February 2026 Market Update

Economic Highlights

United States

- Fourth-quarter GDP came in below expectations based on the advanced reading. GDP rose at an annualized rate of just 1.4%, well below the estimate for a 2.5% gain. Consumer spending increased at a slower pace in Q4, while government spending tumbled sharply in a quarter marked by the record-length shutdown. The government shutdown was estimated to cost growth about 1% in Q4, although the exact impacts cannot easily be quantified. Consumer spending rose 2.4% in Q4, down from 3.5% in Q3. For the full year, the U.S. economy grew at a 2.2% pace, down from the 2.8% increase in 2024.

- The January jobs report showed a better-than-expected gain of 130,000 new jobs versus the 55,000 estimate. The unemployment rate edged lower to 4.3% while the broader U6 unemployment rate fell to 8%. Wages grew 0.4% M/M or 3.7% Y/Y. Healthcare and social assistance accounted for nearly all of the job gains in January. The Bureau of Labor Statistics also released final benchmark revisions for the period of April 2024 to March 2025. These numbers saw the initial counts revised lower by 898,000 on a seasonally adjusted basis.

- December’s CPI report came in better than anticipated, with headline inflation running at 2.7% and core inflation easing to 2.6%. Food prices jumped 0.7% M/M, energy prices rose 0.3% and recreation surged 1.2%. Rent increased 0.4%, but used cars fell 1.1%. With inflation largely contained, markets continue to project 2 to 3 rate cuts in 2026. In contrast, the PCE Index rose 3% in December, with core PCE increasing 2.9%. In December, goods inflation rose 0.4% M/M and services inflation increased 0.3%. Wholesale inflation also came in hotter than anticipated last month, perhaps a sign of tariffs working their way through the economy.

- The ISM Manufacturing PMI edged lower in February, with the headline reading falling to 52.4 (from 52.6 in January). New orders and production weakened in February while prices and employment strengthened. Survey respondents cited improving business activity overall, with building cost pressures.

Non-U.S. Developed

- The HCOB final manufacturing Purchasing Managers' Index rose to 50.8 in February from 49.5 in the previous month. Factory output increased in February, accompanied by a rise in new orders, but employment continued to weaken across the eurozone. Input costs also increased at the fastest clip in 38 months. Among big four economies, Germany returned to growth for the first time in over three-and-a-half years. The broader composite PMI for the region increased from 51.3 in January to 51.9 in February.

- Japan’s economy grew 0.1% in Q4 2025, narrowly missing a technical recession after GDP fell 0.7% in Q3. Private consumption drove the modest expansion, offsetting weakness in exports and public spending. The Bank of Japan in January raised its economic growth forecast for the fiscal year ending March 2026 to 0.9% from 0.7%. It also lifted its fiscal 2026 outlook to 1% from 0.7%. Japan’s inflation slowed sharply to 2.1% in December, its lowest level since March 2022. Still, prices have remained above the BOJ’s 2% target for 45 consecutive months.

Emerging Markets

- China’s economy is struggling with internal structural adjustments, including ongoing economic downside risks, a sharp decline in foreign investment, high youth unemployment, insufficient consumption momentum and a sluggish real-estate market. Massive government subsidies in China have led to industrial overcapacity, involution-style competition, and stagnant prices or even deflation. China’s economy is also facing increasingly high external risks, as its unfair competitive practices and overcapacity have triggered an ongoing tariff and technology war with the U.S.

- The Chinese economy continues to slow, with economists questioning the 5% growth rate reported last year.

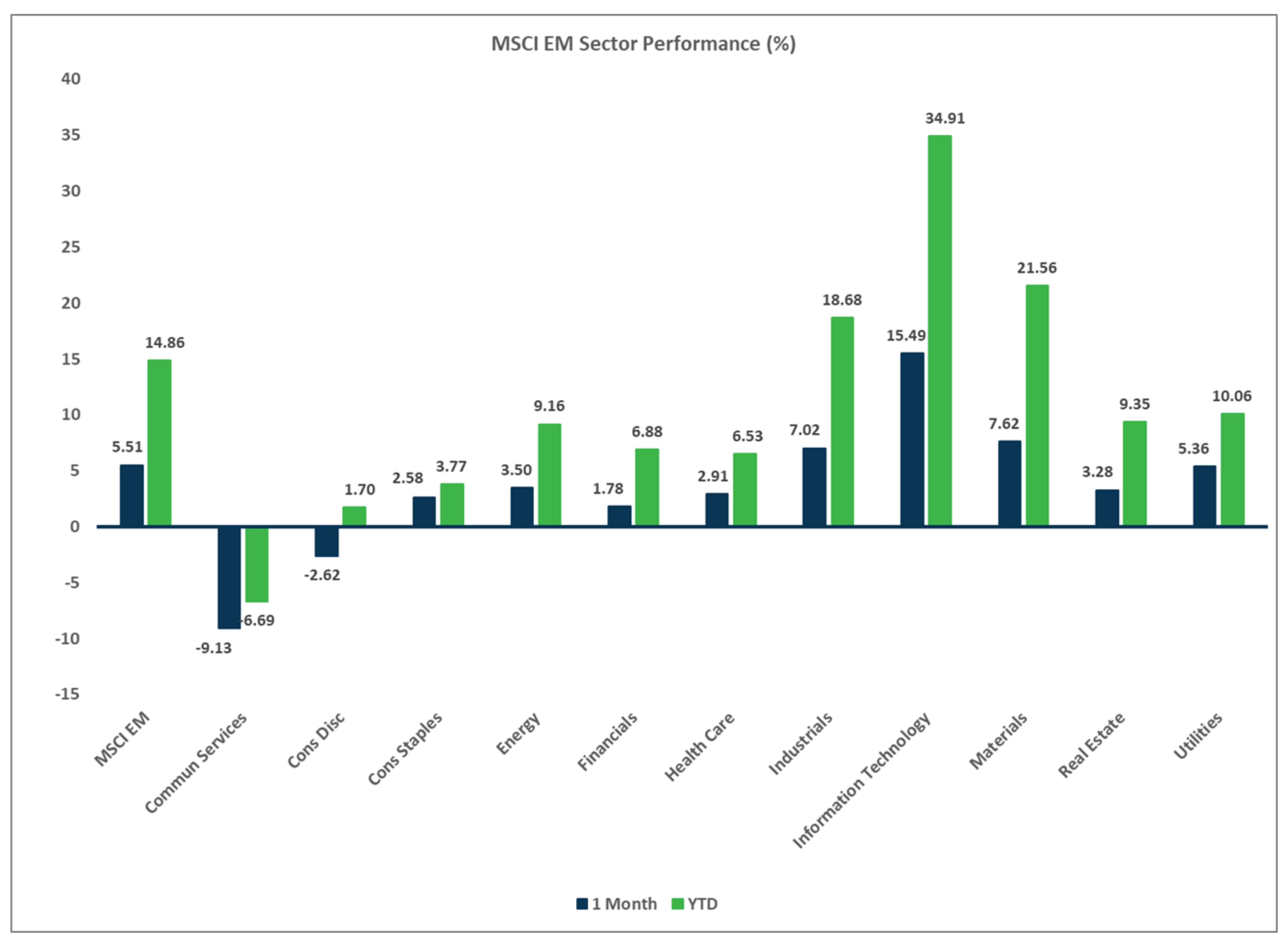

- Emerging markets have surged nearly 15% through the first two months of 2026, driven by broad-based gains across Latin America, Eastern Europe and Asia ex-China. This is largely an extension of strong gains that started in early 2025. We believe the backdrop for EMs remains favorable, with GDP growth that should far exceed most developed markets, cheap relative valuations, potential USD weakness, AI hardware (chips from TSMC) and tailwinds from commodities.

- After a decade dominated by U.S. exceptionalism, the current rally points to a potential broadening of global leadership — driven by currency dynamics, shifting capital flows and the geography of AI-driven production.

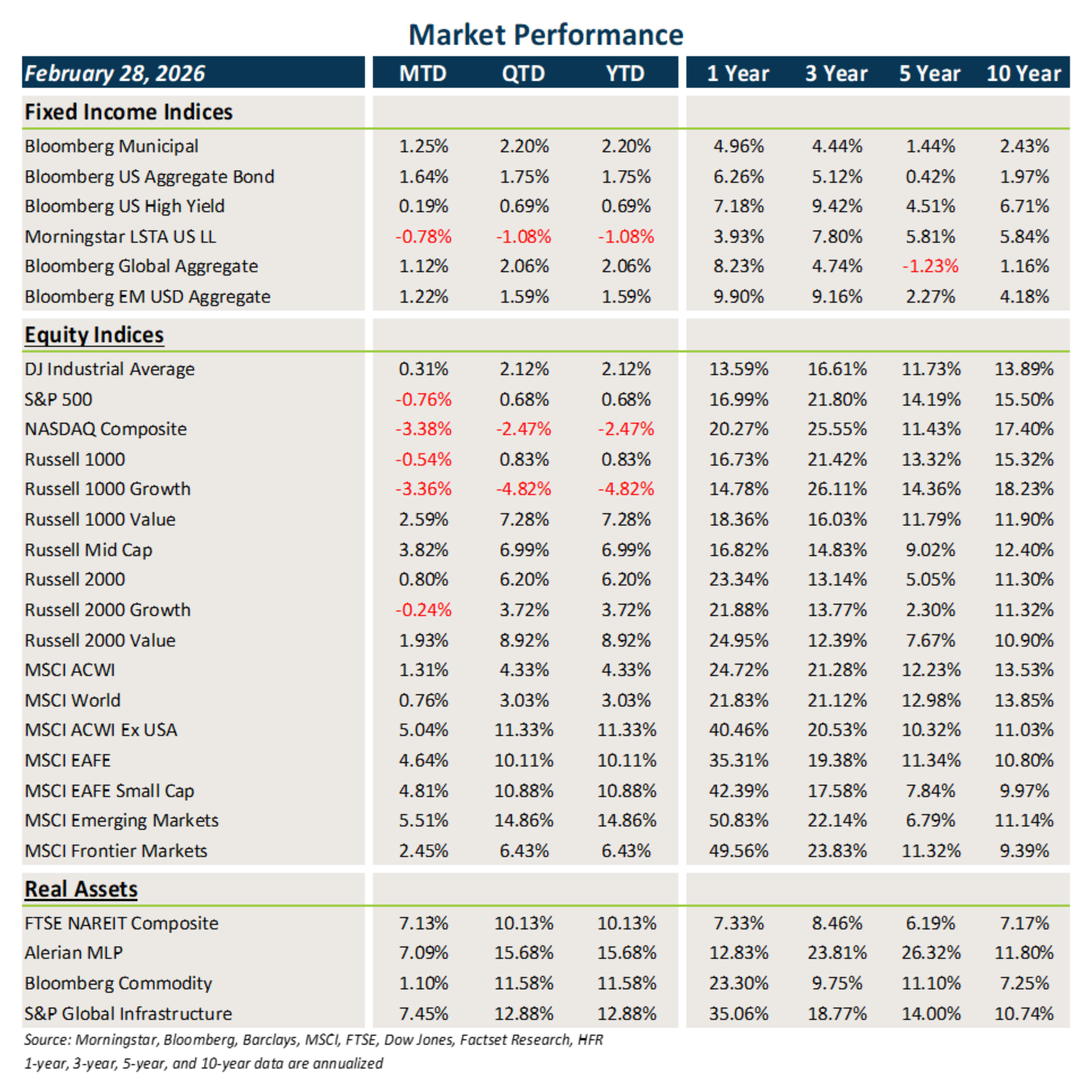

Market Performance (as of 2/28/26)

Fixed Income

- Fixed income across the globe posted strong gains in February, as rates declined and investors clipped coupons.

- The decline in interest rates was particularly good for core fixed income and municipal bonds.

- Credit continues to broadly display healthy fundamentals and near-historic tight spreads. Despite the noise, most of the weakness has occurred in the lowest quality issues.

U.S. Equities

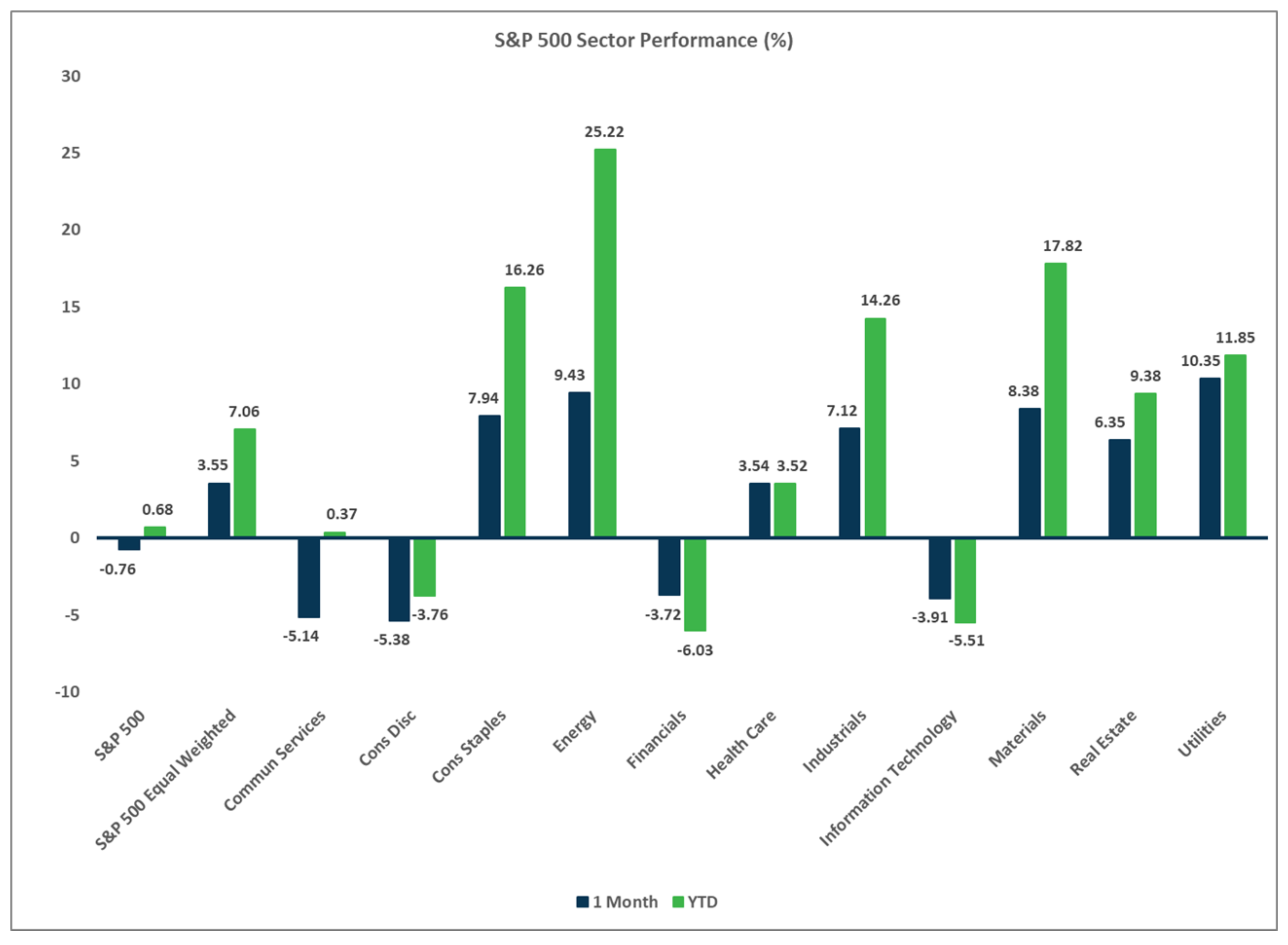

- U.S. equities struggled in February on the surface, largely due to weakness in the Mag 7 and other large cap tech.

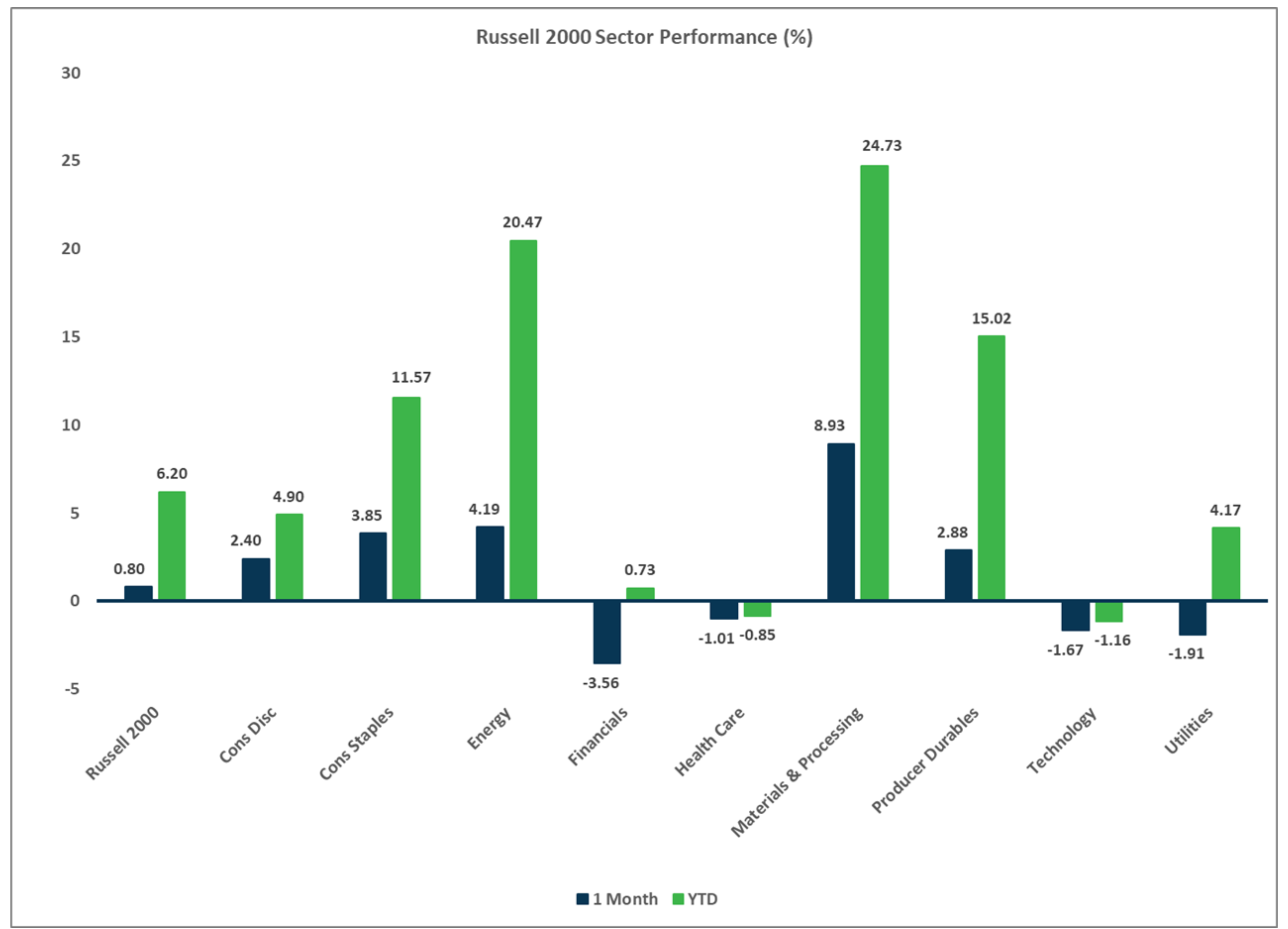

- Growth underperformed value across all market capitalizations, and small caps continue to lead large caps in 2026.

- The S&P 500 equal-weighted index leads the market-cap-weighted index YTD.

Non-U.S. Equities

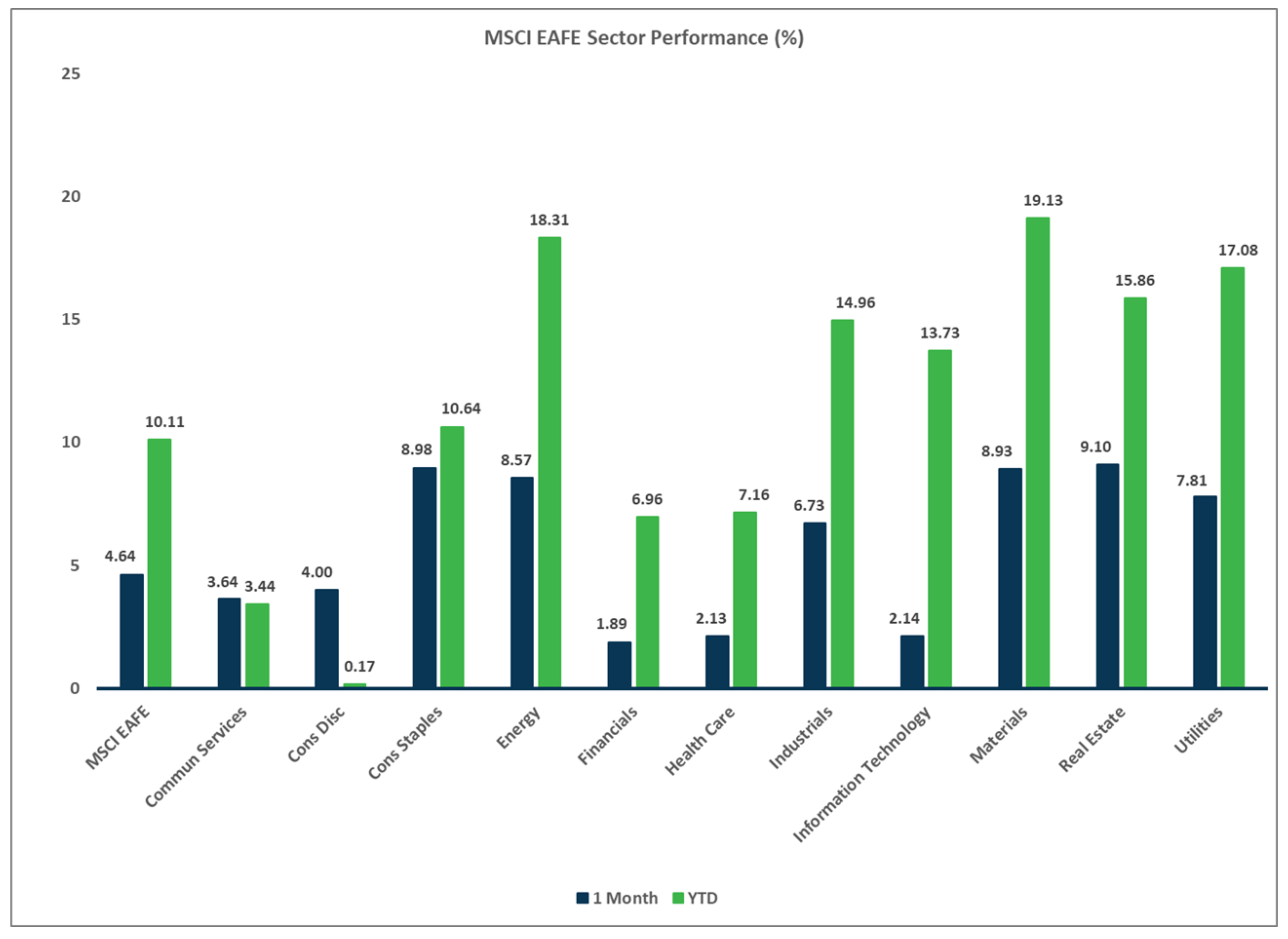

- Stocks outside the U.S. posted solid gains, driven by emerging markets, value stocks and small caps.

- EAFE markets outperformed U.S. equities, with the best gains coming from Japanese equities.

- EMs rose another 5.5% in February, with strong gains coming from Latin America and Asia ex-China. USD volatility hurt EAFE returns by 83 bps but boosted EM returns by 54 bps.

Sector Performance – S&P 500 (as of 2/28/26)

Sector Performance – Russell 2000 (as of 2/28/26)

Sector Performance – MSCI EAFE (as of 2/28/26)

Sector Performance – MSCI EM (as of 2/28/26)

Disclosures

Investment services offered by Enterprise Bank & Trust are not deposits, obligations, or guaranteed by the bank or its affiliates. The information provided represents the opinions of Enterprise Bank & Trust and is not intended to forecast future events or guarantee future results. Past performance does not guarantee future returns. This information is for educational purposes only. Investors should consult with their investment professionals for advice concerning their particular situation.

Investments are: *Not FDIC insured *May lose value *Not financial institution guaranteed *Not a deposit *Not insured by any federal government agency.