Market Flash Report | March 2022

Economic Highlights

United States

- The U.S. economy grew 7% Y/Y during Q4, but estimates for the first quarter of 2022 have come way down due to Fed/inflation expectations and the impact from the Russia-Ukraine conflict. Economists now expect the U.S. economy to grow 0-1% in Q1, well below earlier estimates. Q1 has been a traditionally weak period for growth due to some seasonality, but higher prices are clearly impacting sentiment and consumer spending. The latest GDP estimate from the Atlanta Fed sits at 0.9%.

- The April employment report showed continued strength in the U.S. labor market. Employers added 431,000 new jobs to the economy, slightly below the estimate of 490,000. Revisions from prior months also were strong. January’s total rose 23,000 to 504,000, while February was revised up to 750,000 compared with the initial count of 678,000. For the first quarter, job growth totaled 1.685 million, a monthly average of nearly 562,000. The unemployment rate declined to 3.6% and the broader U6 unemployment rate fell to 6.9%. Average hourly earnings rose 5.6% Y/Y, in-line with expectations.

- All eyes are on the Fed and how hawkish monetary policy will need to be to counter surging inflation. The latest CPI/PCE readings are near the highest levels in 40+ years and there are few signs of cooling. The Fed hiked rates by 25 bps at its March meeting and has indicated 6 more rate hikes for the remainder of 2022 based on their dot chart. Markets are now pricing in as many as 8 more rate hikes this year including several 50 bps moves over the next few meetings. More Fed officials are also talking increasingly about balance sheet reduction.

- The ISM Manufacturing Index fell from 58.6 in February to 57.1 in March. New orders and production were particularly weak while employment and prices strengthened. The service sector surprisingly strengthened last month with the ISM Services Index increasing from 56.5 in February to 58.3 in March. New orders, employment and business activity all strengthened last month.

Non-U.S. Developed

- The eurozone economy maintained a strong rate of growth in March, easing only slightly from February's five-month high as looser COVID-19 restrictions continued to accommodate rising levels of business activity. The main impetus to the expansion was provided by the service sector, where growth edged slightly higher, as manufacturing output rose at a softer pace. New orders also increased at a solid rate in March, although new business from export markets deteriorated due to the war in Ukraine. It certainly seems likely however that the solid expansion seen in March will prove hard to sustain and there is clearly a greater risk of the economy stalling or contracting during the second quarter.

- We expect to see downward revisions to GDP growth estimates for the eurozone and other developed markets that are heavily reliant on energy/commodity imports. The eurozone and Japan are particularly vulnerable to higher energy and commodity costs. Prices were already high across the board prior to the Russia-Ukraine conflict and the sanctions will only further exacerbate the issue. The U.S. can increase its exports, but that is by no means an immediate solution.

- The ECB and BOJ will likely take a more patient approach with monetary policy given the ongoing conflict in the Ukraine. The ECB has previously signaled its intention to raise rate this year, but the eurozone economy will take a hit from energy shortages.

Emerging Markets

- China is clearly struggling with its zero tolerance COVID policy. The country is currently dealing with its largest outbreak since the start of the pandemic and that has led to harsh lockdowns/restrictions for Hong Kong, Shenzen and Shanghai. China is one of the few countries stimulating its struggling economy while the rest of the world has been tightening monetary policy. Additional stimulus measures may be necessary from the PBOC. A cut in the RRR is expected in April to help stabilize the world’s second largest economy.

- The Caixin/Markit Manufacturing PMI fell to its lowest level since February 2020. The reading fell from 50.4 in February to 48.1 in March. The deterioration in manufacturing conditions was broadly in line with the official PMI released on Thursday, which showed activity contracted at the quickest rate since October 2021. The private-sector Caixin survey focuses more on small firms in coastal regions compared with the official survey. In particular, the decline in new export orders in March accelerated.

- The Russian economy is set to shrink sharply this year while inflation skyrockets, as punitive international sanctions in response to its unprovoked invasion of Ukraine begin to bite. Russian manufacturing activity in March contracted at its sharpest rate since May 2020, in the early stages of the Covid-19 pandemic, as material shortages and delivery delays weighed heavily on factories.

- Capital Economics projects that Western sanctions are likely to push Russian GDP into a 12% contraction in 2022, while inflation is expected to exceed 23% Y/Y. Goldman Sachs has also forecast a 10% contraction, while the Institute for International Finance think tank has projected a more damaging 15% plunge in Russian GDP in 2022 and a further 3% in 2023.

- Thus far, Russia has avoided a default on its sovereign debt by making a recent bond payment and the stock market and ruble have rebounded sharply since reopening on March 24.

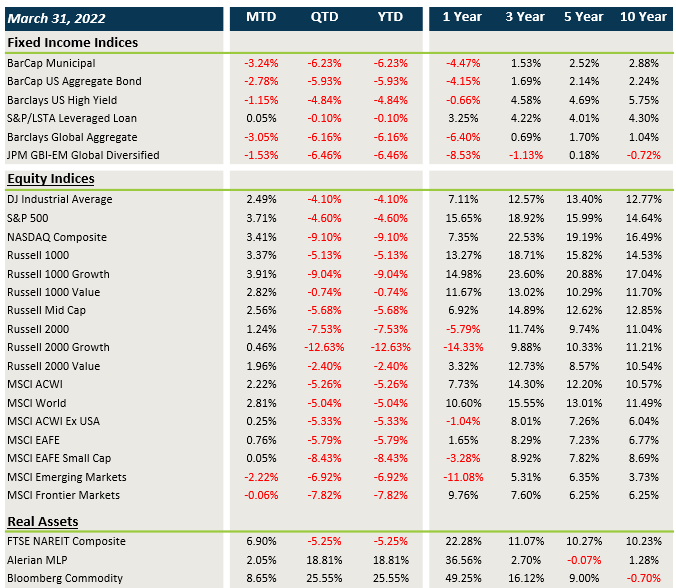

Market Performance (as of 3/31/22)

Fixed Income

- Treasury and sovereign bond yields across the globe continued their move higher in March, leading to losses in core fixed income and munis.

- Spread tightening was not enough to offset the negative move in rates.

- Floating rate loans held up their end of the bargain with positive performance.

U.S. Equities

- After struggling in January & February, U.S. equities finally rebounded in March.

- Growth beat value in large caps but lagged across small caps.

- Large cap tech/growth finally returned to favor last month.

Non-U.S. Equities

- Non-U.S. equities lagged U.S. counterparts in March. Europe outperformed Japan last month.

- The discrepancy between growth and value was muted outside the U.S. last month, but value leads the way YTD.

- EMs fell again in March as the Russia- Ukraine conflict weighed on risk assets.

- The stronger USD was a headwind for both EAFE and EM performance.

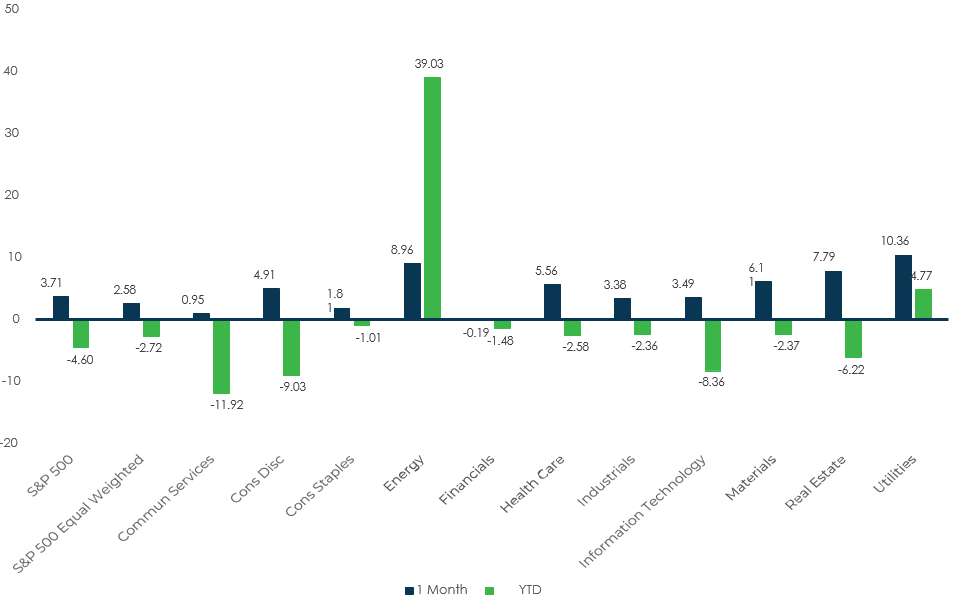

Sector Performance – S&P 500 (as of 3/31/22)

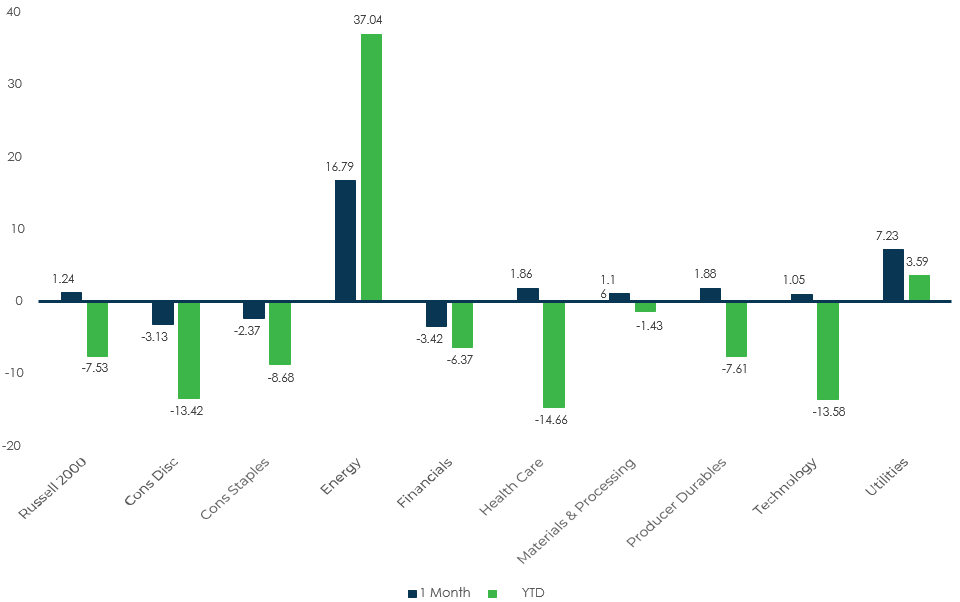

Sector Performance – Russell 2000 (as of 3/31/22)

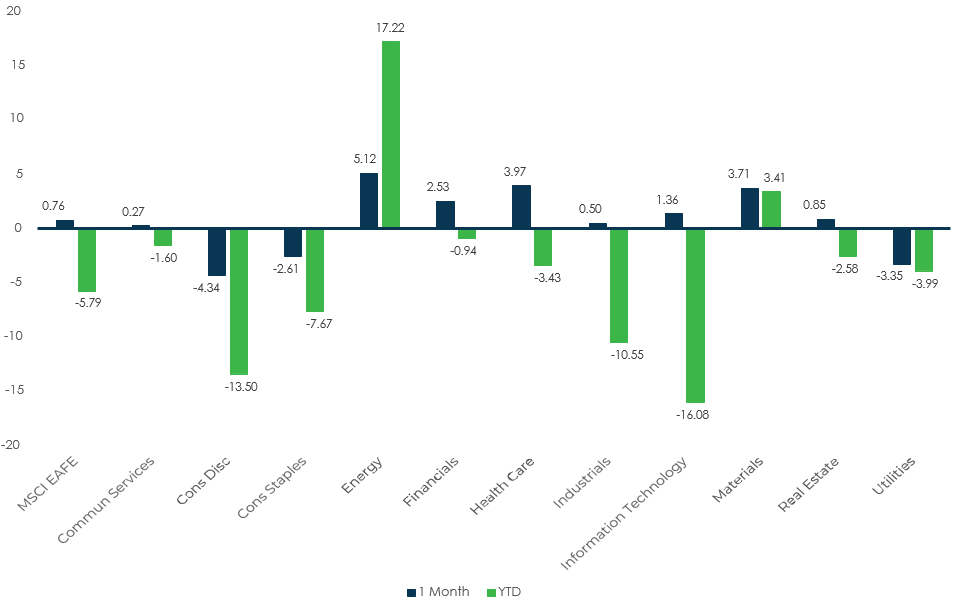

Sector Performance – MSCI EAFE (as of 3/31/22)

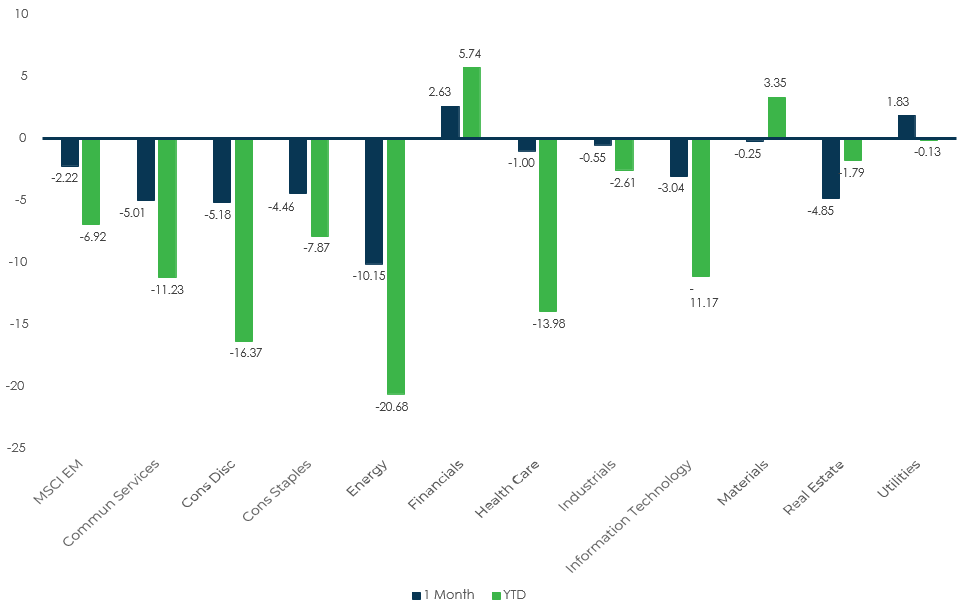

Sector Performance – MSCI EM (as of 3/31/22)