Market Flash Report | September 2022

Economic Highlights

United States

- Mixed signals for the U.S. economy continued with the release of the August employment report. U.S. employers added 315,000 new jobs to the economy, in line with economist expectations. The prior two months’ reports were revised lower by a total of 107,000 jobs, and the August reading was down sharply from July. The unemployment rate rose to 3.7%, largely due to an increase in the labor participation rate (62.4%). A broader measure of unemployment that includes discouraged workers and those holding part-time jobs for economic reasons climbed to 7% from 6.7%. Wages continued to rise, though slightly less than expected. Average hourly earnings increased 0.3% for the month and 5.2% from a year ago.

- The Federal Reserve raised rates by another 75 bps at its September meeting, bringing the target range to 3-3.25%. With rates already moving 3% higher this year, the Fed sees rates at 4.4% by year-end and the terminal rate at 4.6% in 2023.

- The PCE index came in with a Y/Y rise of 6.2% in August, down slightly from 6.4% in July. The index rose 0.3% M/M. The core PCE index, which excludes volatile food and energy prices, showed a 4.9% rise Y/Y and a gain of 0.6% M/M in August, coming in hotter than forecasts on both counts. Headline CPI rose 8.3% Y/Y based on the August report with Core CPI increasing 6.3%. Both PCE and CPI inflation remain well above the Fed’s 2% target.

- U.S. manufacturing flatlined in August with no change in the ISM Manufacturing Index. The headline reading of 52.8 for August was unchanged from July. Employment and new orders showed strength last month while production softened. Prices also showed some signs of easing in August. The ISM Services PMI increased slightly in August to 56.9 from 56.7 in July. Business activity, employment and new orders all firmed in August.

- The headline retail sales figure for August showed a surprising mild increase of 0.3% after falling a downwardly revised 0.4% in July. While the headline number was better than expected, “core” retail sales, which removes some volatile categories, actually fell 0.3%. Auto sales jumped 2.8%, restaurant sales rose 1.1% and gas station sales sank 4.2%. Similar to the report on retail sales, durable good orders were flat in July, trailing market expectations. This marked the first month in five in which the headline durable goods number didn't advance. Orders for nondefense capital goods excluding aircraft, a proxy for investment in equipment, increased 0.4%, easing from a 0.9% rise in June.

Non-U.S. Developed

- The eurozone economic downturn deepened in September, with business activity contracting for the third consecutive month. Although only modest, the rate of decline accelerated to a pace which, barring pandemic lockdowns, was the steepest since 2013. Forward-looking indicators, such as new orders, backlogs of work and future output expectations point to the decline gathering further momentum in coming months. Softening was seen in both manufacturing and services, with demand falling at faster rates in each sector as a result of the rising cost of living and growing gloom around future prospects.

- Inflation in Japan is the lowest among major economies, with the consumer price index rising 2.8% in August, compared with 8.3% in the U.S. and 9.1% in the EU. Abenomics may be the cause, but wages are also not growing adding pressure for consumers.

Emerging Markets

- Although the official manufacturing PMI unexpectedly strengthened in September, most other economic indicators in China showed weakness. China’s official manufacturing PMI surprisingly grew in September to 50.1, up from 49.4 in the prior month and well ahead of subdued expectations. Meanwhile, the Caixin/S&P Global manufacturing PMI, a private survey of smaller factory activity, reported a contraction with a reading of 48.1. Subdued demand conditions and lower production requirements led firms to cut back on their purchasing activity in September, with the rate of decline the quickest in four months. COVID-19 lockdowns were also cited as an explanation for decreased demand.

- China’s official services PMI also declined to 50.6 in September from 52.6 in August. New export orders showed a lot of weakness in last month’s report.

- Brazil’s polarizing presidential race will go to a second round runoff after no candidate achieved a majority of more than 50% of the ballot. Results showed left-wing candidate and former president Luiz Inácio Lula da Silva held a slight lead over right-wing incumbent President Jair Bolsonaro, but not enough to cross the threshold to victory. The runoff will be held on October 30. Brazilian assets like the real and equities outperformed as a result of the closer-than-expected election result.

- Investors are betting the leftist former President Luiz Inacio Lula da Silva’s narrow lead may pressure him to pivot toward the center before the second-round vote and prioritize market-friendly policies. Meanwhile, the incumbent Jair Bolsonaro’s better- than-expected showing suggests he still has a chance to win in the second round, potentially providing continuity for investors.

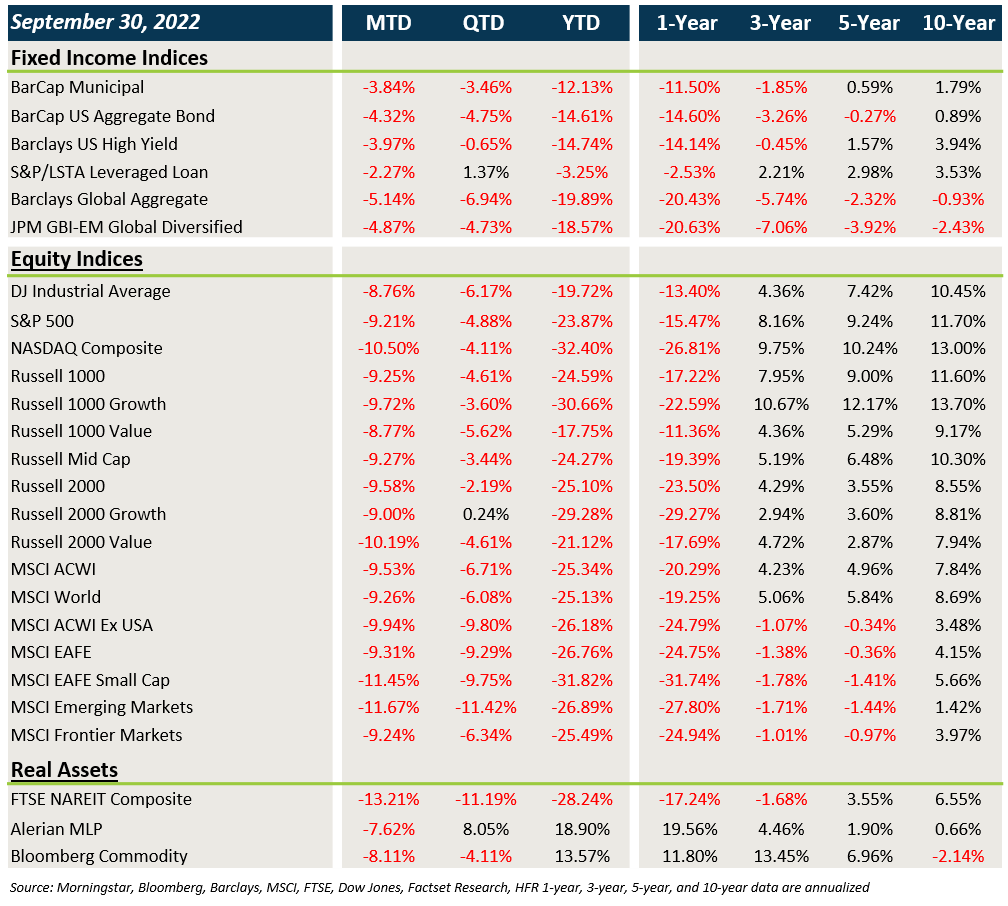

Market Performance (as of 9/30/22)

Fixed Income

- Treasuries and other sovereign debt yields continued their surge higher in September, leading to sharp losses in core fixed income and munis.

- Credit spreads widened last month on the growing risk off trade. Leveraged loans provided some relative outperformance.

- Bonds outside the U.S. were hit particularly hard by higher yields and the strong U.S. dollar.

U.S. Equities

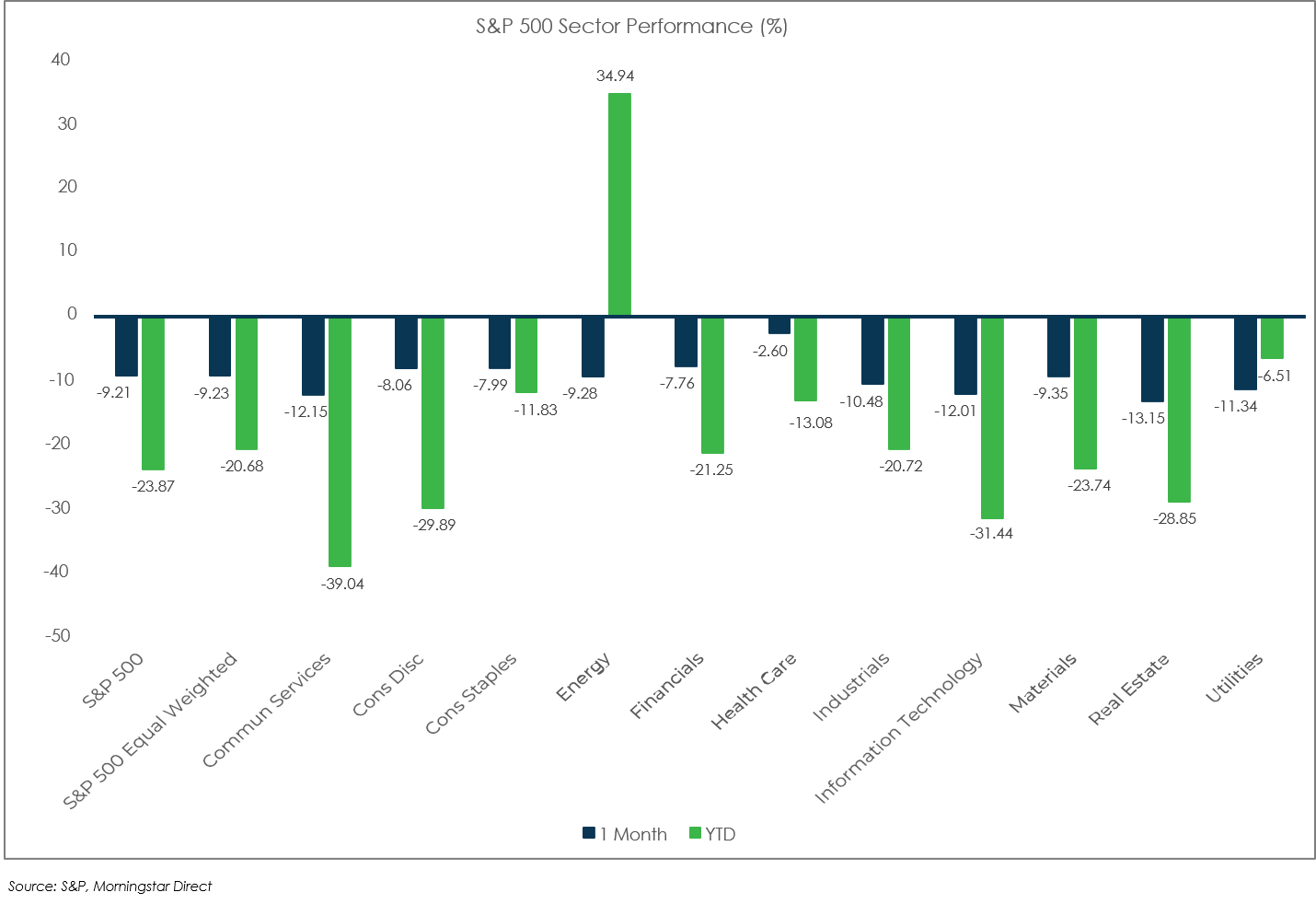

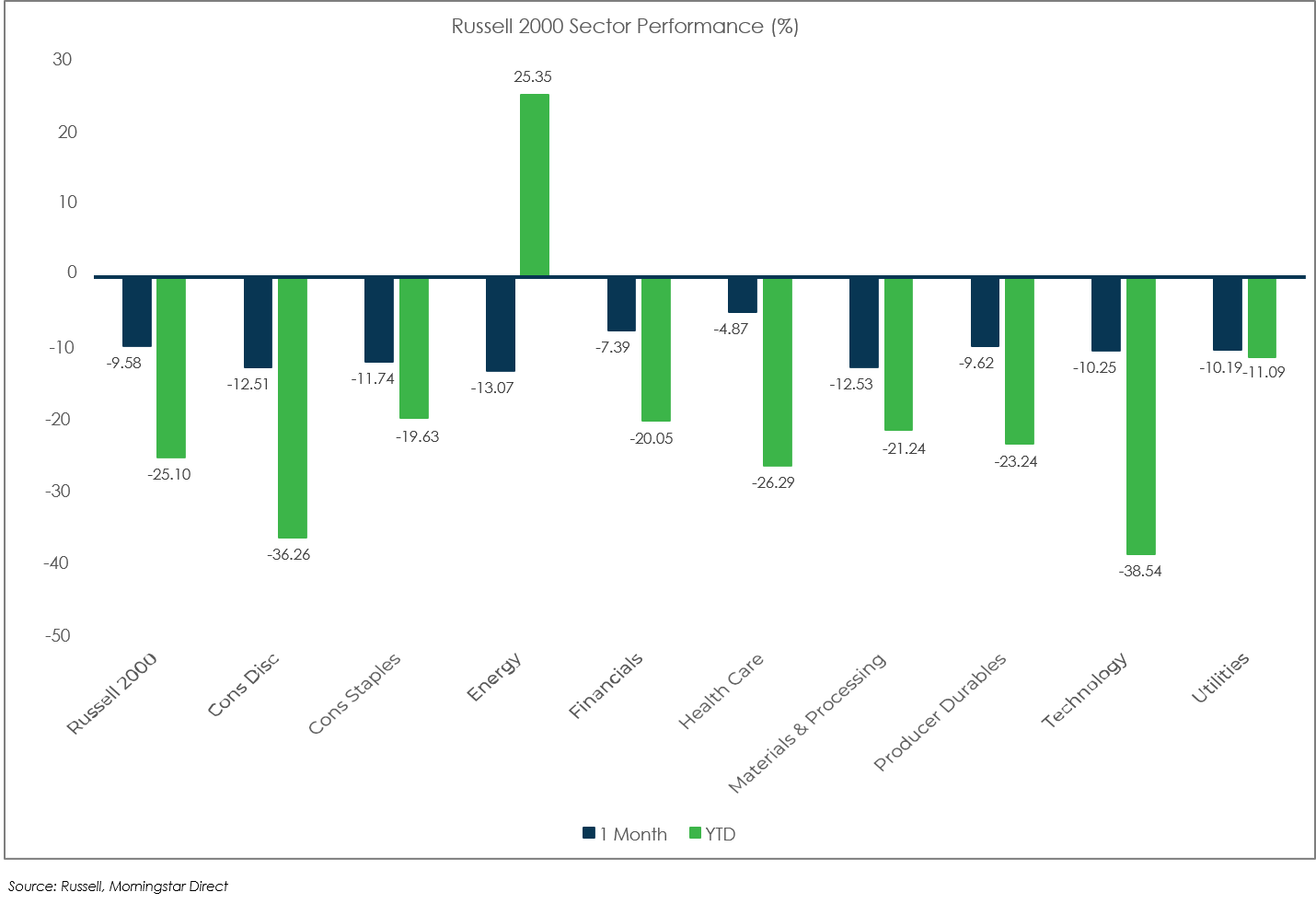

- September was a rough month for risk assets like U.S. equities. The S&P 500 fell 9.2% while the Russell 2000 dropped 9.6%.

- Large cap tech and growth stocks were the hardest hit in September.

- Value led growth in large caps last month, but growth beat value across small caps.

Non-U.S. Equities

- Non-U.S. developed market equities outperformed the U.S. in local terms, but lagged when factoring in the strong U.S. dollar.

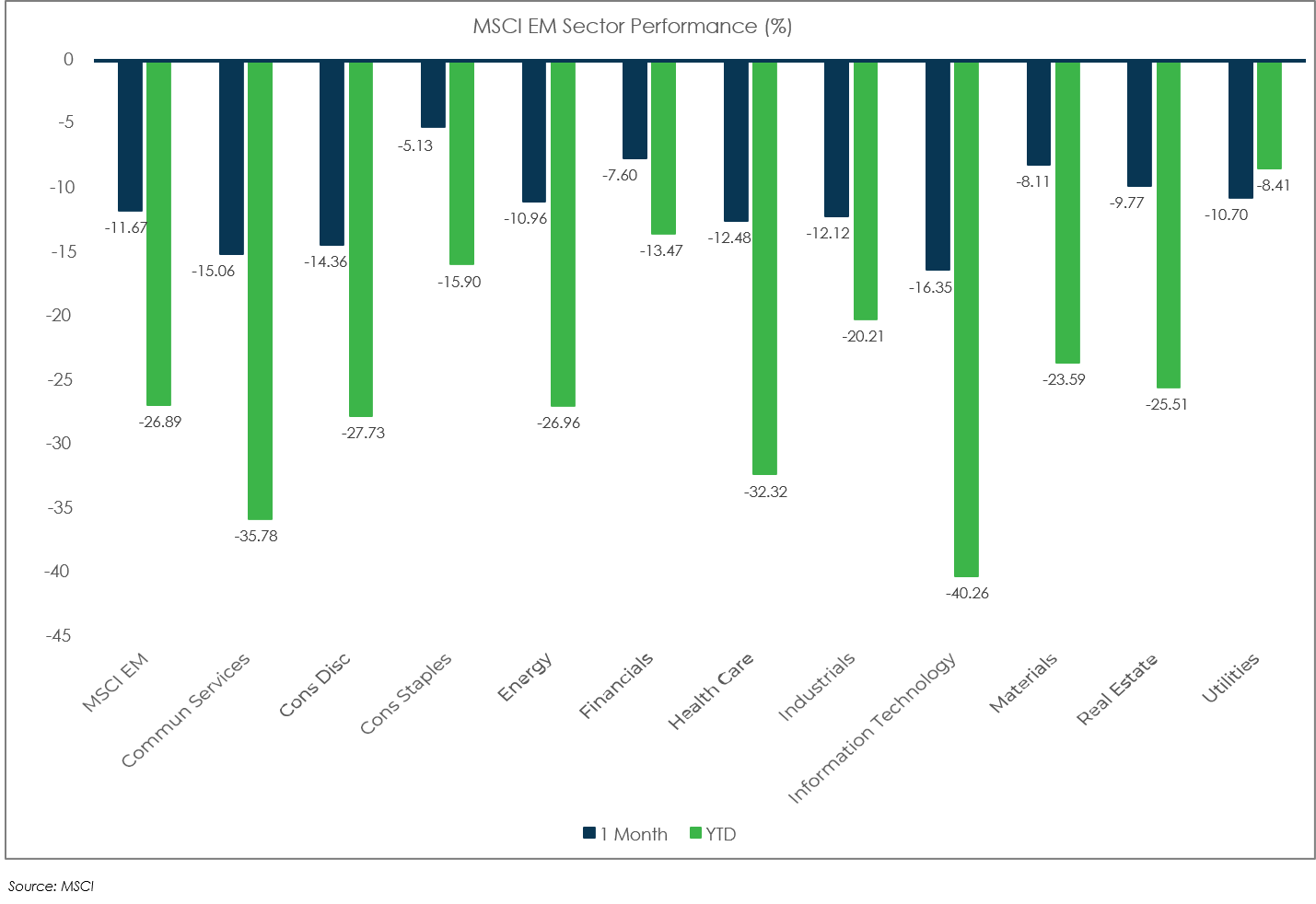

- Value beat growth within the EAFE and EM indices.

- Small caps beat large caps in EMs, but lagged in developed markets.

Sector Performance

S&P 500 (as of September 30, 2022)

Russell 2000 (as of September 30, 2022)

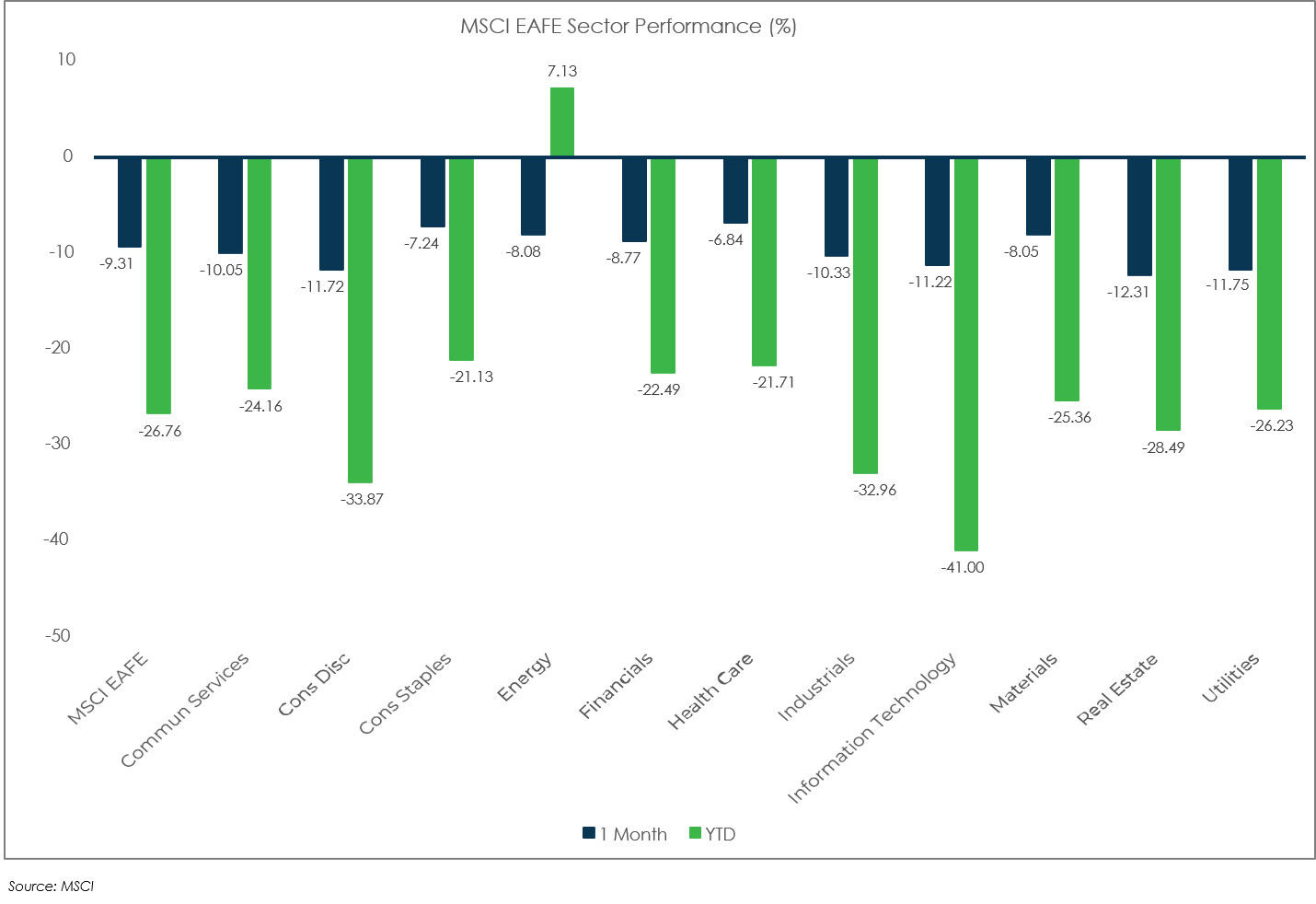

MSCI EAFE (as of September 30, 2022)

MSCI EM (as of September 30, 2022)