Market Flash Report | January 2021

Executive Summary

United States

- The U.S. closed out 2020 with 4% GDP growth in Q4. After collapsing in Q1 and Q2, the U.S. economy showed resilience with a decline of only 3.5% for the year. Q4 growth was led by consumer and business spending with some offset from weaker government spending.

- The manufacturing sector softened slightly in January with the ISM Manufacturing Index falling to 58.7 from 60.5 in December.

- The service sector remains in very solid territory based on the latest December reading of 57.2.

- Inflation remains fairly benign with the headline CPI reading sitting at 1.4% Y/Y. Core CPI was 1.6% Y/Y in December and Core PCE, the Fed’s preferred gauge of inflation, was 1.5%. Inflation expectations have risen sharply over the past few months, but outside of the base effect impacting the first half of 2021, we don’t expect meaningfully higher sustained inflation.

Non-U.S. Developed

- Eurozone GDP rose 12.5% Q/Q in Q3, but it is expected to decline 1% in Q4. The U.K. economy is forecast to fall 2% in the final quarter of 2020 after surging 16% in Q3.

- The latest Eurozone Composite PMI showed strength in manufacturing and significant weakness in services. The January headline number of 47.5 was down from 49.1 in December. Services in particular has been hard hit by renewed lockdowns and restrictions across the region.

- Japan’s economy grew 5.3% Q/Q in Q3 after contracting for the prior three quarters. GDP is forecast to grow under 1% in Q4 with slowdowns expected in consumer and business spending.

Emerging Markets

- The Chinese economy grew 6.5% in Q4 and 2.3% in 2020. The country did a great job overall containing COVID and over the second half of the year, retail sales and consumer spending strengthened.

- Economists expect China’s economy will grow over 10% in 2021. GDP is forecast to grow 12% in India, 3% in Brazil, 3.5% in Russia and 5% in South Korea.

- EM earnings are only projected to decline 6% in 2020 with several Asian countries expected to post positive growth. In 2021, the analyst community expects earnings growth of 35% with revenue growth of 12%.

- The EM growth story is intact and 2021 should see a strong rebound in terms of economic and corporate earnings growth.

Fixed Income

- Treasury/sovereign debt yields rose in January and credit spreads were mostly flat outside of riskier securities and floating rate loans.

- Recent USD weakness reversed course.

U.S. Equities

- After surging higher for most of January, U.S. equities finished the month on weak footing, led by the massive retail short squeeze and fund deleveraging.

- Small caps easily outperformed large caps for the month.

- LCG beat LCV by a small amount, but the opposite occurred within the small cap segment.

Non-U.S. Equities

- Non-U.S. developed equities showed similar weakness to end January. Europe in particular lagged Japan.

- Small caps beat large caps outside the U.S. and growth outperformed value.

- Emerging markets were the star performer, beating developed markets by almost 4%.

- The stronger USD detracted 69 bps from EAFE returns and 144 bps from EM returns.

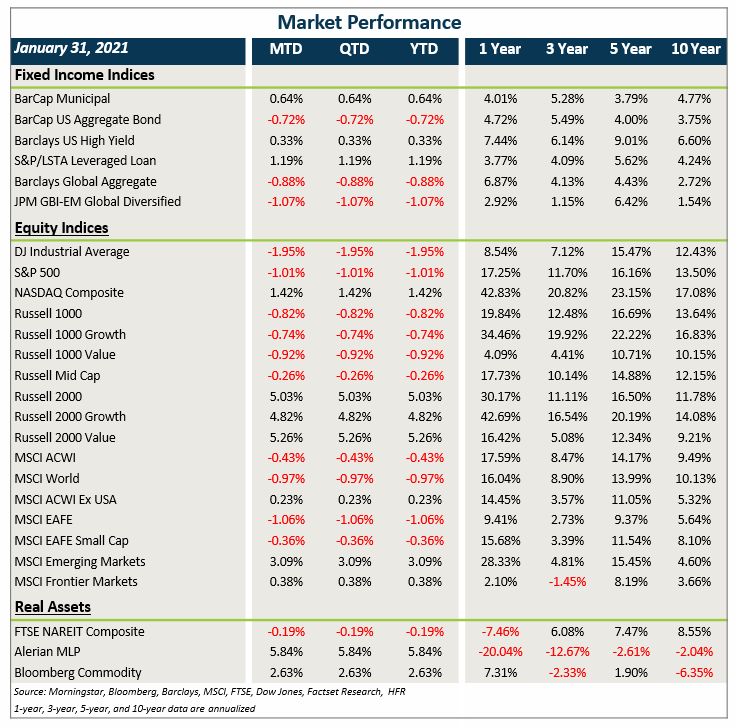

Market Performance (as of 1/31/21)

Sector Performance

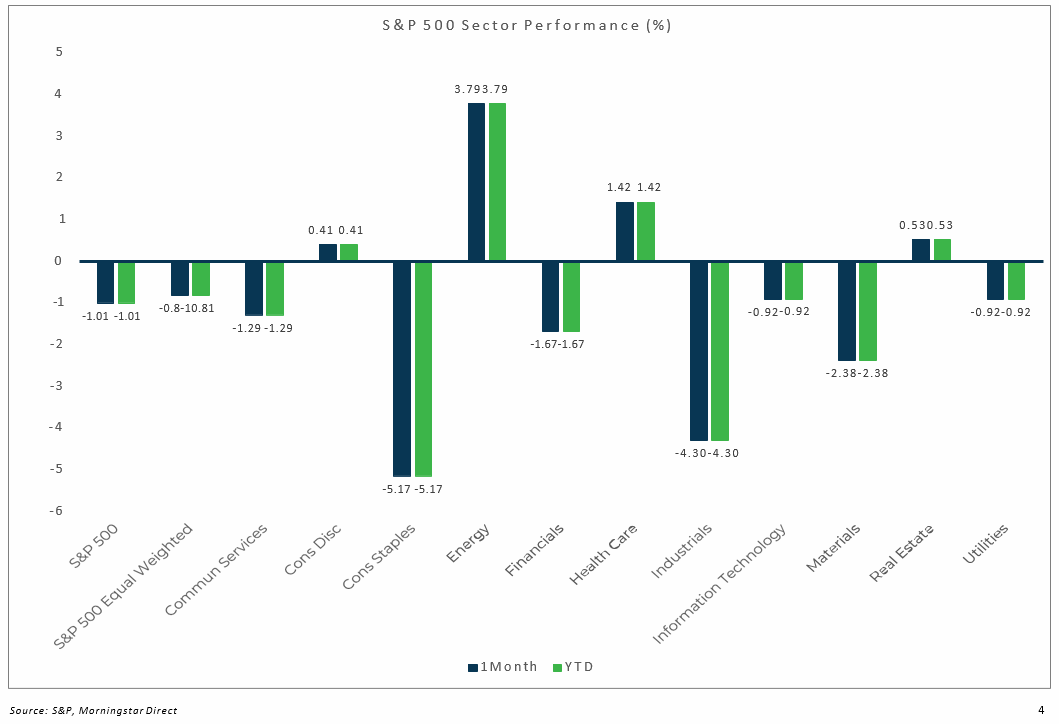

S&P 500 as of January 31, 2021

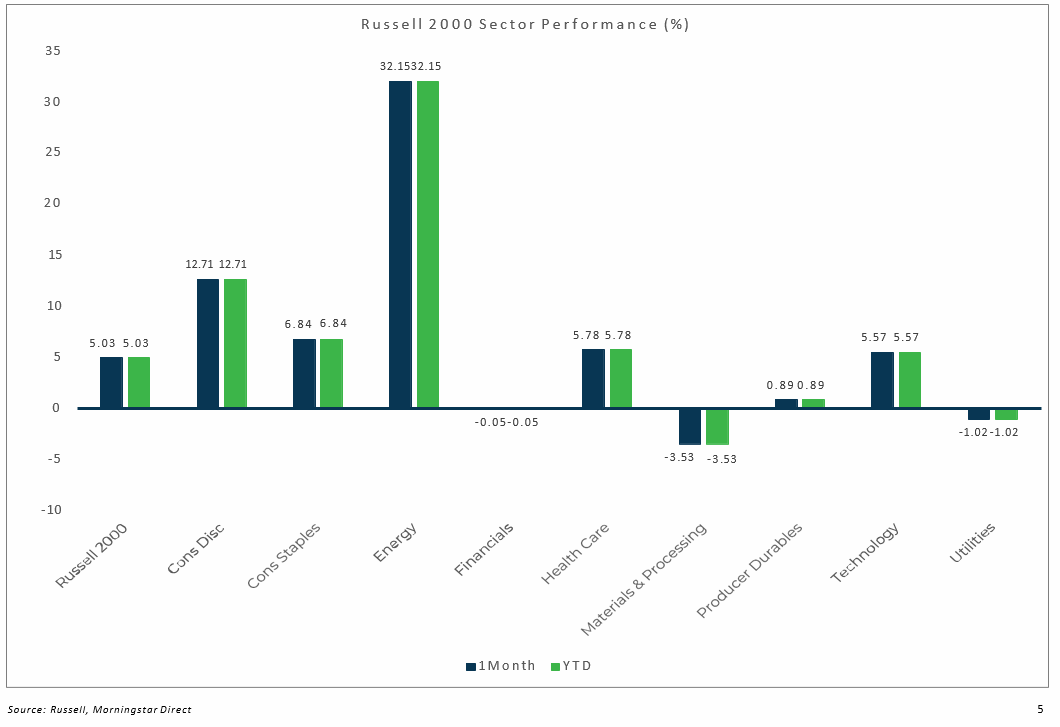

Russell 2000 as of January 31, 2021

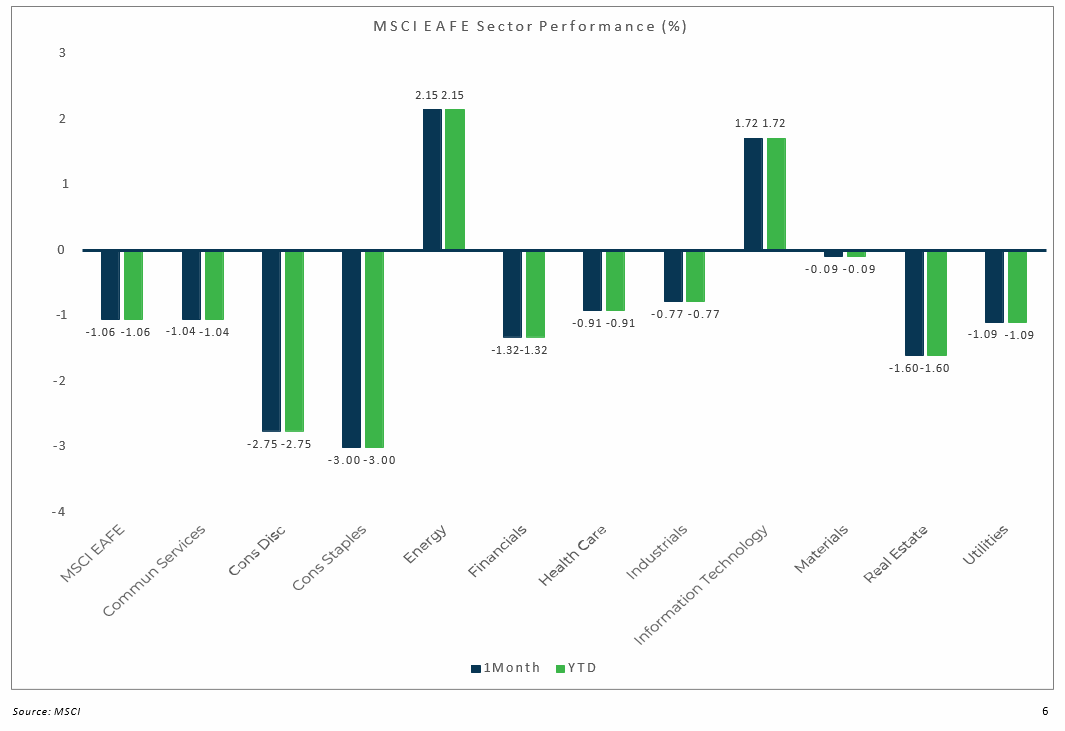

MSCI EAFE as of January 31, 2021

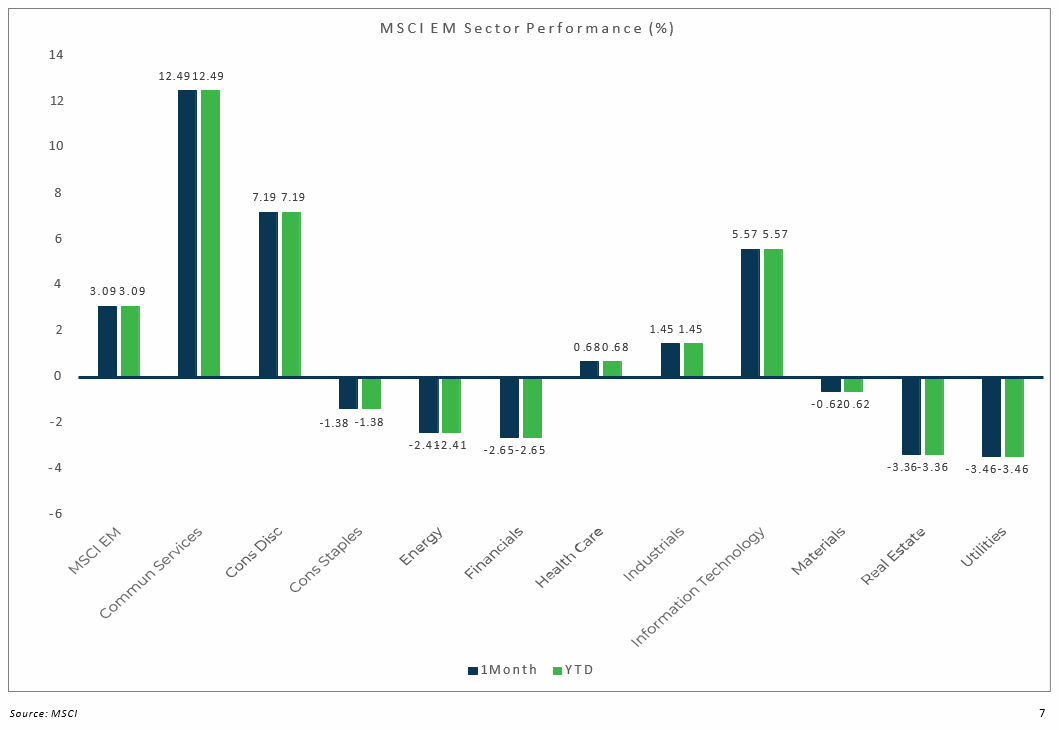

MSCI EM as of January 31, 2021