Market Flash Report | January 2024

Economic Highlights

United States

- The January employment report blew past expectations with 353,000 new jobs added to the economy. The unemployment rate held steady at 3.7% and average hourly earnings surged 0.6% M/M or 4.5% Y/Y. The December report was also revised sharply higher. The Fed Fund Futures priced out a March rate cut, but markets still expect ~5 rate cuts this year starting in May.

- The Federal Reserve held rates steady at its January meeting and disappointed markets a bit by not signaling more willingness to cut rates starting at the March meeting. Chair Powell indicated that inflation is trending towards its target, but the Fed is looking for more confirmation before beginning an easing cycle. We believe the key here is that rate hikes are finished and it is only a matter of when the Fed starts cutting rates, as they are certainly too restrictive today relative to the level of inflation.

- For the second consecutive quarter, U.S. economic growth showed strength and outperformed economist expectations. GDP grew 3.3% in Q4, well ahead of the 2% estimate, but below the 4.9% pace in Q3. Personal consumption expenditures increased 2.8% for the quarter, down just slightly from the previous period. State and local government spending also contributed, up 3.7%, as did a 2.5% increase in federal government expenditures. Based on initial estimates, the U.S. economy grew 2.5% in 2023.

- The Fed’s preferred inflation gauge, the Core PCE Index, increased 0.2% M/M in December or 2.9% Y/Y. On a monthly basis, core inflation increased from 0.1% in November, but the annual rate declined from 3.2%. The annual rate is the lowest since March 2021. Including volatile food and energy costs, headline inflation also rose 0.2% for the month and held steady at 2.6% annually. Within the inflation numbers, prices for goods declined by 0.2% while services prices rose by 0.3%. One other key data point was the personal savings rate, which fell from 4.1% to 3.7%.

- The U.S. manufacturing sector strengthened in January, but remained in contraction territory. New orders rebounded sharply back above 50 while production was flat, and employment fell slightly. The employment reading of 47.1 suggests hiring weakness across the sector.

Non-U.S. Developed

- Business activity in the eurozone fell at the slowest rate for six months in January, according to flash PMI data, albeit with downturns persisting in both manufacturing and services amid further declines in new business. Inflation remains an issue across the eurozone, but the broad economic weakness should lead to the European Central Bank (ECB) cutting rates as opposed to implementing any increases. When assessing the performance of Germany and France, it is only a question of who is having the tougher time.

- Inflation in the eurozone fell from 2.9% in December to 2.8% in January. Core inflation decreased to 3.3% in January from 3.4% in December. Most of the decline came from the energy sector. Services inflation showed a rise of 4%, consistent with the prior month. Markets expect the ECB to start easing in April, but the central bank stresses that it is data dependent.

- Japan's core CPI climbed 3.1% last year to mark its biggest gain since 1982, driven up by rising food costs and as a weaker yen made imports more expensive. For the month of December, the core index, which excludes fresh food, increased 2.3% from a year earlier, down from 2.5% in November and surpassing the Bank of Japan's inflation target of 2% for the twenty-first straight month.

Emerging Markets

- The Chinese economy grew 5.2% in Q4 2023, but slightly missed expectations. GDP growth for the full year was also 5.2%, compared with a 3% increase in 2022. Investment into real estate fell by 9.6% in 2023, while those into infrastructure and manufacturing rose by 5.9% and 6.5%, respectively.

- Retail sales rose 7.4% in December from a year earlier, missing expectations for 8% growth. They rose by 7.2% for the full year.

- Looking ahead to 2024, the Chinese economy faces a number of challenges including weak domestic demand, sluggish external demand, overcapacity in some industries and weak expectations for future growth. The bursting property bubble is another significant challenge for the government.

- The International Monetary Fund (IMF) upgraded its global growth outlook on the heels of the strong, resilient U.S. economy and policy support measures from China. It increased its 2024 forecast from 2.9% to 3.1% and maintained its 2025 projection of 3.2%. The IMF also cited stronger-than-anticipated growth in EM countries like Brazil and India. The IMF forecasts growth this year of 2.1% in the U.S., 0.9% in both the eurozone and Japan, and 0.6% in the United Kingdom.

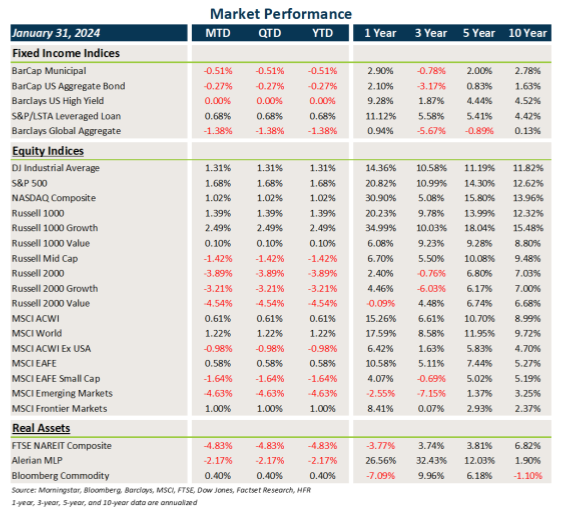

Market Performance (as of 01/31/24)

Fixed Income

- Treasury and other sovereign debt yields moved higher in January, and this led to losses in core fixed income and municipal bonds.

- Credit generally benefited from its higher carry entering the year, helping to offset the move higher in Treasury yields. Investment grade was modestly positive, high yield was flat, and loans gained ground.

- After weakening in Q4, the USD strengthened last month, creating a headwind for non-U.S. assets.

U.S. Equities

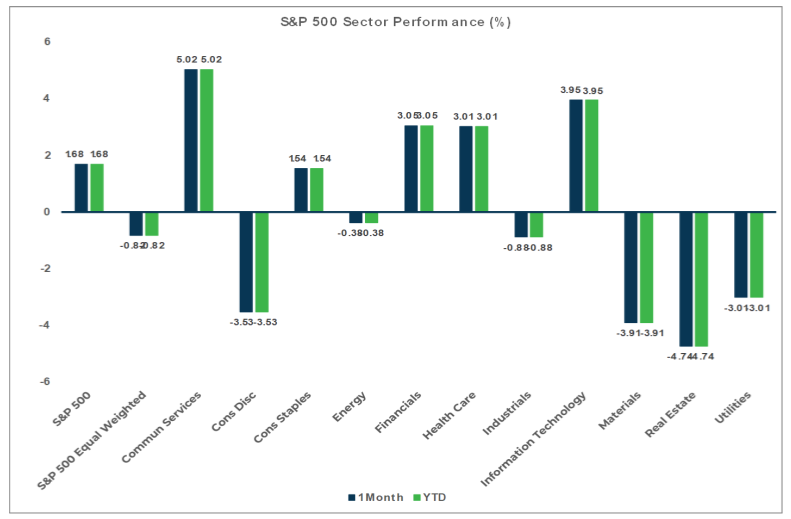

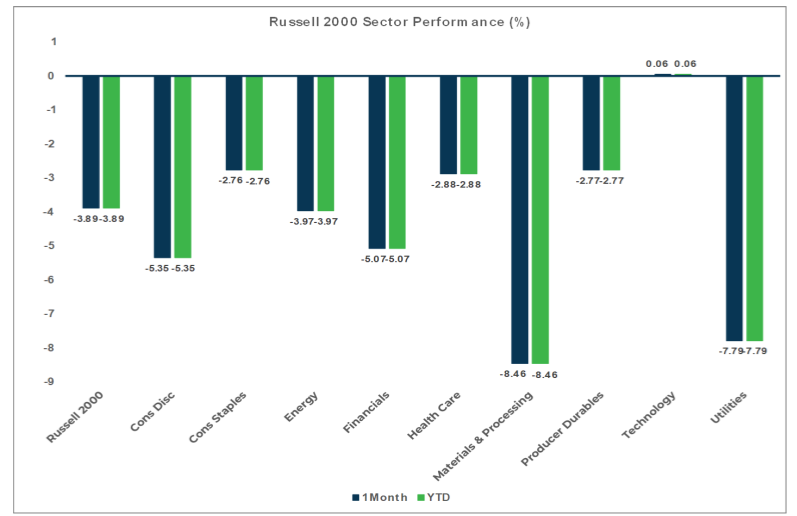

- U.S. equities were a mixed bag in January, with gains in large caps and losses in small caps.

- Growth once again led value across all market capitalizations, and large caps trounced small caps.

- Similar to most of 2023, U.S. equities were led by only a handful of mega-cap tech stocks.

Non-U.S. Equities

- Non-U.S. equities started the month on a weak note, but rallied over the final week to post slight gains across developed markets.

- Similar to what occurred in the U.S., EAFE markets saw growth beating value and large caps outperforming small caps.

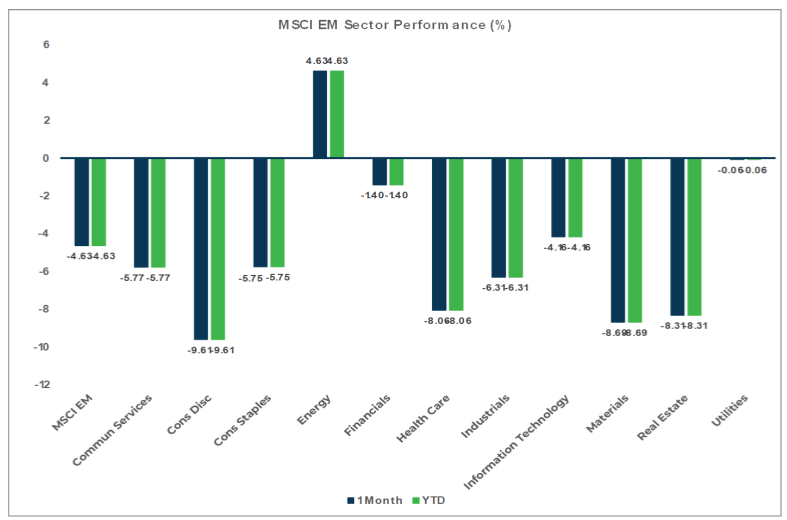

- The big story in January was the continued weakness in emerging markets, specifically driven again by China.

Sector Performance - S&P 500 (as of 01/31/24)

Sector Performance - Russell 2000 (as of 01/31/24)

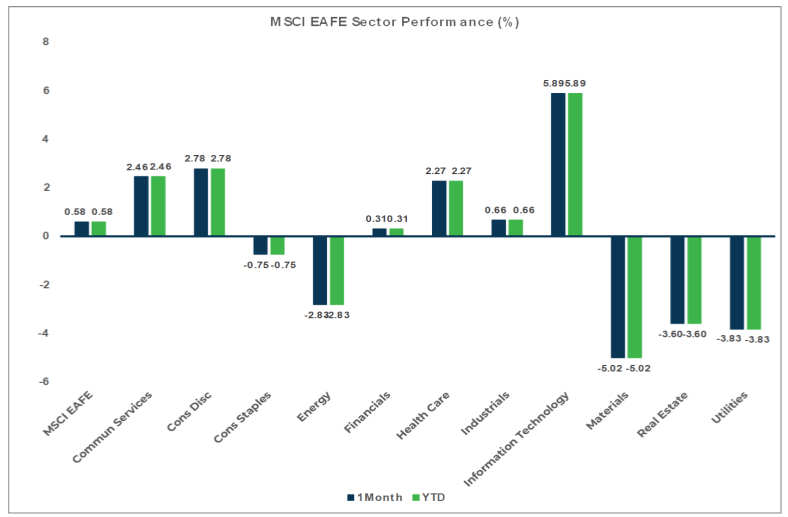

Sector Performance - MSCI EAFE (as of 01/31/24)

Sector Performance - MSCI EM (as of 01/31/24)