value and small caps generally outperformed large caps.

Non-U.S. Equities

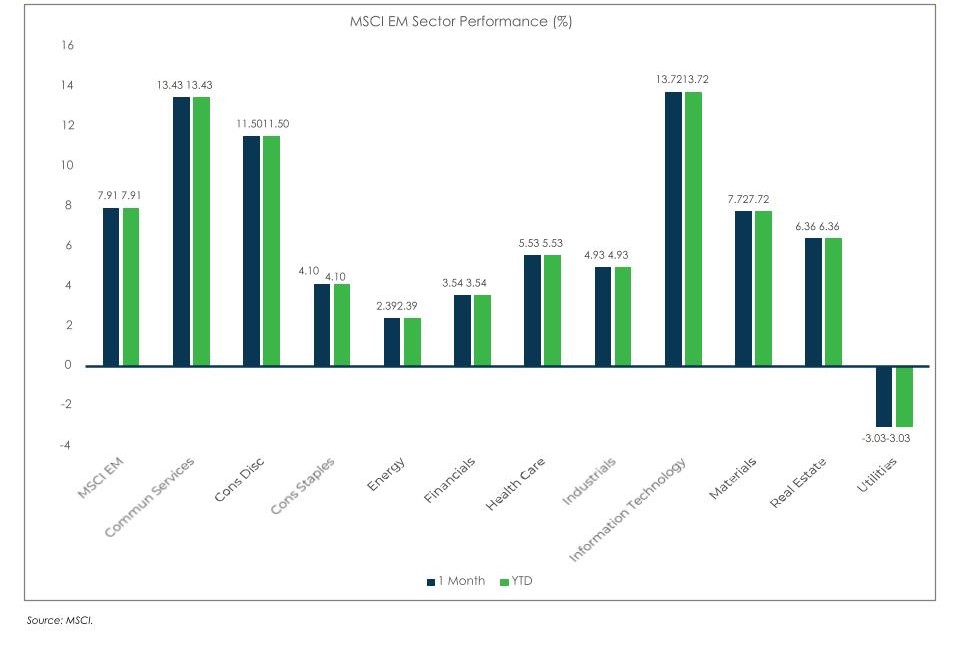

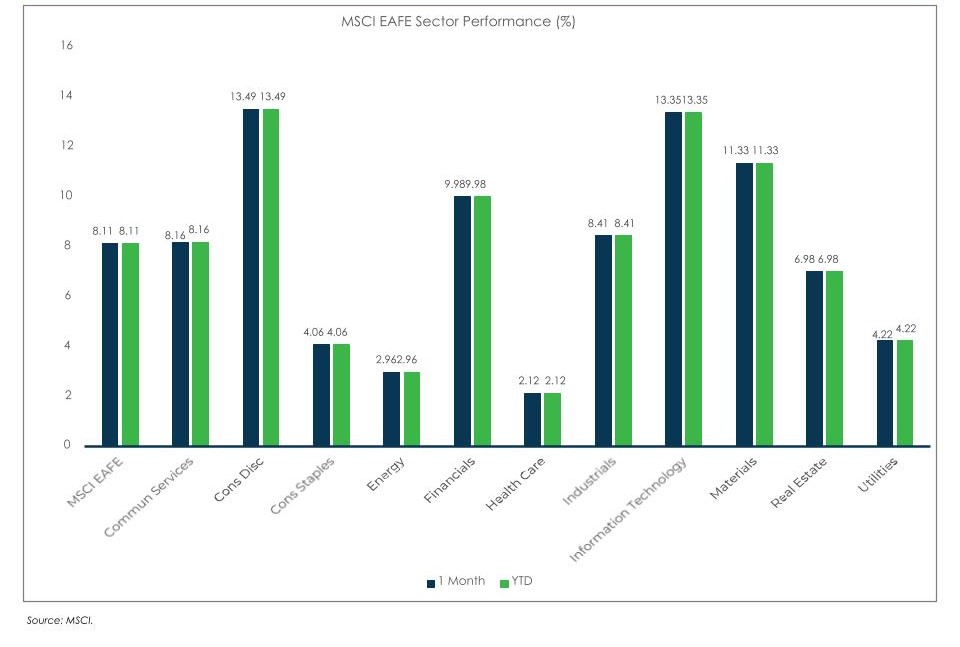

- Non-U.S. equities gained 7-8% in January with solid performance from all regions.

- Europe drove gains in the EAFE Index and China powered the EM Index higher.

- Small caps lagged large caps outside the U.S.

- USD weakness added 180 bps to EAFE returns and 136 bps for EM returns.

S&P 500 (as of January 31, 2023)

Russell 2000 (as of January 3, 2023)

MSCI EAFE (as of January 3, 2023)

MSCI EM (as of January 31, 2023)