Market Flash Report | November 2023

Economic Highlights

United States

- Labor markets may finally be showing signs of cooling based on October’s below-expectations report and downward revisions to reports from August and September. U.S. employers added 150,000 new jobs to the economy last month, below the 170,000 estimate and trend for most of 2023. The unemployment rate of 3.9% jumped more than anticipated and the broader U6 unemployment rate increased to 7.2%. Average hourly earnings, a key measure for inflation, increased 0.2% for the month, less than the 0.3% forecast, while the 4.1% year-over-year gain was 0.1 percentage point above expectations. While the healthcare sector added 58,000 new jobs in October, the manufacturing sector shed 35,000 jobs, most coming from the UAW strike. The August and September reports were revised lower by a total of 101,000.

- The U.S. economy expanded an annualized 5.2% in Q3 2023, higher than 4.9% in the preliminary estimate. Consumer spending went up 3.6%, slightly less than 4% in the advance estimate, but remaining the biggest gain since Q4 2021.

- The Institute of Supply Management (ISM) Manufacturing PMI was flat in November at 46.7. New orders gained ground while production and employment weakened. All three major sub-components remain in contraction territory. Respondents cited a slowing global economy and elevated financing costs. The ISM Services PMI also declined in October, led by slower growth in production and employment. New orders firmed up and prices remained fairly flat. The November Services PMI report is due early next week.

- New orders for manufactured durable goods in the U.S. plummeted by 5.4% M/M in October 2023, reversing a 4.0% surge seen in September and significantly surpassing market expectations of a 3.1% drop. It was the second-largest fall in durable goods orders since April 2020, mainly driven by reduced demand for transportation equipment. Orders for nondefense capital goods excluding aircraft, a closely monitored proxy for business spending plans, decreased by 0.1% in October.

- Retail sales in the U.S. decreased by 0.1% M/M in October 2023, putting an end to a six-month streak of increases. On a yearly basis, retail trade growth slowed to 2.5% in October from an upwardly revised 4.1% in September.

Non-U.S. Developed

- Business activity in the eurozone continued to fall during November amid a further solid decline in new orders, according to flash PMI data. Both output and new business have now decreased in each of the past six months. While all of the PMIs in the eurozone remain well below the vaunted 50-level that separates contraction from expansion, the composite and services gauges hit two-month highs and the manufacturing PMI hit a six-month high.

- Annual inflation in the eurozone cooled to 2.4% in November from 2.9% in October. Core inflation also came in lower than expected, dropping to 3.6% from 4.2% in October.

- The unemployment rate in the eurozone remained at a record low of 6.5% in October, despite a contraction in Q3 GDP.

- Japan’s GDP shrank at its fastest quarterly pace in two years during Q3. GDP fell 2.1% Y/Y in Q3, down sharply from the 4.8% surge in Q2. GDP shrank 0.5% Q/Q in Q3.

Emerging Markets

- China’s official manufacturing PMI weakened to 49.4 in November from 49.5 in October. High-tech and equipment manufacturing both recorded expansions.

- China’s non-manufacturing PMI weakened to 50.2 in November from 50.6 in October. In the non-manufacturing sectors, weakness in the service industries outweighed strength in construction. In particular, the business activity index of industries such as real estate, leasing and business services stayed below 50, pointing to further contraction.

- Retail sales in China grew 7.6% Y/Y in October, industrial production rose 4.6% Y/Y, and fixed asset investment for the first 10 months of 2023 grew by 2.9%. Real estate investment declined 9.3% YTD.

- The Chinese property sector remains a weak spot for the economy, likely requiring further government support for stabilization and potential future growth.

- India’s GDP surged 7.6% in the latest quarter, fueled by the strong rebound in manufacturing and construction.

- Brazil's Finance Ministry lowered its forecast for the country's economic growth for 2023 and 2024. It now expects GDP growth in 2023 of 3.0%, slightly down from the 3.2% estimated in September. For 2024, the forecast was cut to 2.2% from 2.3% previously.

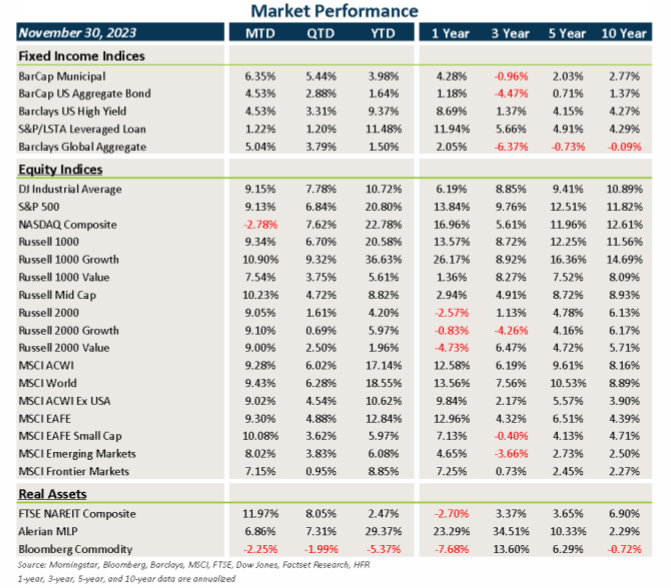

Market Performance (as of 11/30/23)

Fixed Income

- Treasury and other sovereign debt yields plunged across the globe, leading to strong gains for core fixed income, credit and municipal bonds.

- The Bloomberg Aggregate Bond Index (“Agg”) rose an astonishing 4.5% in November.

- Credit spreads tightened across the board last month with the risk-on sentiment.

- The weaker U.S. dollar also provided a nice boost to non-U.S. assets.

U.S. Equities

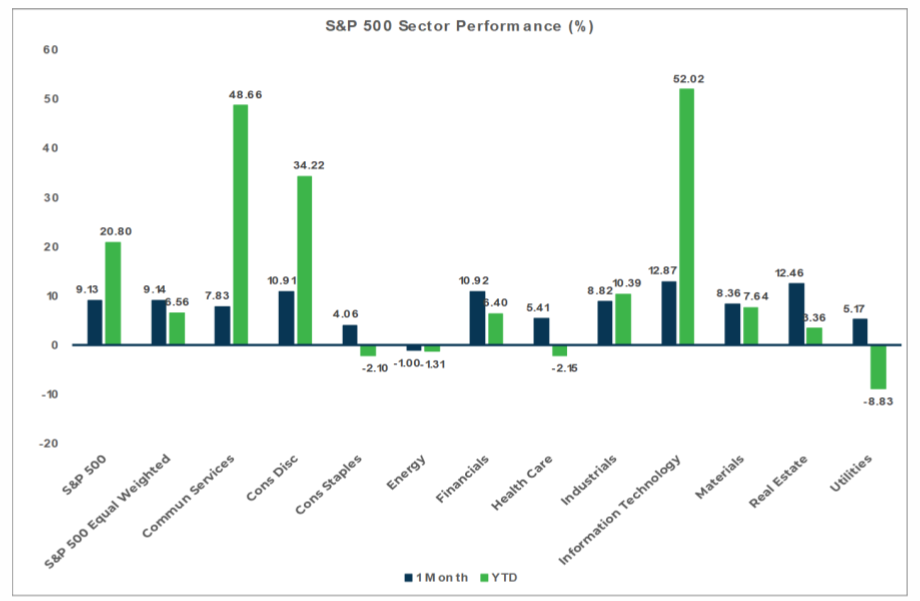

- U.S. equities surged higher in November, led by tech/growth stocks across all market capitalizations.

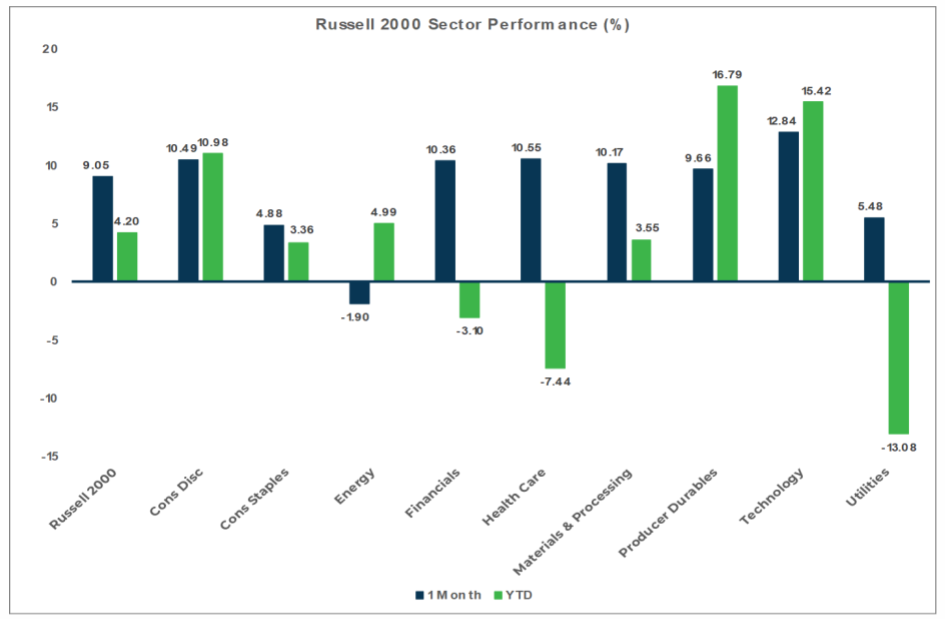

- Growth led value in large caps, but the difference in returns were flat within small caps.

- Small caps rebounded 9.1% last month, but continue to significantly underperform large caps in 2023.

Non-U.S. Equities

- Non-U.S. equities performed well in November, with strong gains from Europe and small caps.

- Similar to the U.S., growth led value within EAFE markets, but small caps outperformed large caps by about 80 bps.

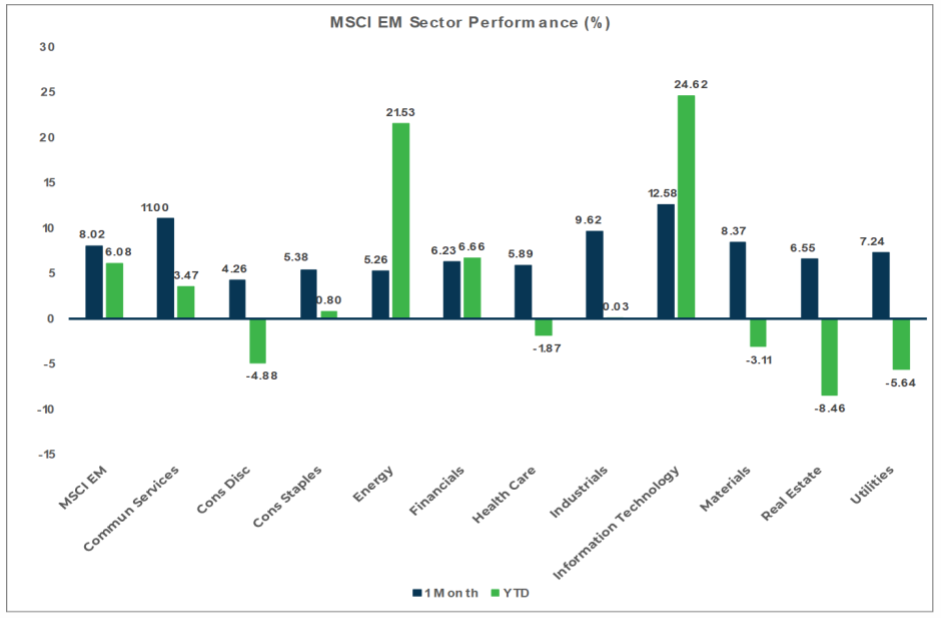

- Within emerging markets, Latin America and Eastern Europe drove the 8% return. Weakness in China caused EM Asia to underperform.

Sector Performance - S&P 500 (as of 11/30/23)

Sector Performance - Russell 2000 (as of 11/30/23)

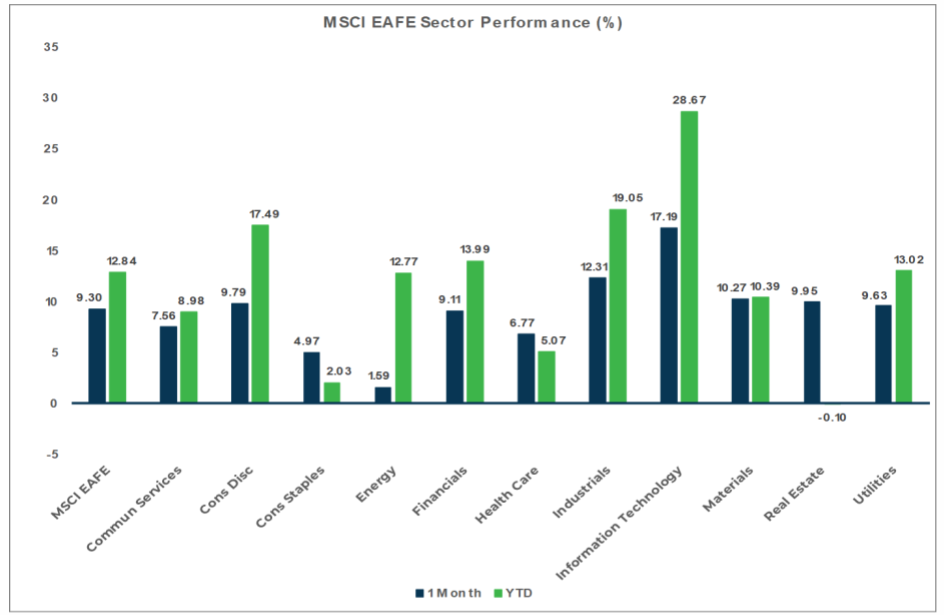

Sector Performance - MSCI EAFE (as of 11/30/23)

Sector Performance - MSCI EM (as of 11/30/23)