Market Flash Report | June 2022

Economic Highlights

United States

- The Federal Reserve delivered a widely anticipated 75 bps rate hike on June 15, while also launching its plan for quantitative tightening. The Fed Funds Rate increased from a range of 0.75%-1.00% to a new range of 1.50%-1.75%. Its updated economic projections showed inflation remaining higher over the next few years while economic growth is now seen at a below-trend 1.7% this year and next, with the unemployment rate rising back above 4% by 2024. The updated dot chart implies another 175 bps of rate increases by the end of 2022 with rates peaking between 3.5-4% in 2023. The Fed appears to be committed to bringing down inflation, but we ultimately believe economic and market data will drive future decisions. We expect rates to move higher, but also believe the Fed put is not dead and either a pause or rate cuts could occur if the economy slows or markets exhibit continued weakness.

- The 390,000 new jobs added to the U.S. economy in May exceeded expectations. The unemployment rate held steady at 3.6% and average hourly earnings moderated a bit at an annualized rate of 5.2%. The strength of payrolls in May was widespread, with solid gains in professional & business services employment (+75,000), leisure & hospitality (+84,000), construction (+36,000) and manufacturing (+18,000). One weak spot was retail, where employment fell by 61,000. Elements of the May report show signs of a deceleration in wage growth, but thus far the slowing is not sufficient to let the Fed alter its plans for additional 50 bps rate hikes.

- Inflation rose at its fastest pace since December 1981 in May. CPI surged 8.6% Y/Y last month with the core rate jumping 6%. Both headline and core inflation exceeded expectations in May. Shelter costs, which account for about a one-third weighting in the CPI, rose 0.6% for the month, the fastest one-month gain since March 2004. The 5.5% 12-month gain is the most since February 1991. Energy prices rose 3.9% M/M in May while food prices climbed another 1.2%. Airfares and used car prices also saw sharp increases. This report was disappointing across the board. Inflation remains a major concern for markets and the Fed Fund Futures now point to at least 175 bps more of rate hikes by year-end. While we think a more hawkish Fed is likely, we also don’t believe the Fed put is dead if market volatility continues and the economy dips into recession.

- U.S. PCE remained unchanged at 6.3% on a year-over-year basis, though U.S. Core PCE fell by 0.2% to 4.7% Y/Y, its third consecutive monthly decline, demonstrating potential signs of easing inflation.

Non-U.S. Developed

- The eurozone economy showed further signs of slowing based on the S&P Global Composite PMI. The reading fell from 54.8 in May to 52.0 in June, a 16-month low. Weighing on the performance in June was the first fall in manufacturing production in two years and a weaker rate of increase in services business activity. All major countries exhibited slower rates of growth led by Ireland, which hit a 16-month low and France, which hit a 14-month low. The sharp deterioration in the rate of growth of eurozone business activity raises the risk of the region slipping into economic decline in the third quarter.

- Japan’s economy shrank at an annualized rate of 0.5% in Q1, slightly better than the preliminary reading of a 1% contraction. Consumer spending and other private demand was stronger than previously thought. One source of worry is the diving value of the yen, now trading at a 20-year low of about 135 yen to the U.S. dollar.

Emerging Markets

- China's manufacturing activity expanded at its fastest in 13 months in June, buoyed by a strong rebound in output, as the lifting of COVID-19 lockdowns sent factories racing to meet recovering demand. The official Manufacturing PMI for China rose to 50.2 in June from 49.6 in the prior month. The smaller company-focused Caixin/Markit manufacturing PMI rose to 51.7 in June, also indicating the first expansion in four months, from 48.1 in the previous month.

- Looking at the consumer side of the economy, the official service sector PMI surged to 54.7 in June of 2022 from 47.8 in May. This was the first expansion in the service sector in four months and the strongest growth since May 2021. A similar jump was seen in the smaller business focused Caixin Services PMI that increased from 41.4 in May to 54.5 in June.

- China's economy has started to chart a recovery path out of the supply shocks caused by strict lockdowns, but headwinds persist, including record high jobless rates in big cities, a still subdued property market, soft consumer spending and fear of any recurring waves of infections. Analysts expect further improvement in economic conditions in the third quarter, although the official GDP target of around 5.5% for this year will be hard to achieve unless the government abandons the zero-COVID strategy.

- Brazil’s economy grew less than expected in the first quarter ahead of an expected downturn later this year, another setback to President Jair Bolsonaro as he readies his re-election bid. GDP grew 1% Q/Q, slightly behind the 1.2% expectation. In recent months, Brazil has seen a string of better-than-expected indicators such as retail and employment, prompting many economists to raise their year-end GDP projections. While Brazil is one of the few countries where GDP estimates have been on the rise, the country has a lot of potential headwinds on the horizon such as the presidential election, high inflation and tightening central bank policy that has already increased rates by 10%. Inflation is eating into consumer purchasing power and the result could be slower growth during the second half of 2022.

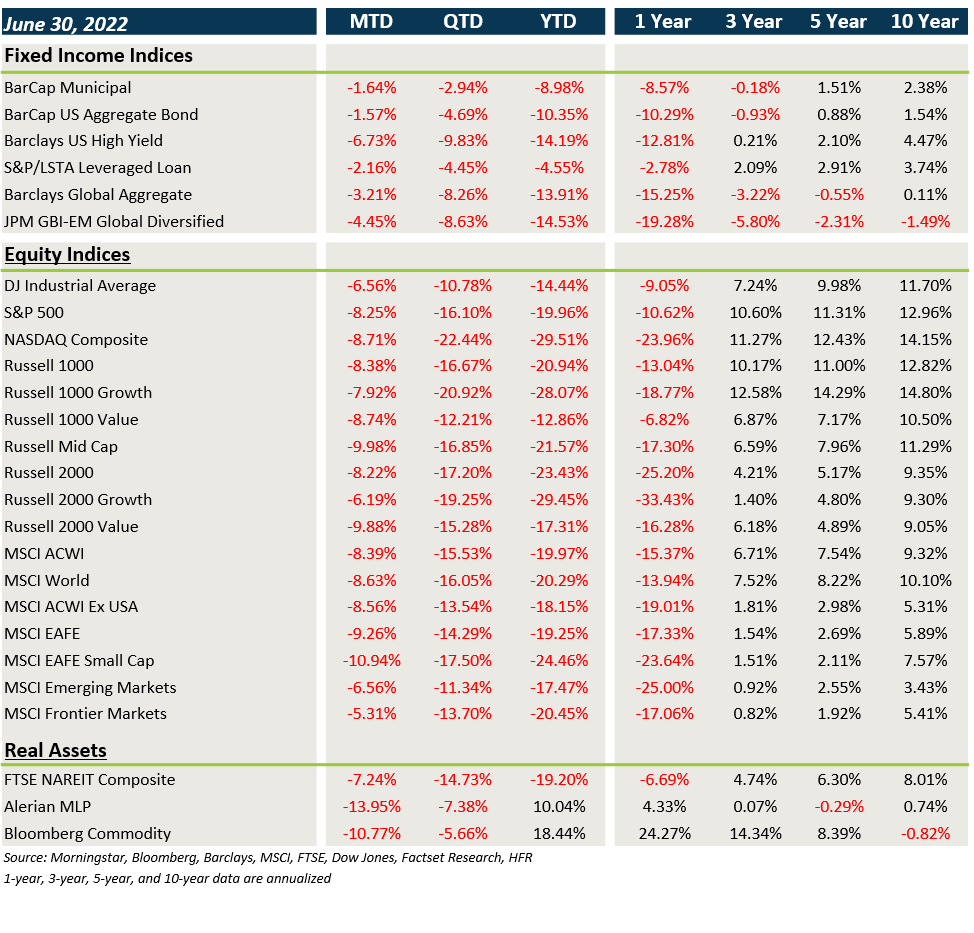

Market Performance (as of 6/30/22)

Fixed Income

- Yields continued their march higher in June and this led to another difficult month for core fixed income and munis.

- Credit was hit hard in June with cracks finally emerging in HY, loans and EMD.

- The stronger U.S. dollar negatively impacted non-U.S. assets.

U.S. Equities

- U.S. equities were weak across the board last month, led by particular weakness in small cap value.

- Growth outperformed value in June and there was little difference between small caps and large caps.

- The Nasdaq has fallen 29.5% YTD.

Non-U.S. Equities

- Non-U.S. equities generally underperformed U.S. equities in June, but currency provided a major headwind.

- Similar to the U.S., value lagged growth, but small caps underperformed large caps.

- The stronger U.S. dollar cost investors last month as it added to already negative local returns.

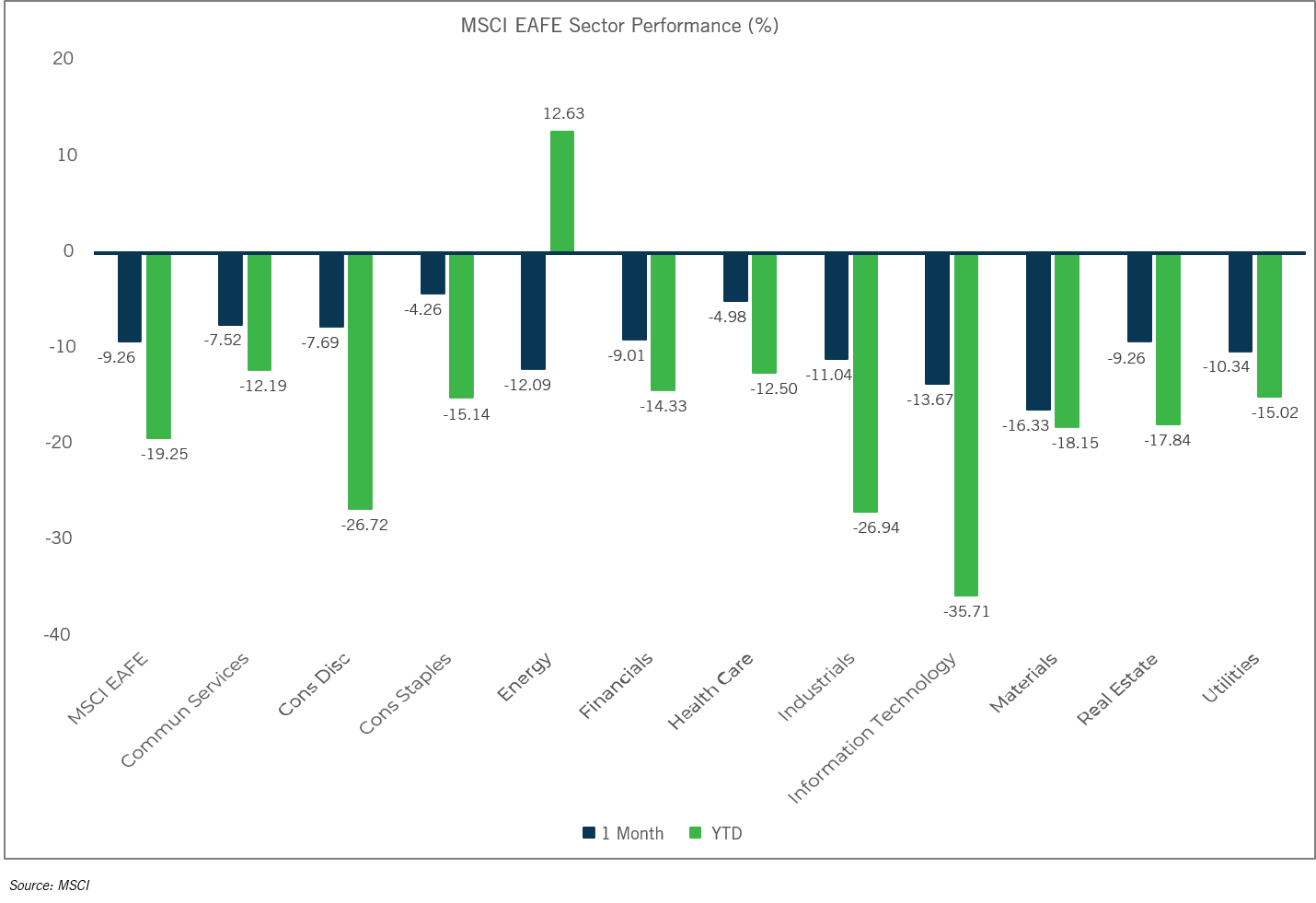

Sector Performance

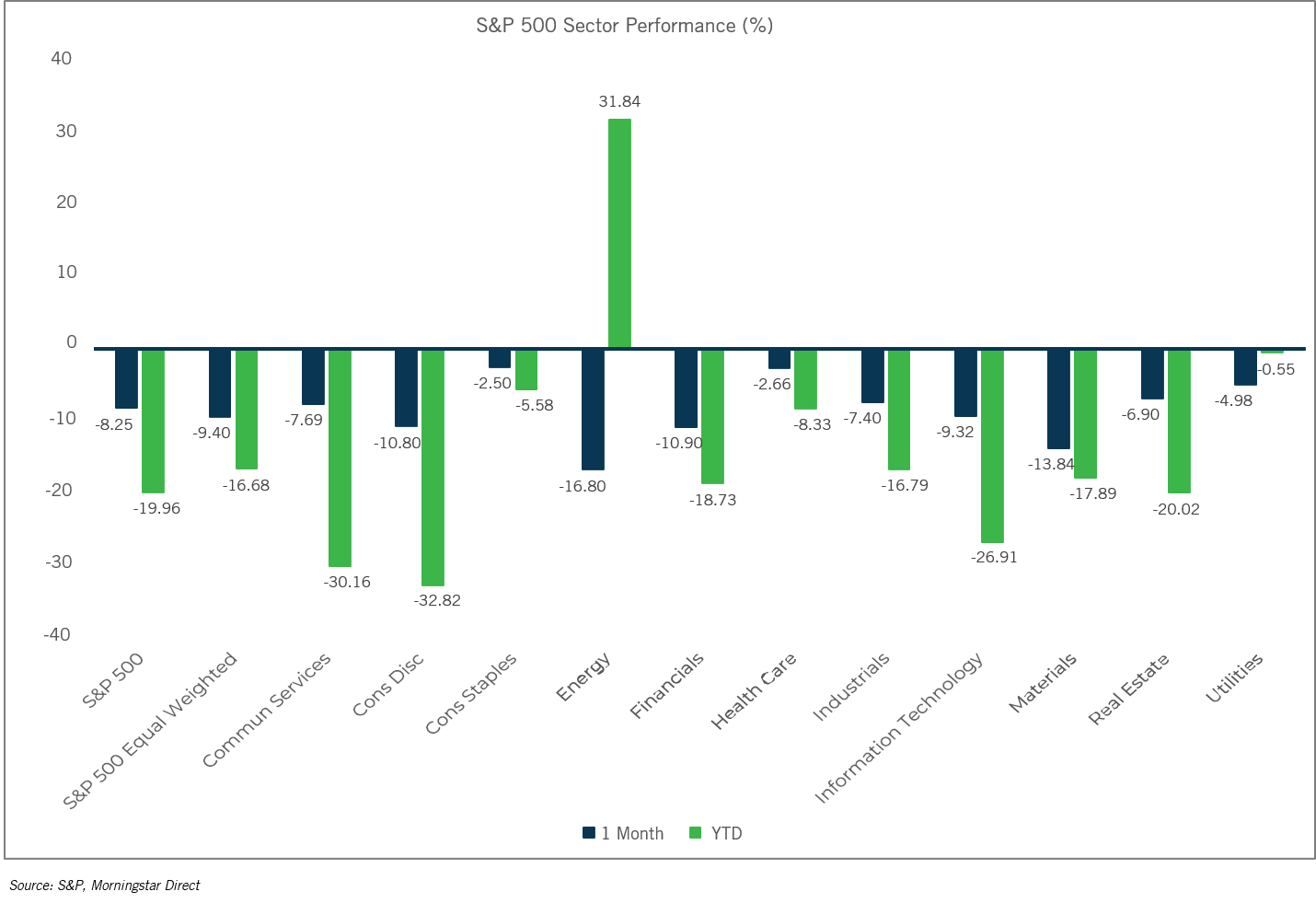

S&P 500 (as of June 30, 2022)

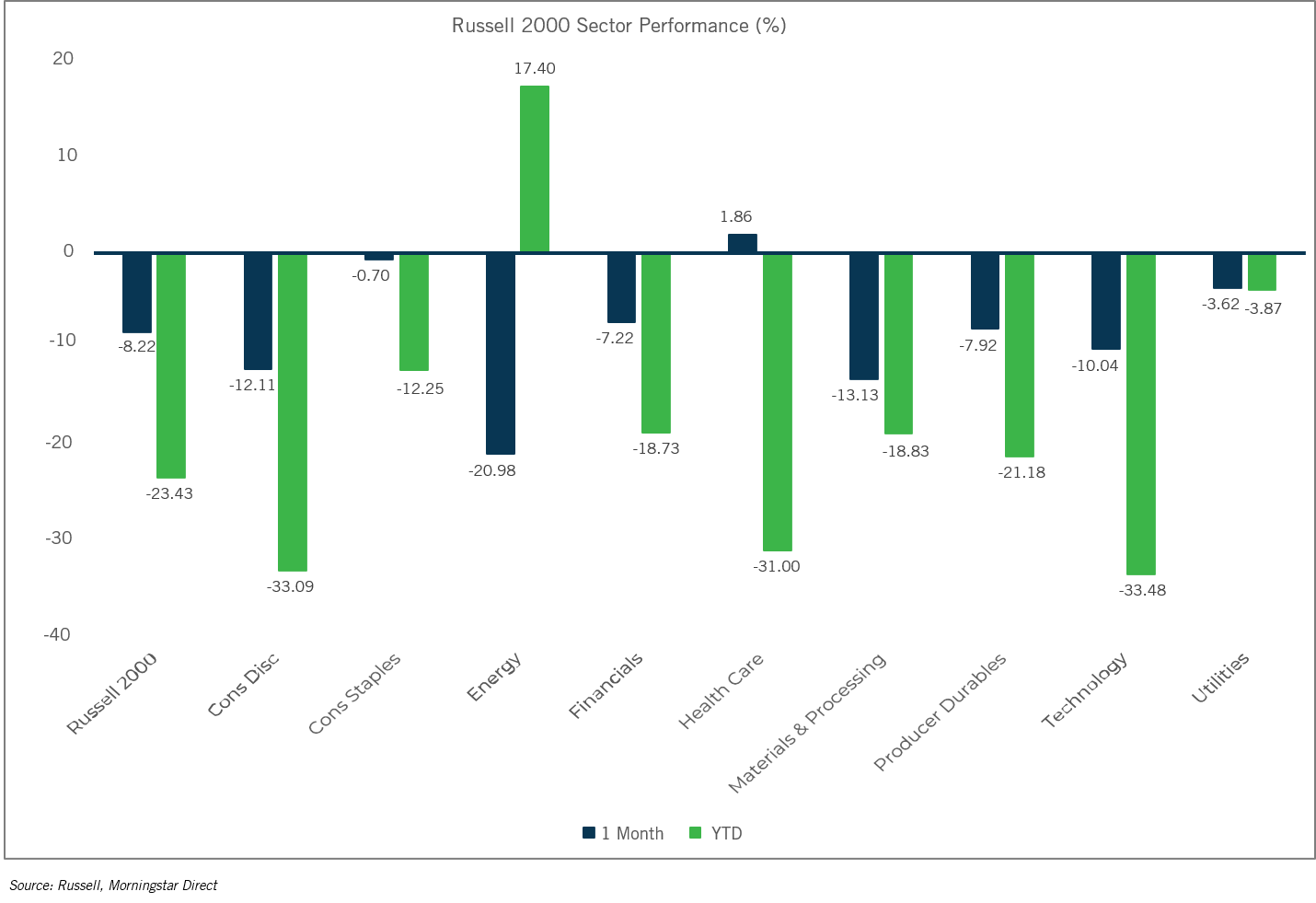

Russell 2000 (as of June 30, 2022)

MSCI EAFE (as of June 30, 2022)

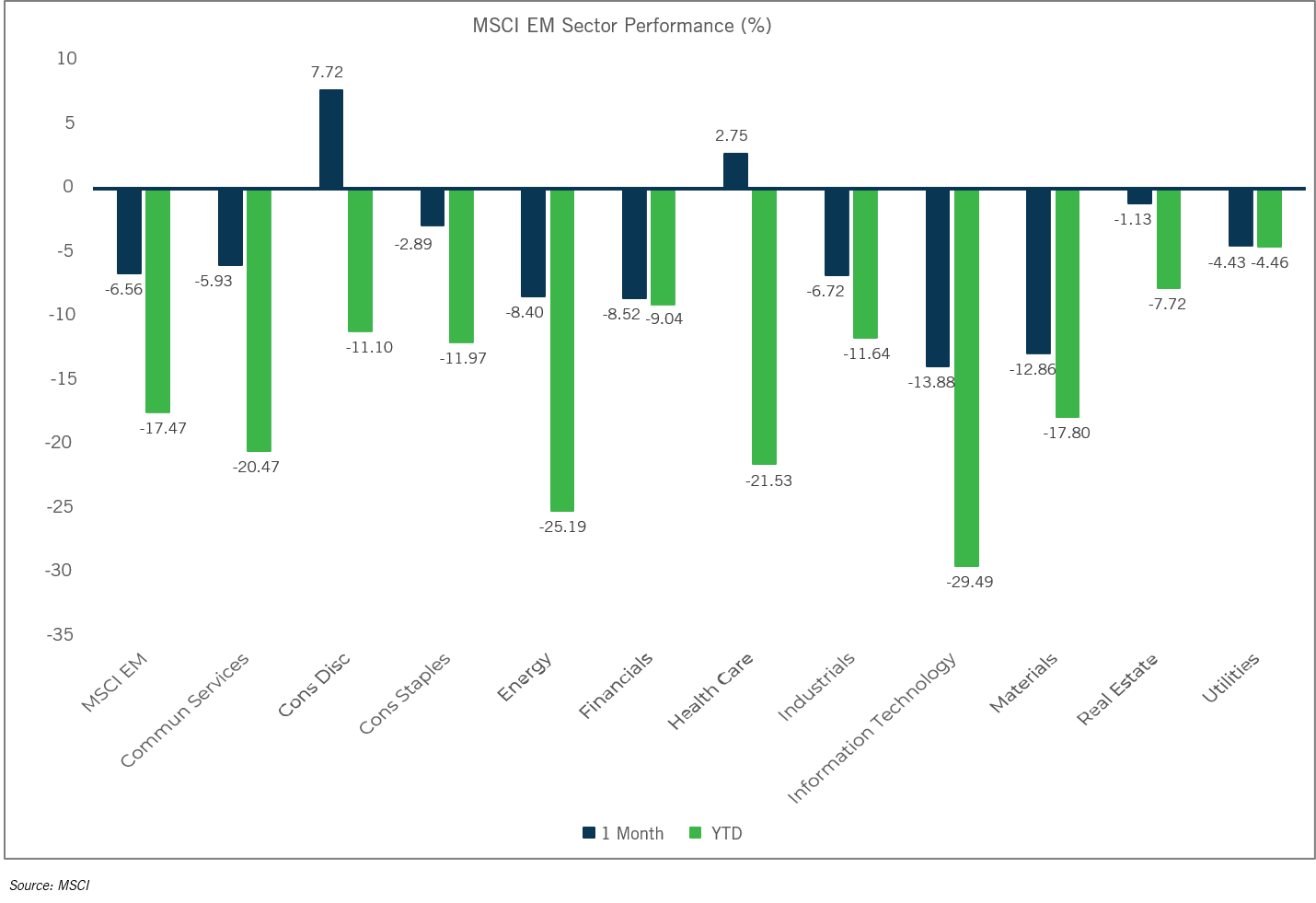

MSCI EM (as of June 30, 2022)