Market Flash Report | July 2022

Economic Highlights

United States

- Nonfarm payrolls increased 372,000 in June, better than the 250,000 estimate and continuing what has been a strong year for job growth. The unemployment rate was 3.6%, unchanged from May and in line with estimates. An alternative measure of unemployment that includes discouraged workers and those holding part-time jobs for economic reasons fell sharply, dropping to 6.7% from 7.1%. The May and April reports were revised downward. Average hourly earnings rose 0.3% M/M or 5.1% Y/Y. Education and health services led job creation, followed by professional and business services and leisure and hospitality. The robust employment market continues to be the counter argument against the U.S. economy being in recession.

- Inflation rose at its fastest pace since November 1981. U.S. consumer prices increased at a 9.1% annualized rate in June, ahead of the 8.8% estimate and last month’s reading. Excluding volatile food and energy prices, core CPI increased 5.9%, compared with the 5.7% estimate. Core inflation peaked at 6.5% in March and has been nudging down since. Energy prices surged 7.5% on the month and were up 41.6% on a 12-month basis. The food index increased 1%, while shelter costs, which make up about one-third of the CPI, rose 0.6% for the month and were up 5.6% annually. June inflation was hotter than expected and counter the narrative that inflation is peaking.

- The Federal Reserve raised rates by another 75 bps at its July meeting, bringing the Fed funds target rate to a range of 2.25% - 2.50%. Jerome Powell would not specifically commit to a rate path forward, suggesting future rate hikes will be data dependent. With CPI, PCE and wage growth showing little sign of easing, the Fed may have more work to do either through an emergency rate hike or another significant move at its September meeting. They have a delicate balancing act right now as Q2 GDP growth contracted for the second straight quarter. The U.S. economy may be teetering on the brink of a recession and further rate hikes could cause more demand destruction. Markets have been doing the job for the Fed as the housing market has slowed sharply with higher mortgage rates. Other interest rate sensitive parts of the economy are also showing signs of slowing.

Non-U.S. Developed

- Eurozone GDP grew 0.7% in Q2, well ahead of the 0.2% expectation. The better than expected and acceleration in economic growth comes at a time of high inflation and concern over energy costs. Most economists expect the eurozone economy to contract in Q3.

- The eurozone economy contracted in July, according to early PMI survey indicators, with output and new orders both falling for the first time since the COVID-19 lockdowns of early 2021. An accelerating downturn in manufacturing was accompanied by a near-stalling of service sector growth as the rising cost of living continued to erode the tailwind of pent-up demand from the pandemic. The latest eurozone composite PMI fell from 52 in June to 49.4 in July. The eurozone economy looks set to contract in Q3 as business activity slipped into decline in July and forward-looking indicators hint at worse to come in the months ahead.

- Japan's government slashed its economic growth forecast for this fiscal year largely due to slowing overseas demand, highlighting the impact of Russia's war in Ukraine, China's strict COVID-19 lockdowns and a weakening global economy. The Bank of Japan now expects GDP to grow 2% in 2022, down from the previous estimate of 3.2% growth. Most of the decline stems from reduced exports. The BOJ expects GDP growth of 1% in 2023.

Emerging Markets

- China eked out GDP growth of 0.4% in the second quarter from a year ago, missing expectations as the economy struggled to shake off the impact of COVID-19 controls. The Q2 reading was sharply lower than the 4.8% increase during Q1 and far below the 1% growth estimated by economists. On a quarterly basis, GDP shrank 2.6%. The Chinese government faces mounting challenges to keep growth steady, as the country contends with a sharp slowdown in activity due to Beijing's stringent zero-COVID policy, a bruising regulatory crackdown on the private sector, and a real estate crisis that is causing rising bad debts at banks and growing social protests.

- Chinese industrial production in June also missed expectations, rising by 3.9% from a year ago, versus the 4.1% forecast. However, retail sales in June rose by 3.1%, recovering from a prior slump and beating expectations for no growth from the prior year. Major e-commerce companies held a promotional shopping festival in the middle of last month. Fixed asset investment for the first half of the year came in above expectations, up 6.1% versus 6% predicted.

- China’s factory activity contracted unexpectedly in July after bouncing back from COVID-19 lockdowns the month before, as fresh virus flare-ups and a darkening global outlook weighed on demand. The official manufacturing PMI fell from 50.2 in June to 49.0 in July. The official non-manufacturing PMI in July fell to 53.8 from 54.7 in June. In addition, the smaller company-focused Caixin manufacturing PMI also fell sharply in July.

- Last week, the International Monetary Fund (IMF) slashed its global growth forecast to 3.2% (from 3.6%) with downside risks being high inflation and the war in Ukraine. The IMF also believes the global economy is teetering on the brink of a recession. The IMF cut its growth projections for the U.S., China and the eurozone. They also reduced their 2023 forecast for global growth from 3.6% to 2.9%.

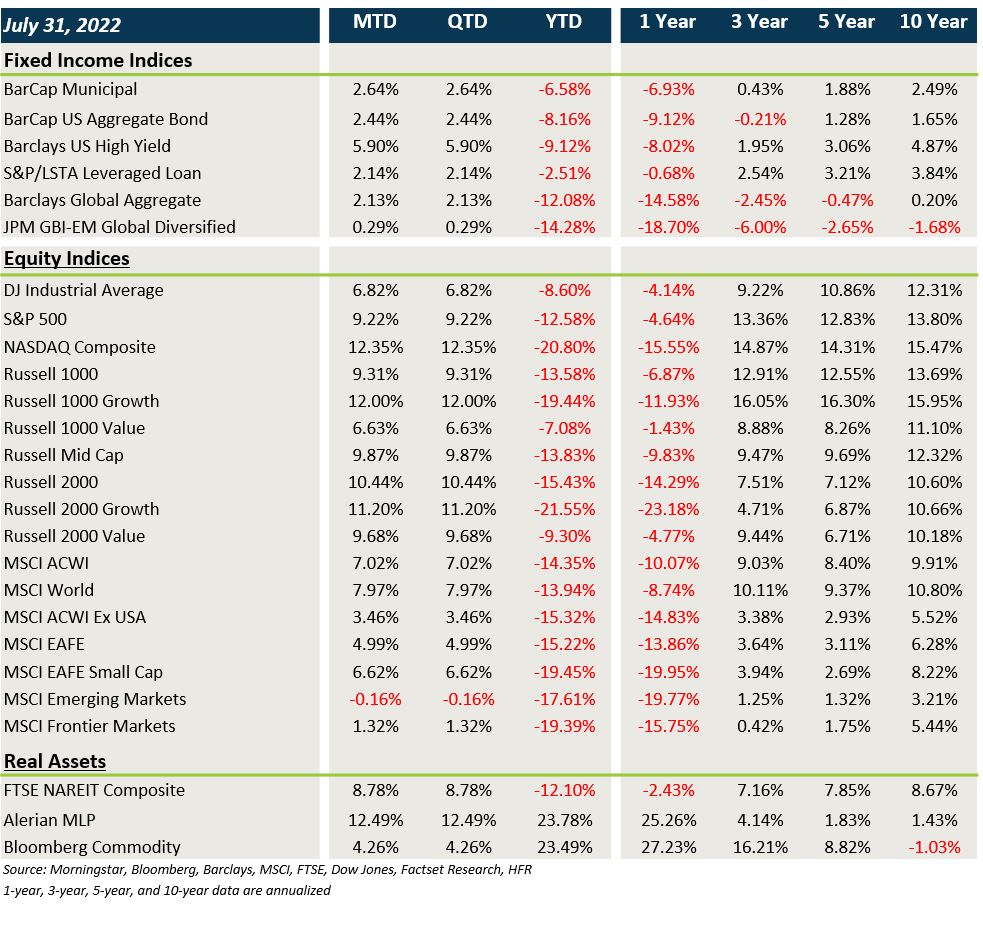

Market Performance (as of 7/31/22)

Fixed Income

- Yields fell sharply in July and this led to strong gains across fixed income, specifically core and munis.

- Credit spreads also tightened leading to outsized gains in IG, high yield and floating rate loans.

- Gains were more muted in non-U.S. fixed income due to USD strength.

U.S. Equities

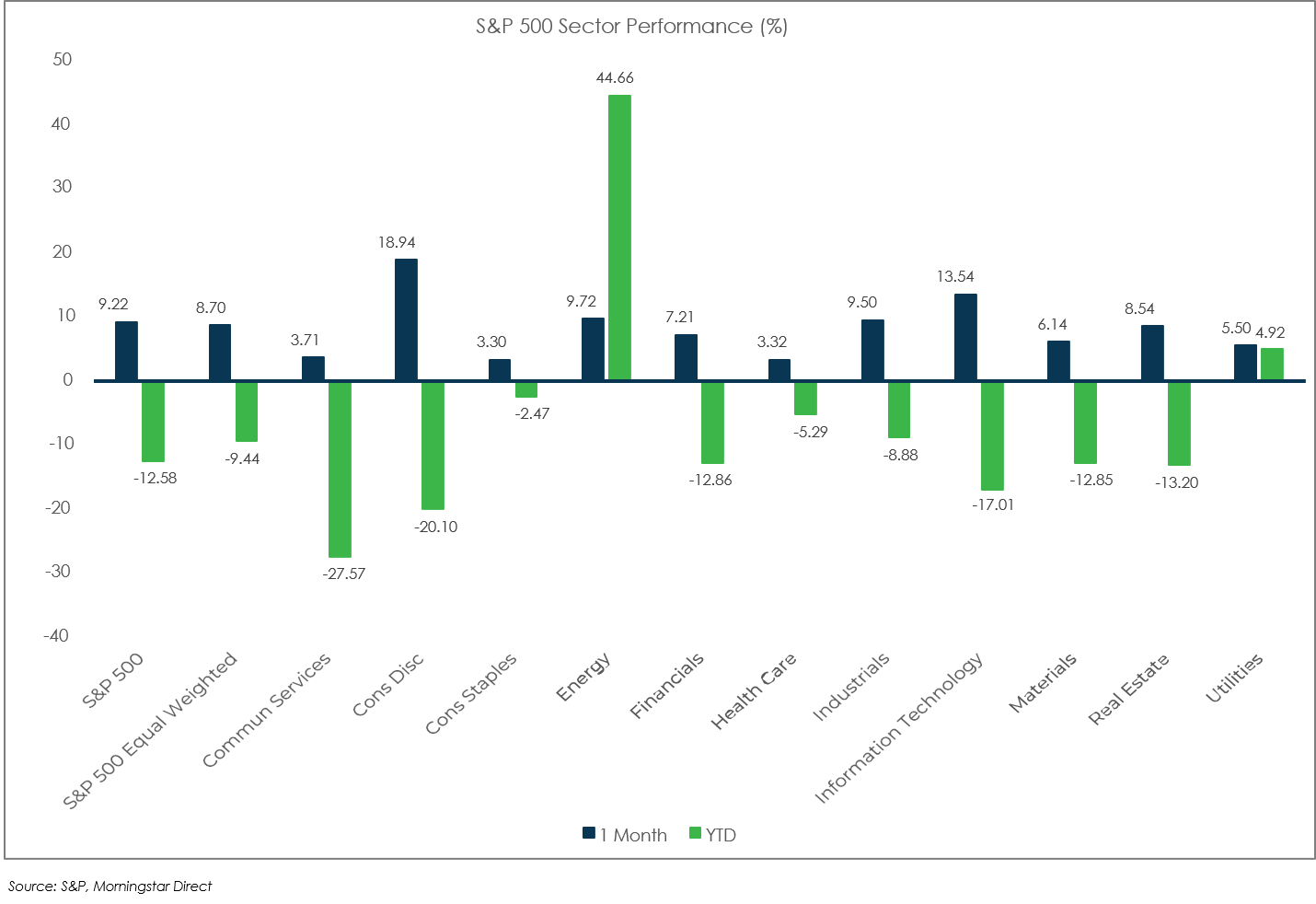

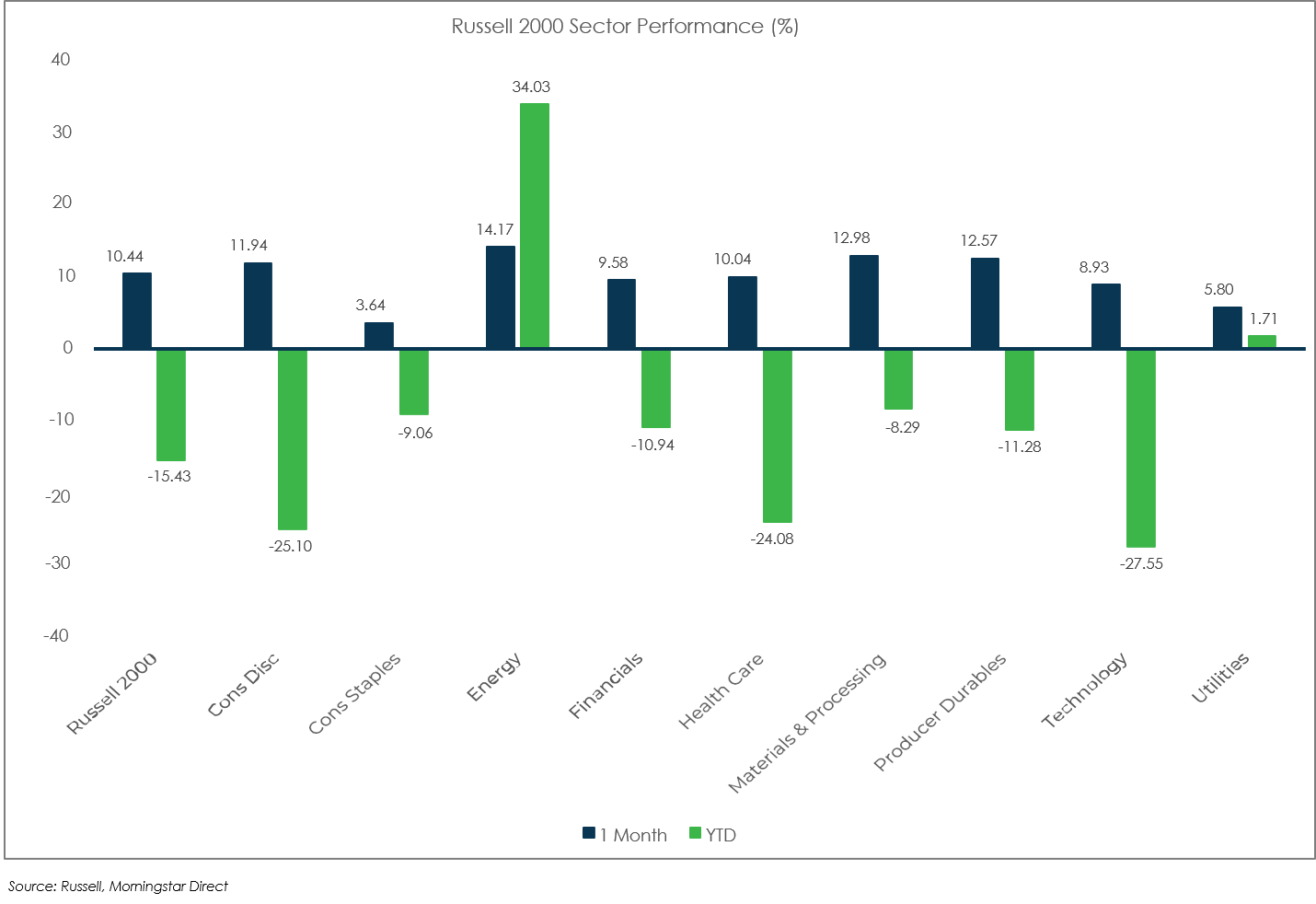

- U.S. equities posted strong gains in July led by a strong rebound in growth/tech stocks and small caps.

- Growth led value last month and small caps slightly outperformed large caps.

- The S&P 500 gained 9.2% in July but is still down 12.6% YTD.

Non-U.S. Equities

- Non-U.S. equities posted solid gains last month although they lagged their U.S. counterparts.

- Similar to the U.S., growth trounced value and small caps beat large caps.

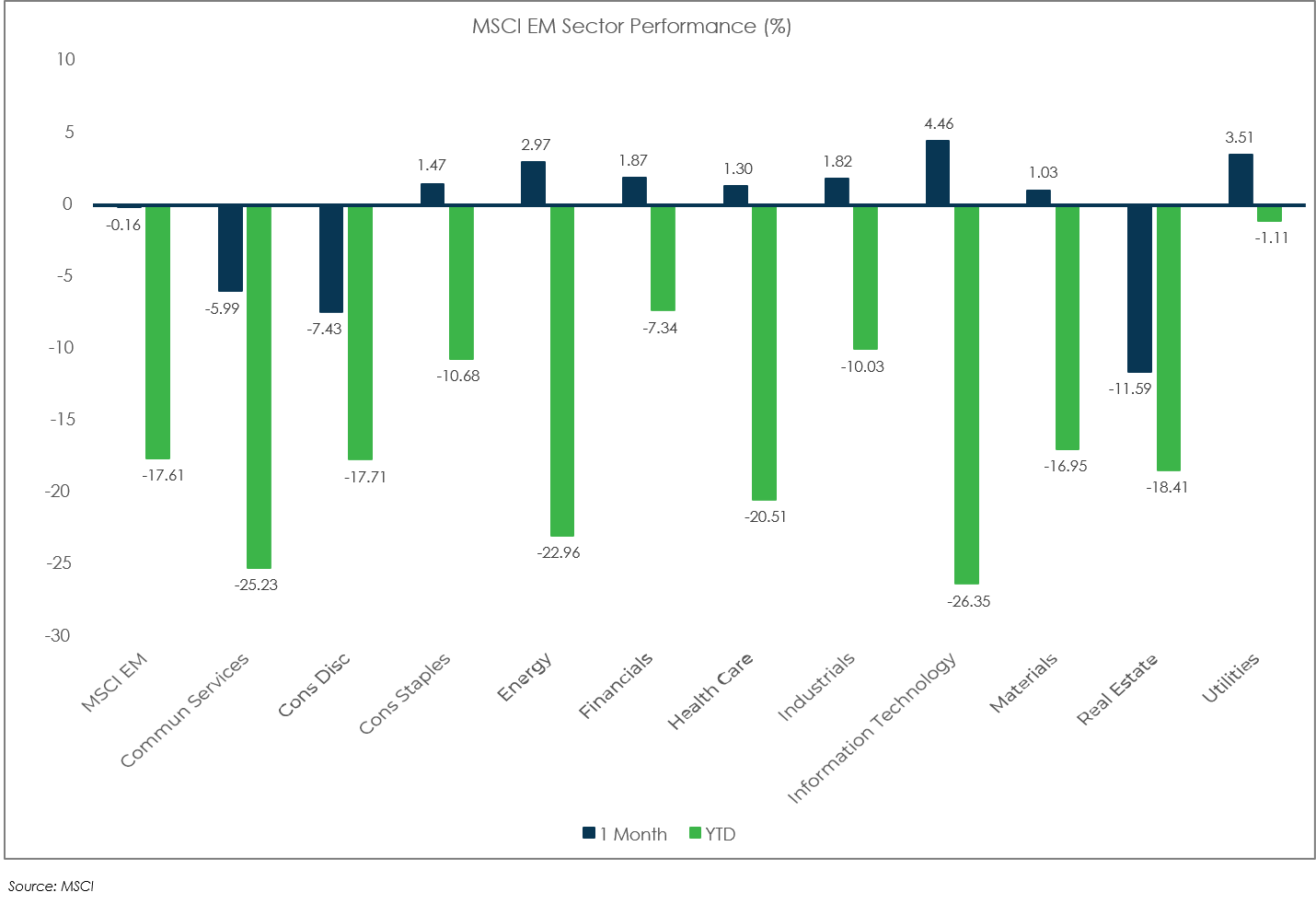

- EM stocks lost ground in July, largely due to weakness in China.

- The strong USD continues to provide a headwind for non-U.S. assets.

Sector Performance

S&P 500 (as of July 31, 2022)

Russell 2000 (as of July 31, 2022)

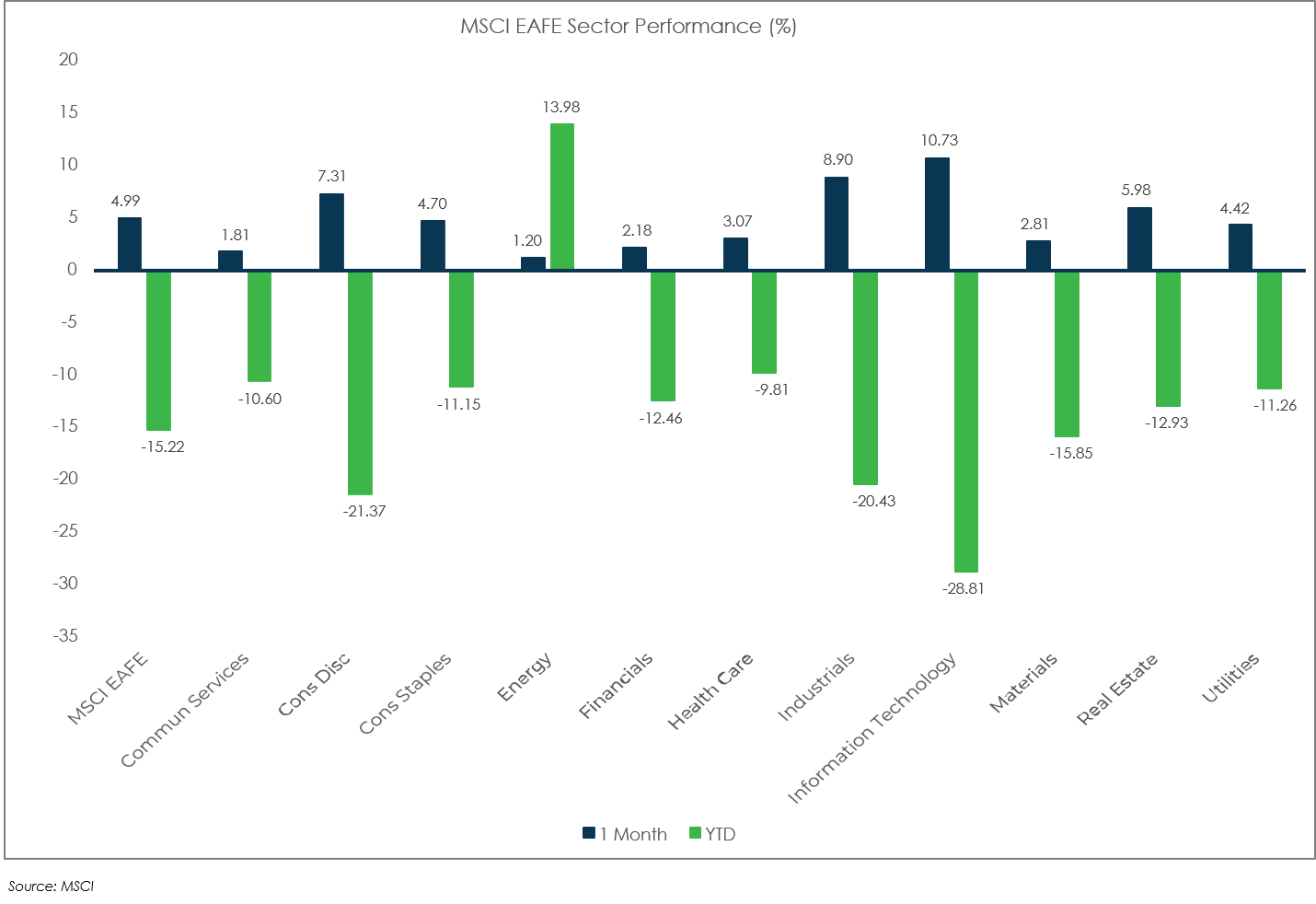

MSCI EAFE (as of July 31, 2022)

MSCI EM (as of July 31, 2022)