December 2025 Market Update

Economic Highlights

United States

- U.S. employers added more jobs than expected in November after the labor market shed 105,000 jobs in October. Job growth totaled 64,000 in November, ahead of the 45,000 estimate, but the unemployment rate rose a bit more than anticipated to 4.6%. A more encompassing measure that includes discouraged workers and those holding part-time jobs for economic reasons swelled to 8.7%, its peak going back to August 2021. The October slump came from a steep fall in government employment, as deferred layoffs instituted earlier last year took effect. Average hourly earnings rose just 0.1% M/M or 3.5% Y/Y, the smallest annual gain since May 2021.

- U.S. GDP grew more than expected in Q3 with growth coming in at 4.3% versus the 3.2% estimate. Consumer spending expanded by 3.5% in Q3 after rising 2.5% in Q2. Increases in exports and government spending also boosted growth while a smaller dip in private fixed investment helped as well.

- The Federal Reserve cut rates again at its December meeting but signaled to investors that there are no guaranteed future rate cuts. The central bank cut its benchmark federal funds rate by another quarter of a percentage point, bringing it to a range of 3.50%-3.75%. This cut marked the third reduction in 2025 and means the federal funds rate has now come down by a total of 1.75 percentage points since it peaked in 2023-2024.

- The Federal Open Market Committee also raised its median gross domestic product forecasts for 2026 by 0.5% to 2.3% while keeping its unemployment projection unchanged at 4.4% and with inflation moving lower by 0.2% to 2.4%. The fed funds futures are pricing in two to three rate cuts in 2026, although we believe action will be data dependent. One major surprise was the announcement of reserve management purchases starting almost immediately at a pace of $40B per month.

Non-U.S. Developed

- After strengthening for most of 2025, eurozone manufacturing weakened in December based on the Hamburg Commercial Bank Manufacturing PMI. The headline reading of 48.8 was down from 49.6 in November, a nine-month low. Demand for euro-area goods also saw fresh signs of weakness as new orders fell at the quickest pace in almost a year. Manufacturing performances worsened in a number of key euro-area economies during December. The most notable was Germany, which posted its steepest deterioration in sector conditions since February of last year and recorded the weakest performance of the eight monitored eurozone nations.

- Eurozone GDP growth for Q3 of 2025 was revised slightly higher to 0.3%, up from the preliminary estimate of 0.2%. The upgrade was driven by a rebound in fixed investment, which rose 0.9% compared with a 1.7% decline in Q2, and stronger government spending, up 0.7% versus 0.4% in Q2. Inventory changes contributed to Q3 GDP growth, while net exports subtracted 0.2%. Spain and France led the expansion in Q3, but German growth remained stagnant.

- Japan’s economy contracted in Q3 due largely to weak consumption growth, and economists believe similar challenges could be ahead in 2026. Consumers are feeling the bite from higher inflation, and the broader economy is suffering a bit from U.S. tariffs and geopolitical issues. Other items to watch include yen weakness, rising Japanese Government Bond yields and corporate earnings, which are expected to remain solid.

Emerging Markets

- China’s factory activity returned to expansionary territory in December, beating market expectations to end an eight-month contraction. Analysts say it may be premature to view the rebound as a sign of sustained stabilization. The manufacturing PMI stood at 50.1 in December, up from 49.2 the previous month, with both production and demand rebounding. New orders expanded for the first time in months, but new export orders continued to contract. Private-sector data showed a similar trend. A separate PMI from independent research firm RatingDog showed manufacturing activity rising to 50.1 from 49.9, beating expectations of 49.8.

- China’s non-manufacturing PMI, which measures activity in the construction and services sectors, rose to 50.2 in December from 49.5 last month. Warmer weather in parts of China likely provided a lift to the construction sector in December.

- Momentum elsewhere in the economy has cooled towards the year-end, with consumption growth slowing further and fixed-asset investment, a traditional growth engine, slumping in November. Retail sales rose 1.3% Y/Y in November, slowing from 2.9% in the prior month. Industrial production climbed 4.8% Y/Y in November, missing expectations for a 5% jump and marking its weakest growth since August 2024. Investment in fixed assets, which includes property, contracted more than expected in the YTD period ending in November.

- China’s trade surplus surged to a record $1.1 trillion in November, breaking its full-year record of $992.2 billion in 2024, in just 11 months, drawing widespread concerns over its reliance on foreign demand and depreciation of its currency to keep exports competitive. A rebalancing of the Chinese economy towards more consumption is necessary to end the significant reliance on external demand and investment for economic growth.

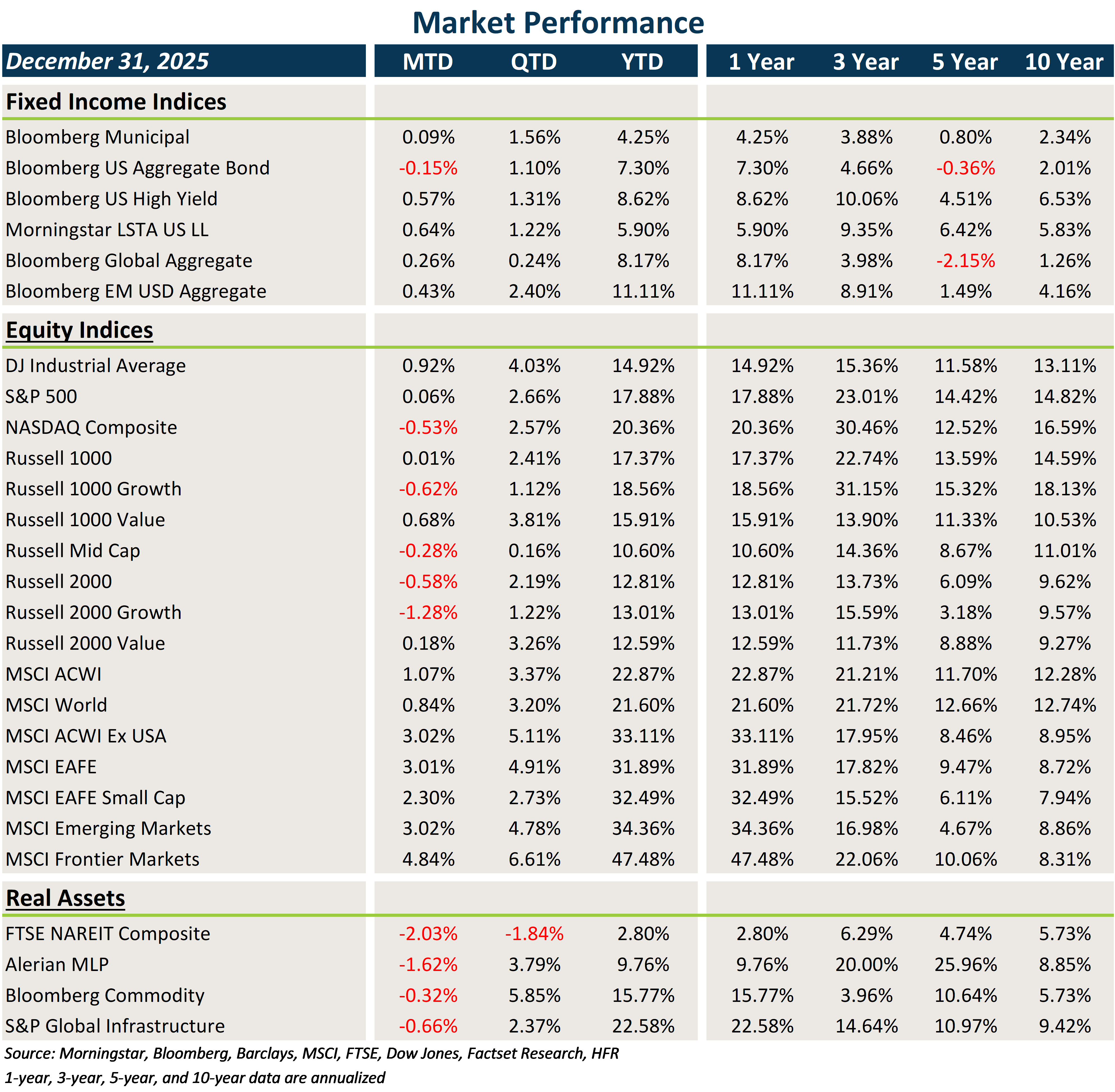

Market Performance (as of 12/31/25)

Fixed Income

- Fixed income across the globe benefited from spread tightening along with higher starting yields to end the year.

- While the 10-year Treasury yield was fairly rangebound in December, it ended the month slightly higher, and this was negative for core fixed income. Municipal bonds performed slightly better due to favorable technicals.

- Credit posted solid returns, largely driven by coupon clipping.

U.S. Equities

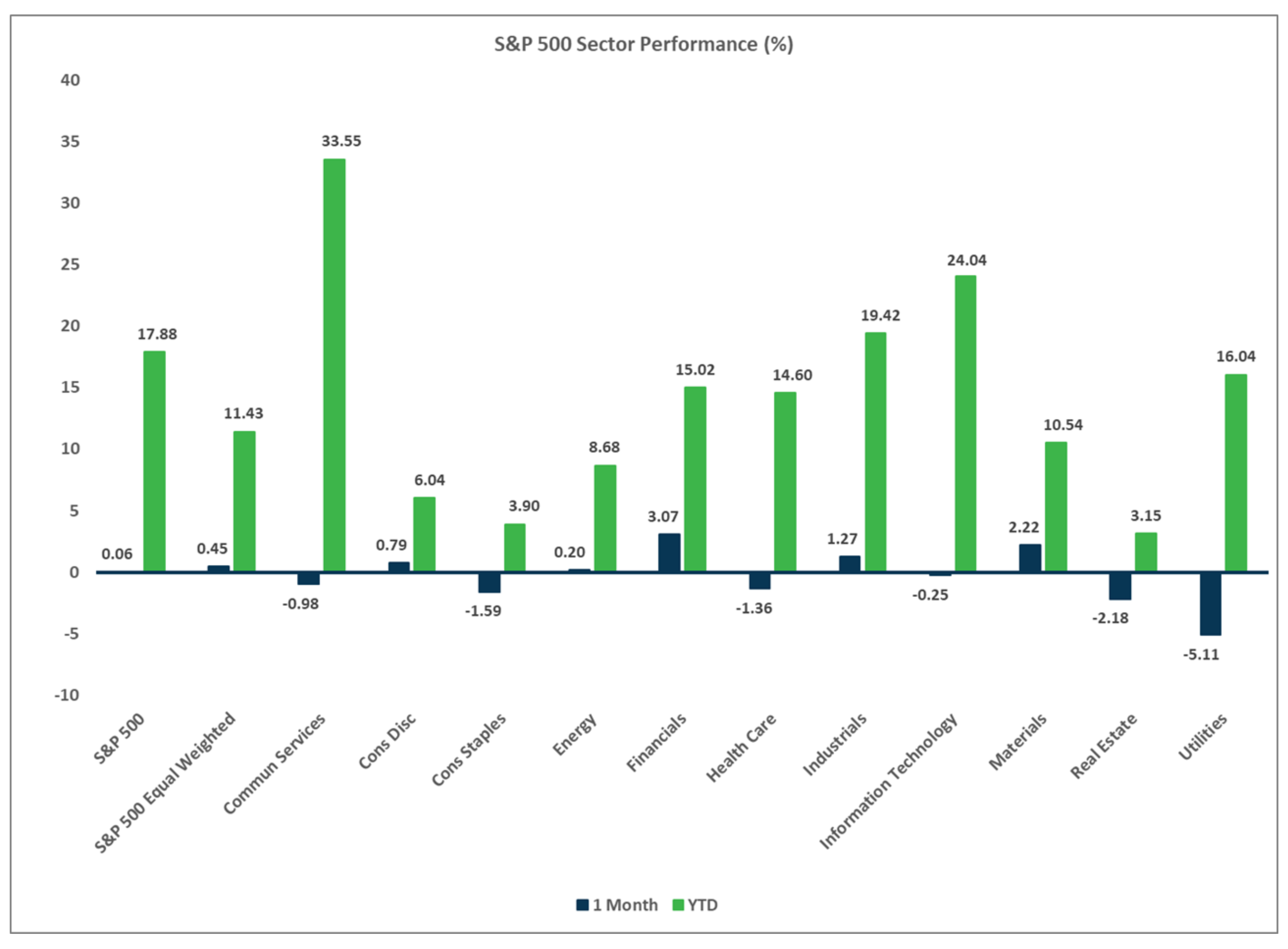

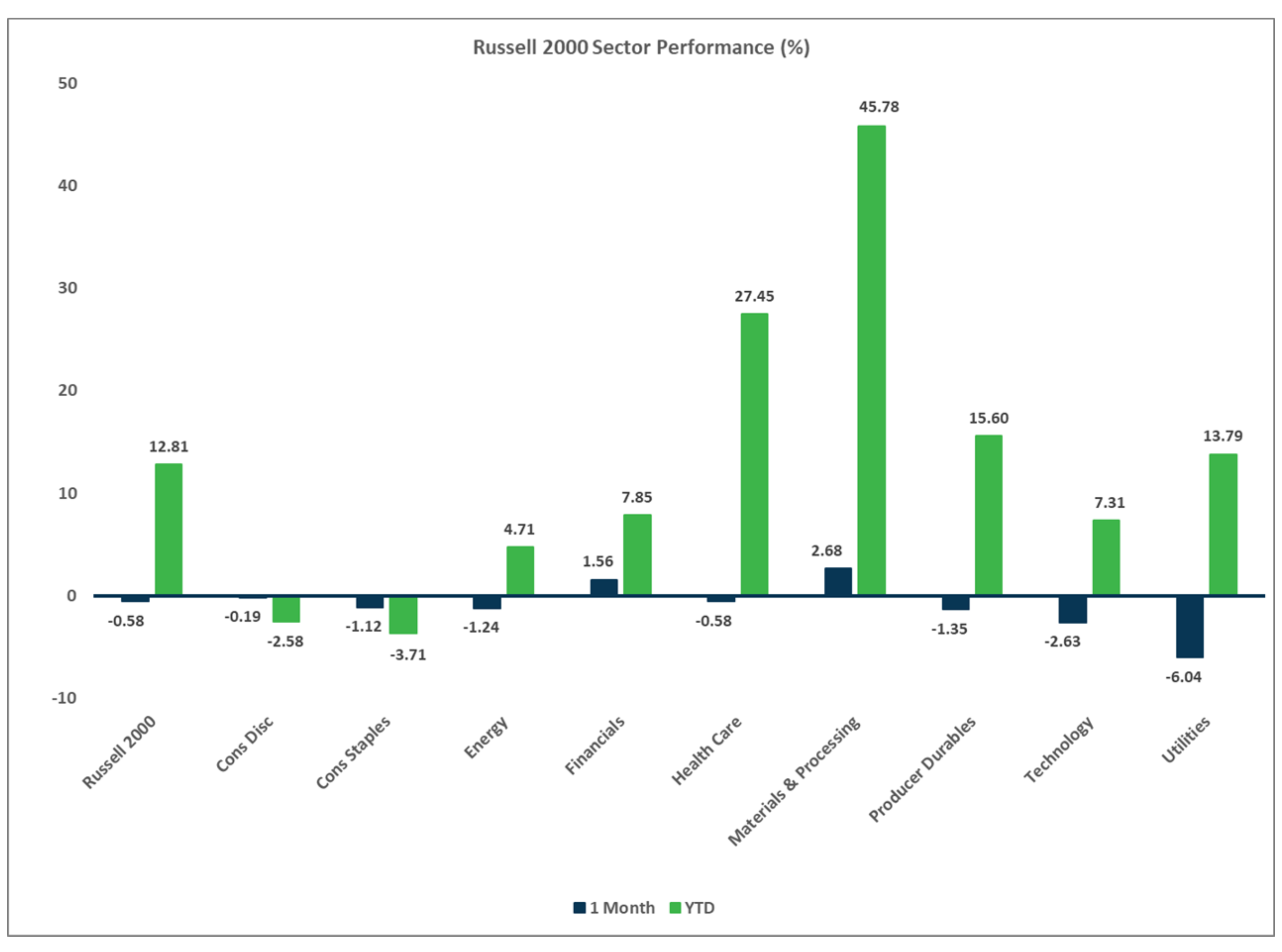

- U.S. equities were a mixed bag last month as large caps mostly gained ground while small caps fell in value.

- Value beat growth across all market capitalizations, and large caps outpaced small caps.

- The S&P 500 posted a gain of 17.9% in 2025 and the 10-year return now stands at a remarkable 14.8%.

Non-U.S. Equities

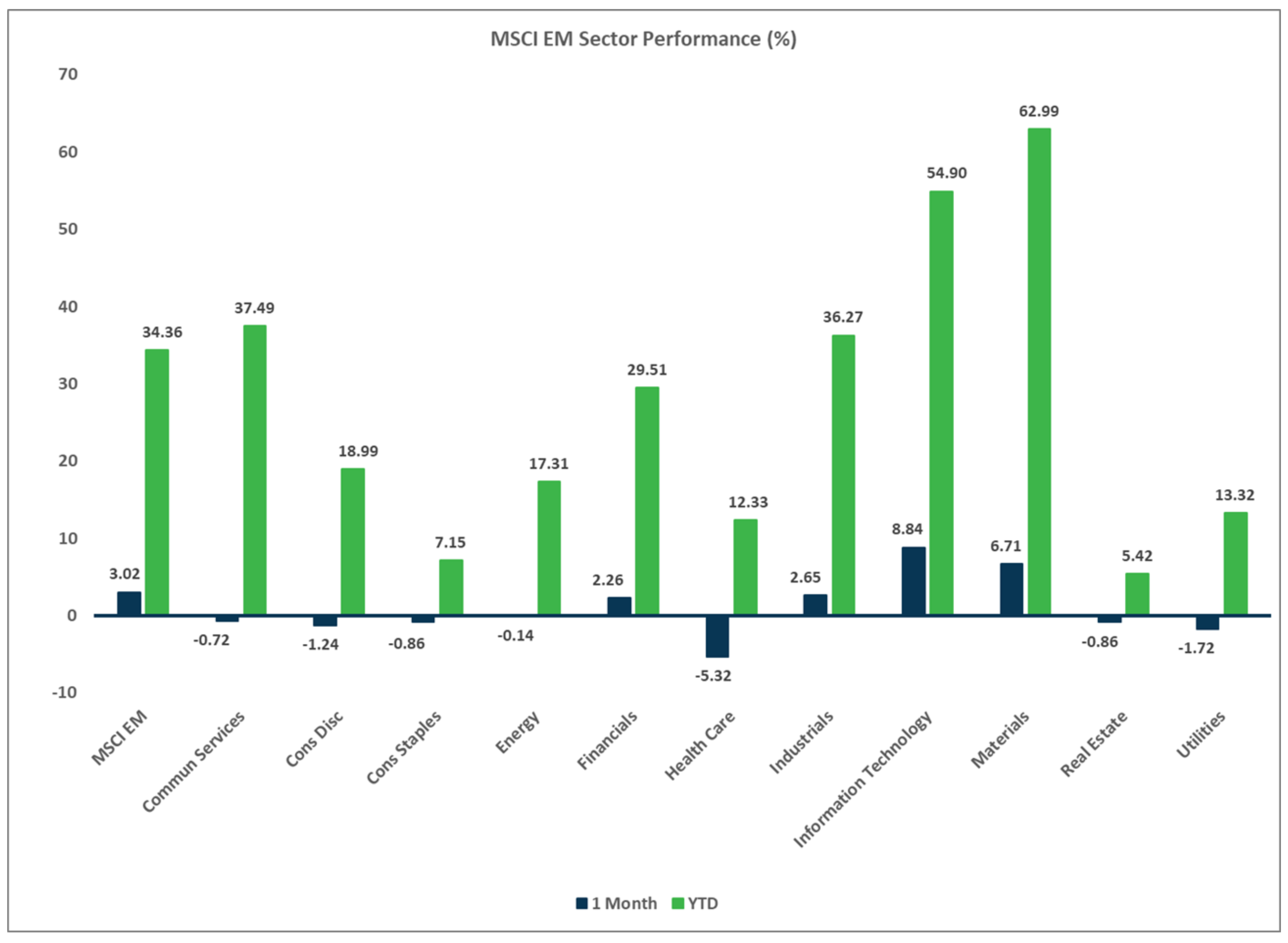

- Stocks outside the U.S. posted modest gains, with some outsized returns from EMs.

- Within EAFE markets, small caps lagged large caps and value stocks outpaced growth stocks. Value-driven Europe also outperformed Japan.

- Within EMs, most of the strength came from Eastern Europe and Asia excluding China.

- The weaker USD boosted EAFE returns by 92 bps in December and EM returns by 38 bps.

Sector Performance – S&P 500 (as of 12/31/25)

Sector Performance – Russell 2000 (as of 12/31/25)

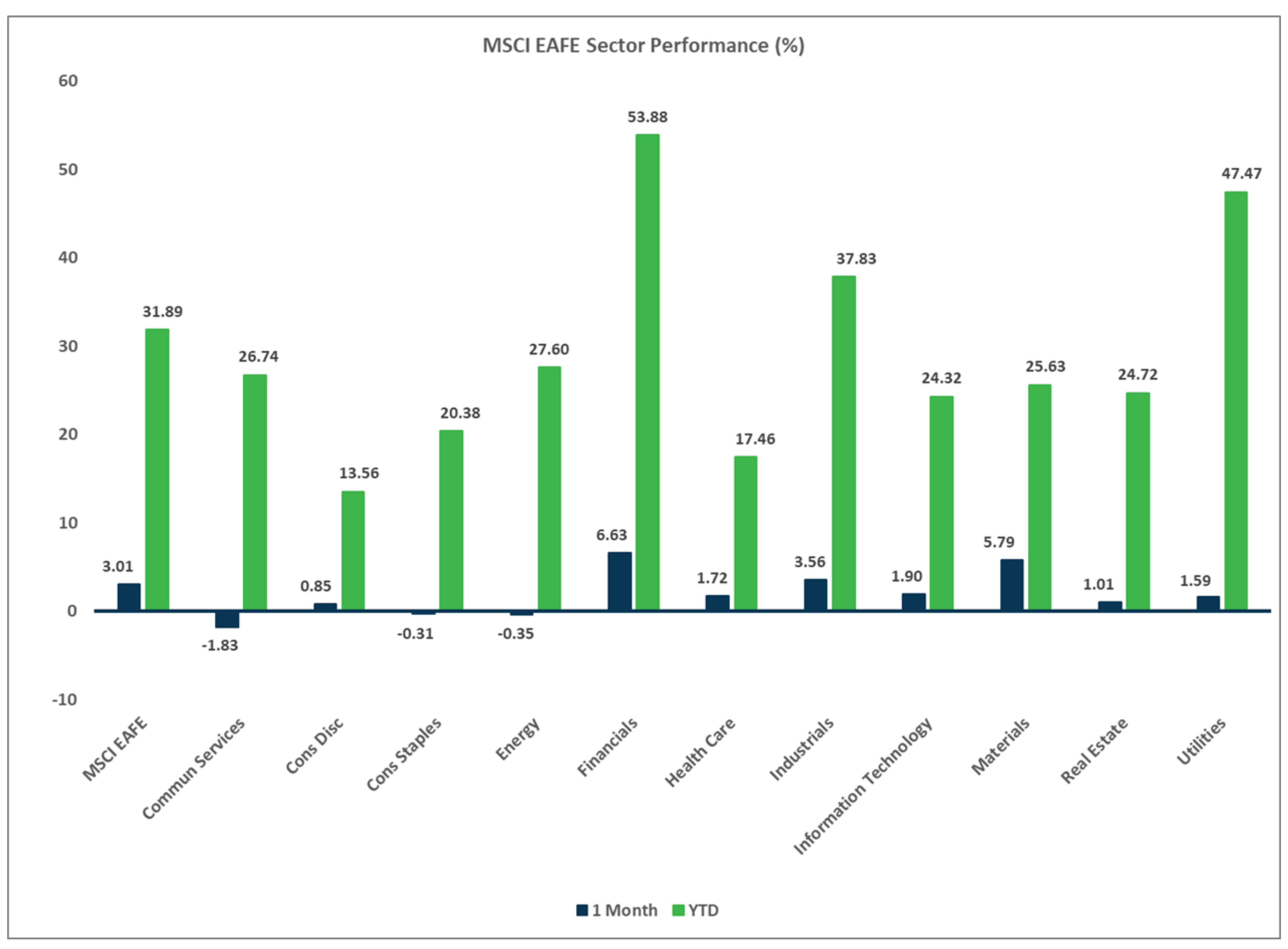

Sector Performance – MSCI EAFE (as of 12/31/25)

Sector Performance – MSCI EM (as of 12/31/25)