Market Flash Report | October 2022

Economic Highlights

United States

- After two consecutive quarters of contraction, the U.S. economy finally grew in Q3 2022. GDP increased at an annual rate of 2.6% during Q3, slightly ahead of economist expectations. The growth came in large part due to a narrowing trade deficit, which economists expected and consider to be a one-off occurrence that won’t be repeated in future quarters. GDP gains also came from increases in consumer spending, nonresidential fixed investment and government spending. Consumer spending as measured through personal consumption expenditures increased at just a 1.4% pace in the quarter, down from 2% in Q2. Gross private domestic investment fell 8.5%, continuing a trend after falling 14.1% in Q2. Residential investment, a gauge of homebuilding, tumbled 26.4% after falling 17.8% in Q2, reflecting a sharp slowdown in the real estate market. On the plus side, exports, which add to GDP, rose 14.4% while imports, which subtract, dropped 6.9%. Net exports of goods and services added 2.77% to the headline total, meaning GDP essentially would have been flat otherwise.

- The Personal Consumption Expenditures (“PCE”) price index, a key inflation measure for the Federal Reserve, increased 4.2%, down sharply from 7.3% in the prior quarter. Core prices, excluding food and energy, increased 4.5%, about in line with expectations. Consumer Price Index (“CPI”) inflation is still well above the Fed’s target level with the headline figures coming down in recent months while core inflation has accelerated. The Fed is expected to raise rates by another 75 bps at its November meeting and perhaps another 50-75 bps at its December meeting. This would put the Fed Funds Rate well into the mid-4% range and we believe a sufficient spot to pause and see how significant tightening is impacting consumers and the U.S. economy as a whole.

- September job growth was strong and largely in-line with expectations. U.S. employers added 263,000 new jobs to the economy and the unemployment rate fell to 3.5%. In the closely watched wage numbers, average hourly earnings rose 0.3% M/M, in line with estimates, and 5% Y/Y, an increase that is still well above the pre-pandemic norm but 0.1% below the forecast.

- September ISM reports showed broad based weakness in manufacturing and services. The ISM Manufacturing Index fell from 52.8 in August to 50.9 in September. The main drivers of the weakness were new orders, employment and supplier deliveries. The ISM Services PMI declined from 56.9 in August to 56.7 in September. Business activity, new orders and prices weakened while employment strengthened.

Non-U.S. Developed

- The eurozone economy slipped into a steeper downturn at the start of Q4 with the rate of decline hitting the fastest since April 2013 barring pandemic lockdowns. Manufacturing, and energy intensive sectors in particular, reported the steepest output loss, but services activity also continued to fall at an accelerating rate amid the ongoing cost-of-living crisis and broad-based economic uncertainty. Manufacturing led the downturn, with factory output declining for a fifth month running and slumping at a rate not seen prior to the pandemic since July 2012. Service sector output also fell, down for a third consecutive month, contracting to a degree not witnessed outside of pandemic lockdowns since May 2013.

- The eurozone economy grew 0.2% Q/Q in Q3 or 2.1% Y/Y. Major countries eked out slight growth, but the forecast looks bleak moving forward. The economic backdrop in Japan remains resilient with supportive fiscal and monetary stimulus boosting economic growth. While inflation is low in Japan, it has increased and is a concern like in most other global economies.

Emerging Markets

- The Chinese economy grew at a 3.9% annual rate in Q3, up from 0.4% growth in Q2. While the headline figure beat expectations, it is well below the government’s official target of 5.5%. Exports, a major driver of China’s growth, beat expectations with an increase of 5.7% in U.S.-dollar terms in September. However, imports in U.S.-dollar terms only rose by 0.3% in September from a year ago, missing the analyst forecast of 1% growth. Finally, retail sales rose 2.5% Y/Y in September, below the forecast of 3.3% growth. Most of the growth came from auto sales, which surged 14.2%.

- Industrial production rose by 6.3% Y/Y in September, well above the 4.5% increase expected by economists. Automobile manufacturing surged by nearly 24%, while the country produced more than twice the number of new energy vehicles compared with a year ago. Fixed asset investment has missed expectations through the first three quarters of 2022, but real estate investment and infrastructure spending have exceeded projections.

- China’s factory activity fell in October due to frequent COVID-19 outbreaks. The official manufacturing PMI dropped from 50.1 in September to 49.2 in October. Sub-indicators on factory employment, production, new orders and supplier delivery time all showed contraction in October compared to September. Activity in the service sector also weakened last month with the official services PMI falling to 48.7 (from 50.6), the first contraction since May.

- China’s economy looks particularly weak right now with declines in manufacturing and services. Consumer spending has been challenged and that looks set to continue with rising COVID-19 cases and nearly 210 million people back in lockdown early in November. Until the country changes its zero tolerance COVID-19 policy, the world’s growth engine may not fully recover.

- Luiz Inácio “Lula” da Silva won the hotly contested Brazilian presidential race over rival and incumbent president Jair Bolsonaro who has yet to concede defeat. The Brazilian real has been one of the few currencies in the world to have gained ground against the U.S. dollar this year, up roughly 5%. The main reason is the assumption that the country's central bank is further ahead of the Fed in its monetary tightening cycle. Base interest rates in the country have been running at 13.75%, and inflation has, in fact, subsided over the previous three months. Unemployment has also been trending down, and GDP estimates revised upward, a sign that the overall economy remains resilient in the face of the current global crisis.

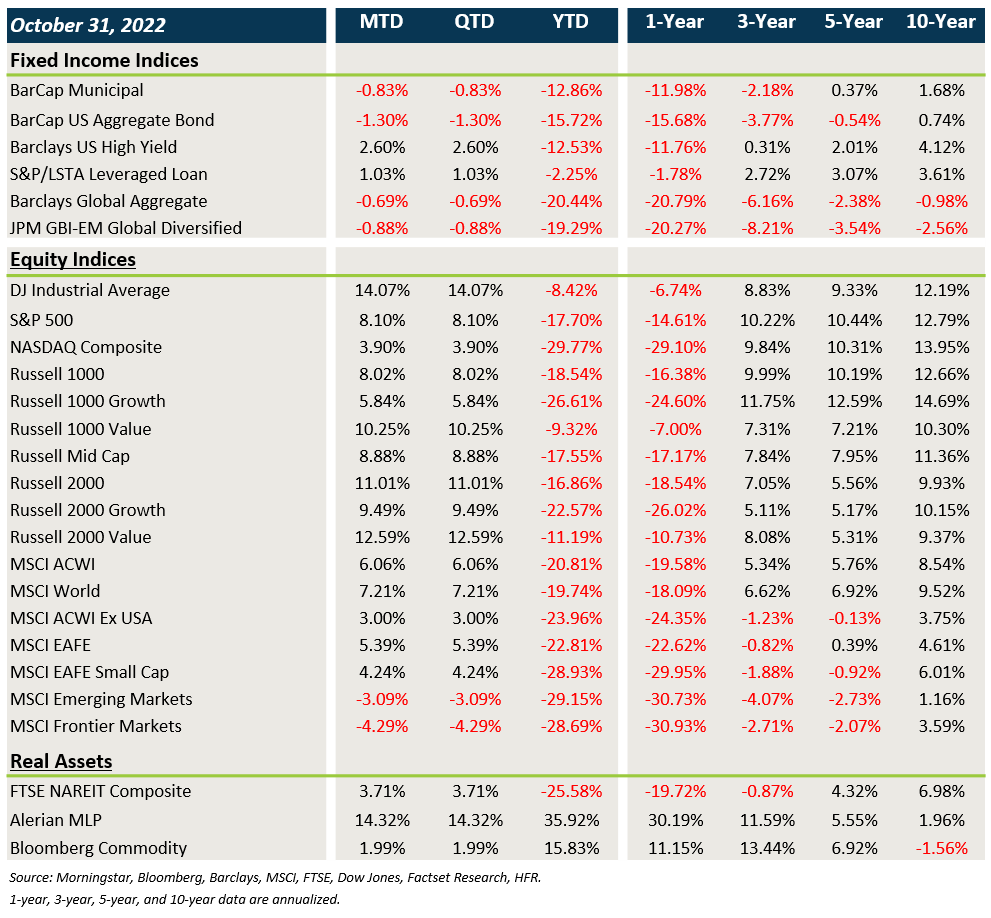

Market Performance (as of 10/31/22)

Fixed Income

- Treasuries and other sovereign debt yields continued to march higher in October, leading to losses in core fixed income and munis.

- Credit spreads generally tightened during October’s risk-on rally. High yield led the way, followed by floating rate loans.

- The impact from currency was largely flat within developed markets and a headwind for EMD.

U.S. Equities

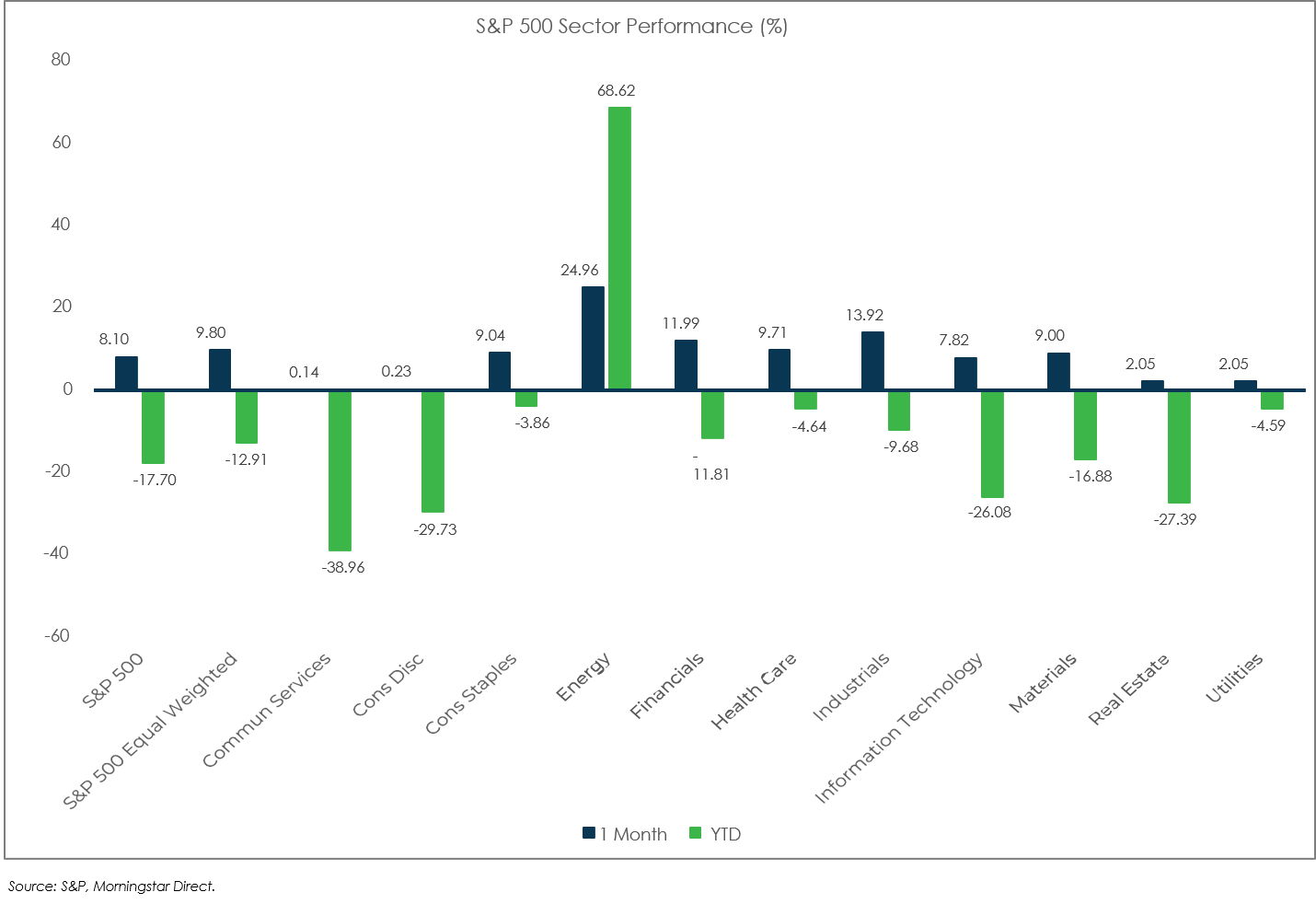

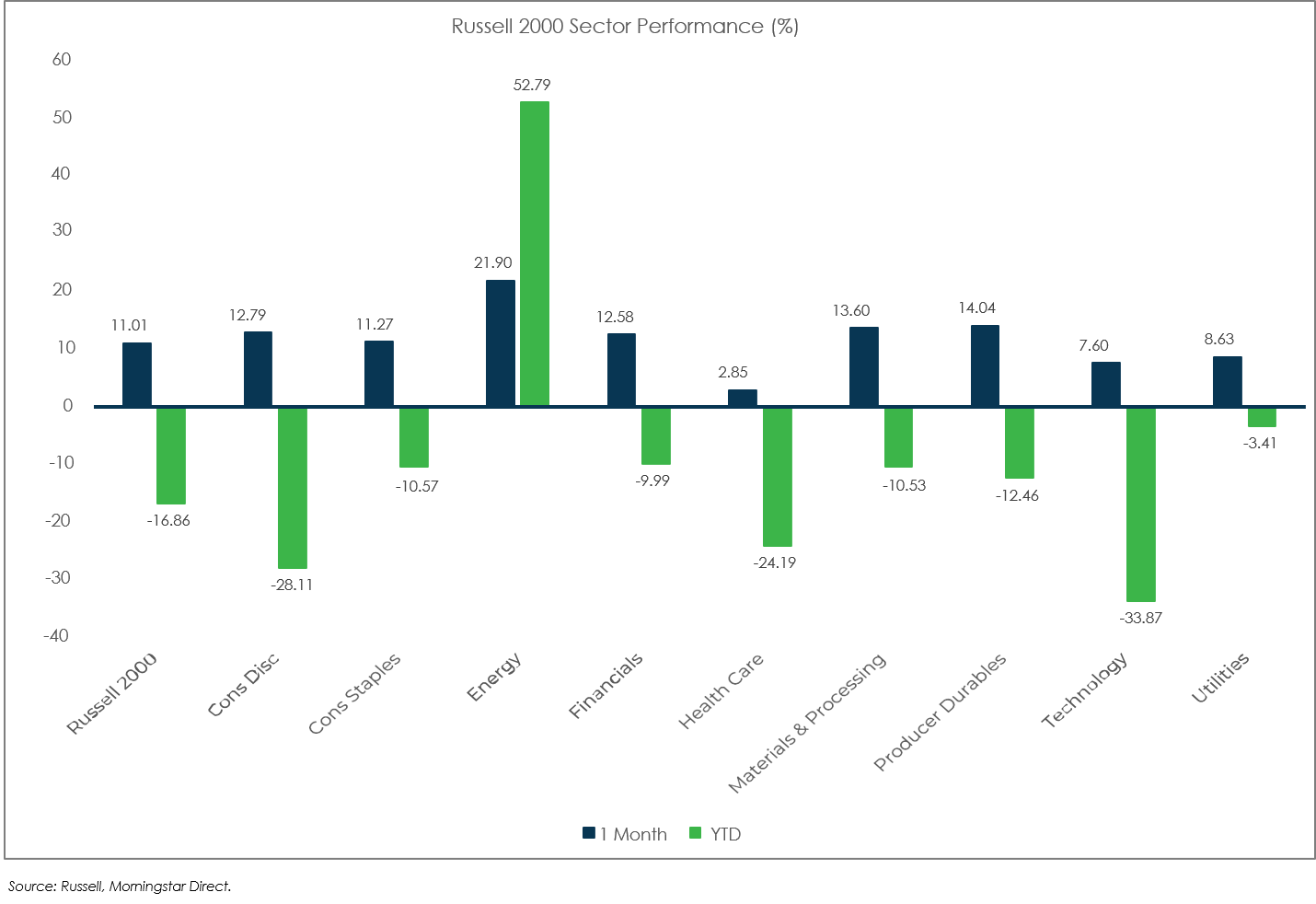

- Equities and other risk assets rallied sharply in October, led by the U.S.

- Value beat growth across large caps and small caps, and small caps out-performed large caps.

- The tech-heavy Nasdaq continues to trail other indices YTD, primarily as some of the heavyweight companies provided weak Q4 guidance.

Non-U.S. Equities

- Non-U.S. developed equities posted solid gains in both local and USD terms last month.

- Value out-performed growth in October and unlike the U.S., small caps trailed large caps.

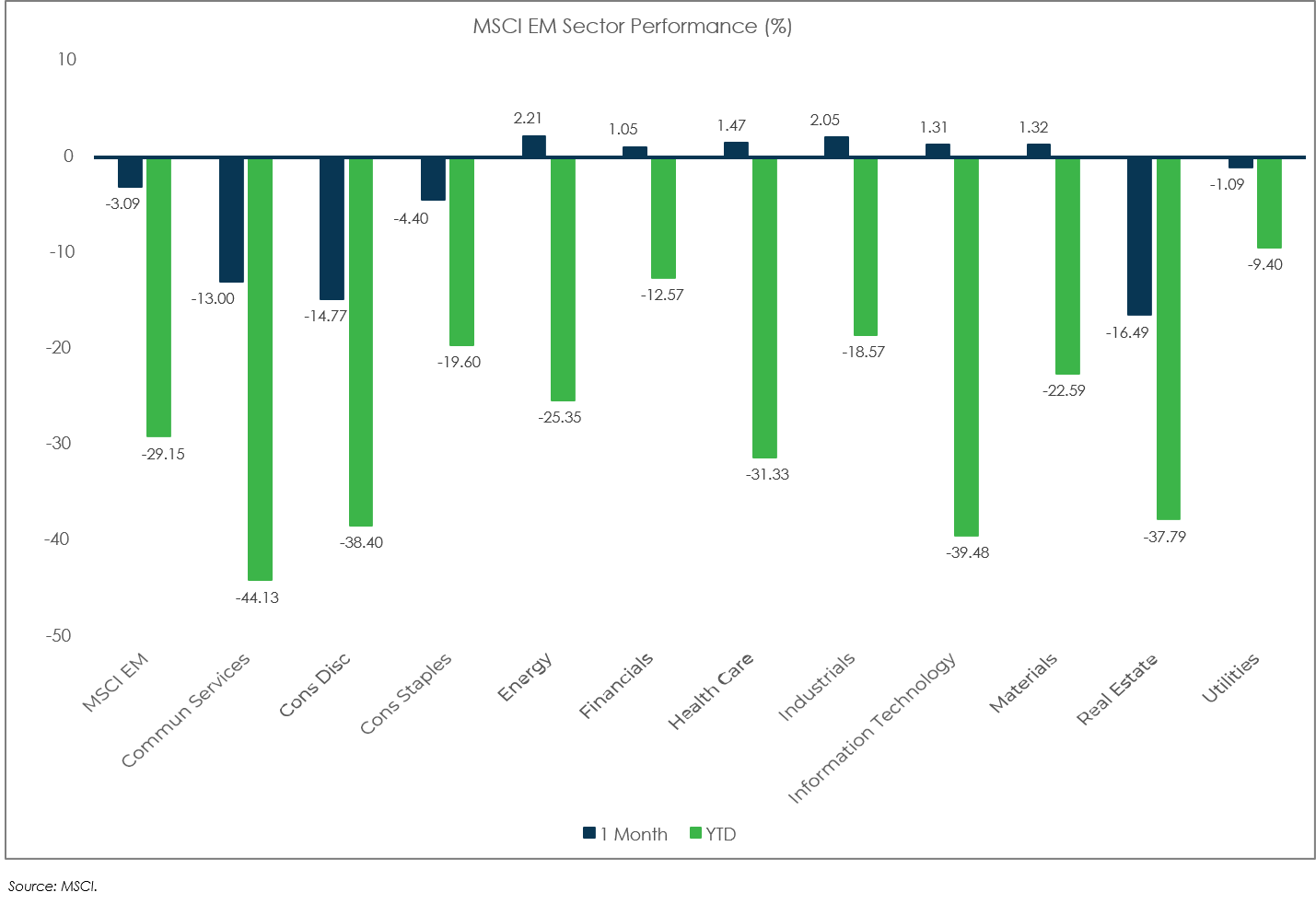

- EM equities were the real laggard in October, led by substantial weakness in China (-16.8%). Local returns also fared better than USD returns.

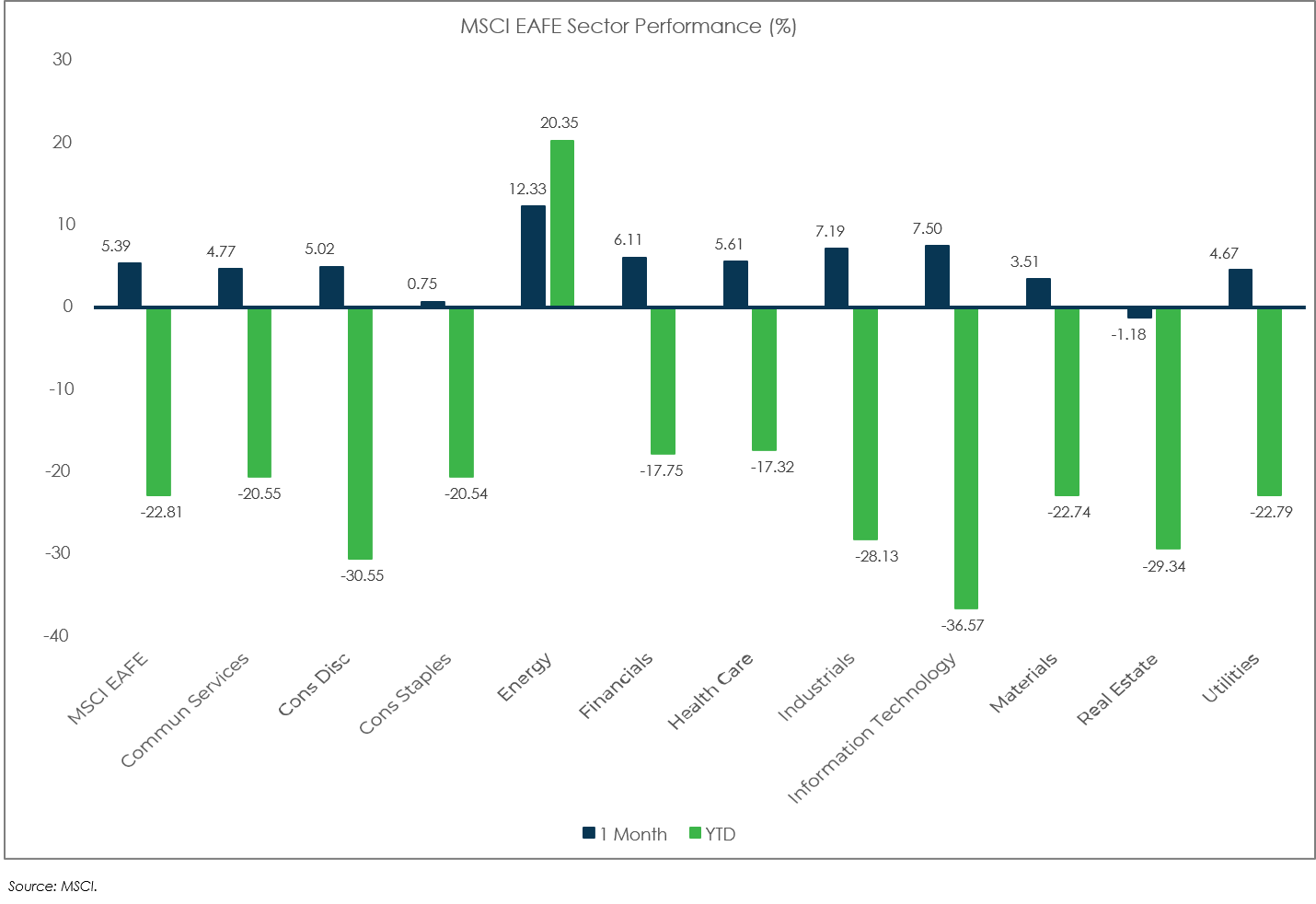

Sector Performance

S&P 500 (as of October 31, 2022)

Russell 2000 (as of October 31, 2022)

MSCI EAFE (as of October 31, 2022)

MSCI EM (as of October 31, 2022)