Market Flash Report | May 2022

Economic Highlights

United States

- The Federal Reserve delivered a widely anticipated 50 bps rate hike on May 4th, while also introducing its plan for quantitative tightening. The Fed Funds Rate increased from a range of 0.25%-0.50% to a new range of 0.75%-1.00%. There were no surprises with the Fed’s stated QT plan in which it will allow $30B of Treasuries to roll off for the first 3 months along with $17.5B in MBS. Those amounts will double after 3 months. It is important to note that the value of MBS maturing each month is in the $20B range, so the overall Fed balance sheet roll-off will likely fall short of its stated $95B/month target. While Chairman Powell took a 75 bps hike off the table, he did indicate that several 50 bps moves may be necessary along with some 25 bps ones. The Fed expects the Fed Funds Rate to end 2022 at a range of 2.50-2.75%. We continue to believe the Fed will take a more patient and methodical approach based on underlying data. Inflation will likely come down and the Fed will not need to raise rates as much as expected.

- Hiring surged again in April with 428,000 new jobs added to the U.S. economy. The unemployment rate held steady at 3.6% and the gains in employment were widespread, with leisure & hospitality up 78,000 jobs, manufacturing up 55,000 and retail up 29,000. The labor participation rate fell by 0.2% to 62.2%, led by the shrinking of the labor force by 363,000. Average hourly earnings increased by a slightly more modest 0.3% m/m last month, but upward revisions to the gains in earlier months mean that the annual rate of wage growth only edged down to 5.5%, from 5.6%. By any measure, labor market conditions are tight, which is driving wages higher. The solid April employment report illustrates that the Fed was right to ignore the misleading contraction in first quarter GDP, with the economy still on firm footing.

- The ISM Manufacturing Index rose from 55.4 in April to 56.1 in May, led by strength in new orders and production. The dip in the employment index to below 50 isn’t a great sign, as it suggests that the May employment report may show a slowdown in job growth. We expect to see some demand destruction in the coming months led by a slowdown in the global economy and the stronger U.S. dollar.

Non-U.S. Developed

- Eurozone economic growth remained robust in May despite headwinds associated with the Ukraine war, pandemic supply constraints and rising inflation. However, while the service sector continued to report strong growth from pent-up pandemic demand, the manufacturing sector saw only a modest expansion for the second month running amid falling order book inflows. Service sector activity remains robust and consistent with an economy growing at a 0.6% quarterly GDP growth rate.

- PMI data fell off a cliff in the U.K. last month as inflationary pressures and geopolitical uncertainty constrained consumer demand. The U.K. Composite PMI fell to a 15-month low of 51.8 in May from 58.2 in April. The services PMI hit a 15-month low while manufacturing hit a 16-month low. The U.K. data signal a severe slowing in the rate of economic growth in May, with forward-looking indicators hinting that worse is to come. Meanwhile, the inflation picture has worsened as the rate of increase of companies' costs hit yet another all-time high.

- Japan's economy shrank for the first time in two quarters in Q122 as COVID-19 curbs hit the service sector and surging commodity prices raised concerns about a protracted downturn. GDP fell at an annualized rate of 1%.

Emerging Markets

- China's retail and factory activity fell sharply in April as wide COVID-19 lockdowns confined workers and consumers to their homes and severely disrupted supply chains, casting a long shadow over the outlook for the world's second-largest economy. Retail sales in April shrank 11.1% Y/Y, the biggest contraction since March 2020, and factory production fell 2.9% Y/Y. Industrial production declined 14.1% in April, while fixed asset investment rose less than expected.

- While the worst is likely over with Shanghai’s reopening, a V-shaped economic rebound does not seem possible with the global economy starting to slow. External demand will put a damper on Chinese exports. Analysts say China's official 2022 growth target of around 5.5% is looking more difficult to achieve as officials maintain draconian zero-COVID policies. The economy grew 4.8% in Q1. Major investment banks have slashed their 2022 GDP growth forecasts for China to the 3-4% range.

- China’s official manufacturing PMI rose to 49.6 in May from 47.4 in April. This marked the third consecutive month in contraction territory. In line with the weakness in the factory sector, services remained soft. The official non-manufacturing PMI in May improved to 47.8 from 41.9 in April.

- India’s economic growth slowed to the lowest in a year in Q1 of 2022, hit by weakening consumer demand amid soaring prices that could make the central bank’s task of taming inflation without harming growth more difficult. GDP grew 4.1% year-on-year in Q1, in line with the 4% estimate and below the 5.4% growth in Q421 and the 8.4% rate in Q321.

Market Performance

Fixed Income

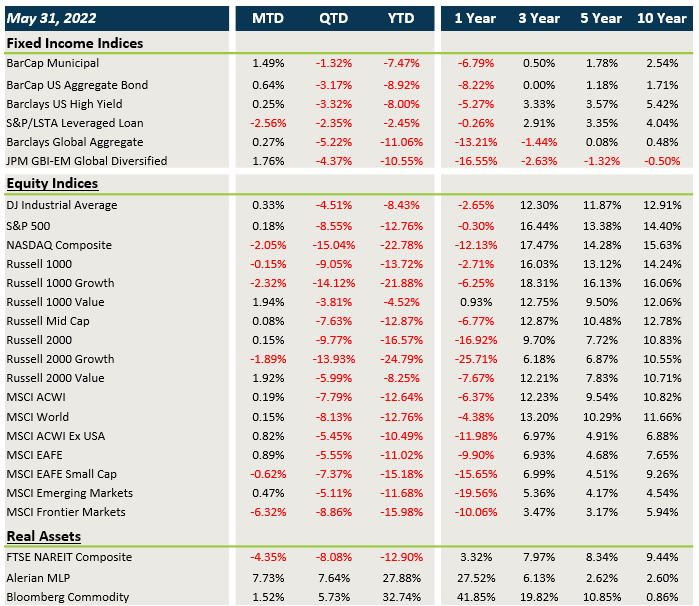

- Yields finally stabilized in May, leading to modest gains in core fixed income and most credit sectors. It has still been a very rough year overall.

- Spreads tightened some in IG, HY and EMD, but floating rate loans finally started to show some cracks.

- USD weakness provided a boost for non-U.S. assets in May.

U.S. Equities

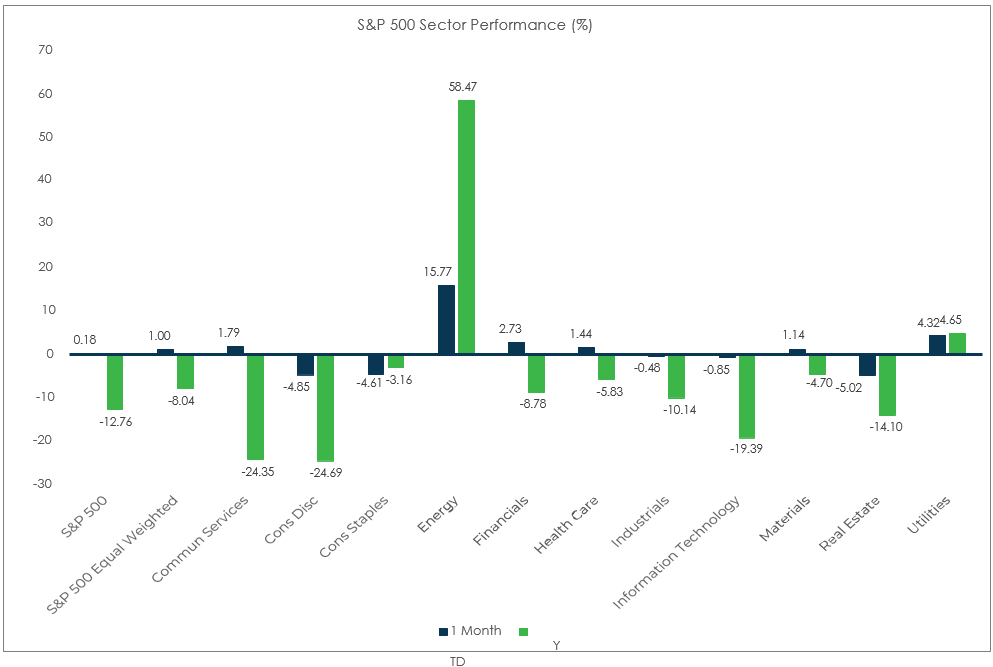

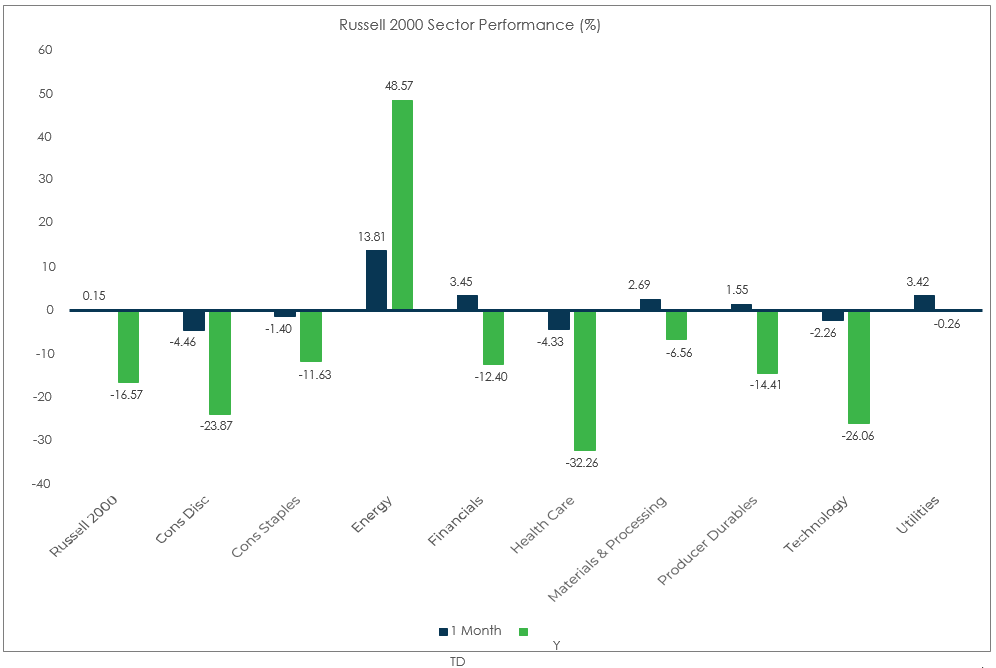

- U.S. equities rallied sharply to end May, but growth stocks still posted another month of negative returns.

- Value beat growth again in May and performance was similar between large caps and small caps.

- The Nasdaq has fallen nearly 23% YTD.

Non-U.S. Equities

- Non-U.S. equities outperformed their U.S. counterparts in May. EAFE markets in particular tend to be value focused so the outperformance is not surprising.

- Outside the U.S., value led growth and large caps beat small caps.

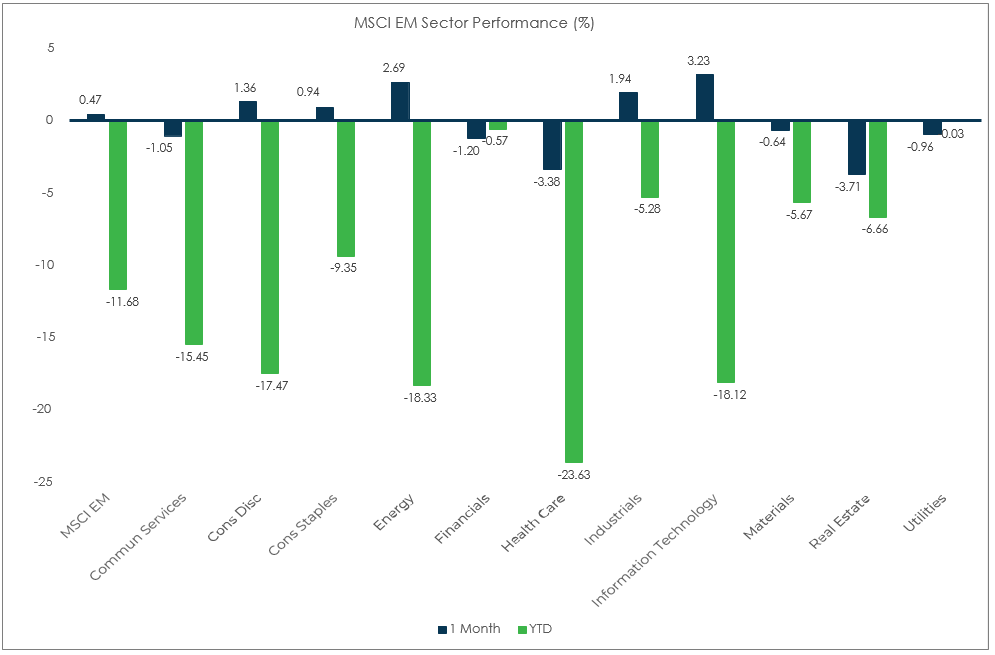

- EMs eked out a small gain in May led by LatAm and China.

- The weaker USD added nearly 100 bps to EAFE returns and approximately 60 bps to EM returns.

Sector Performance – S&P 500 (as of 5/31/22)

Sector Performance – Russell 2000 (as of 5/31/22)

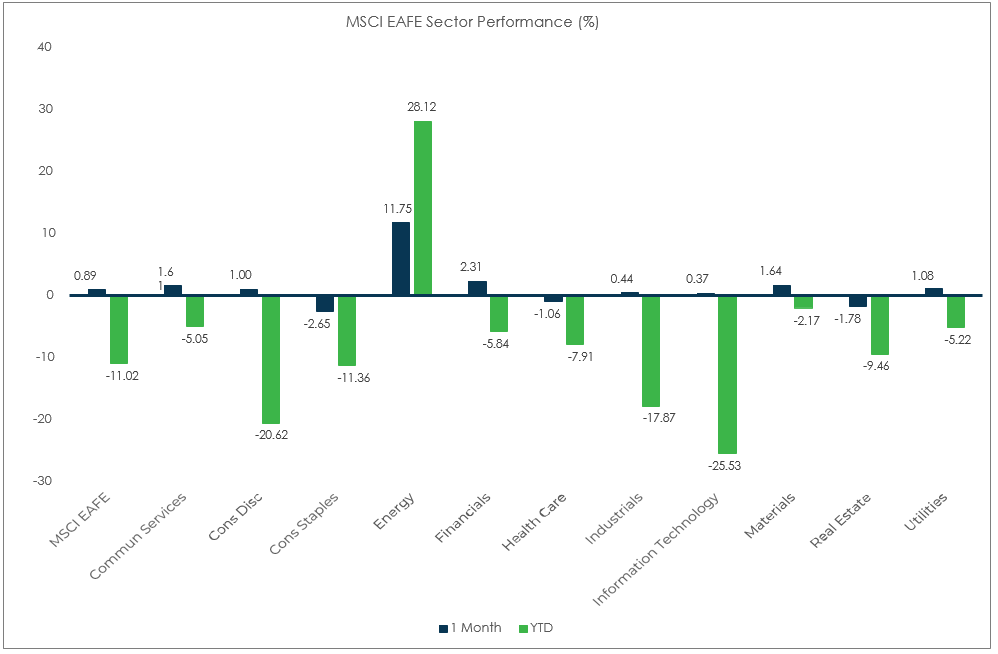

Sector Performance – MSCI EAFE (as of 5/31/22)

Sector Performance – MSCI EM (as of 5/31/22)