2021 Year in Review | Sponsor Finance

What a Year

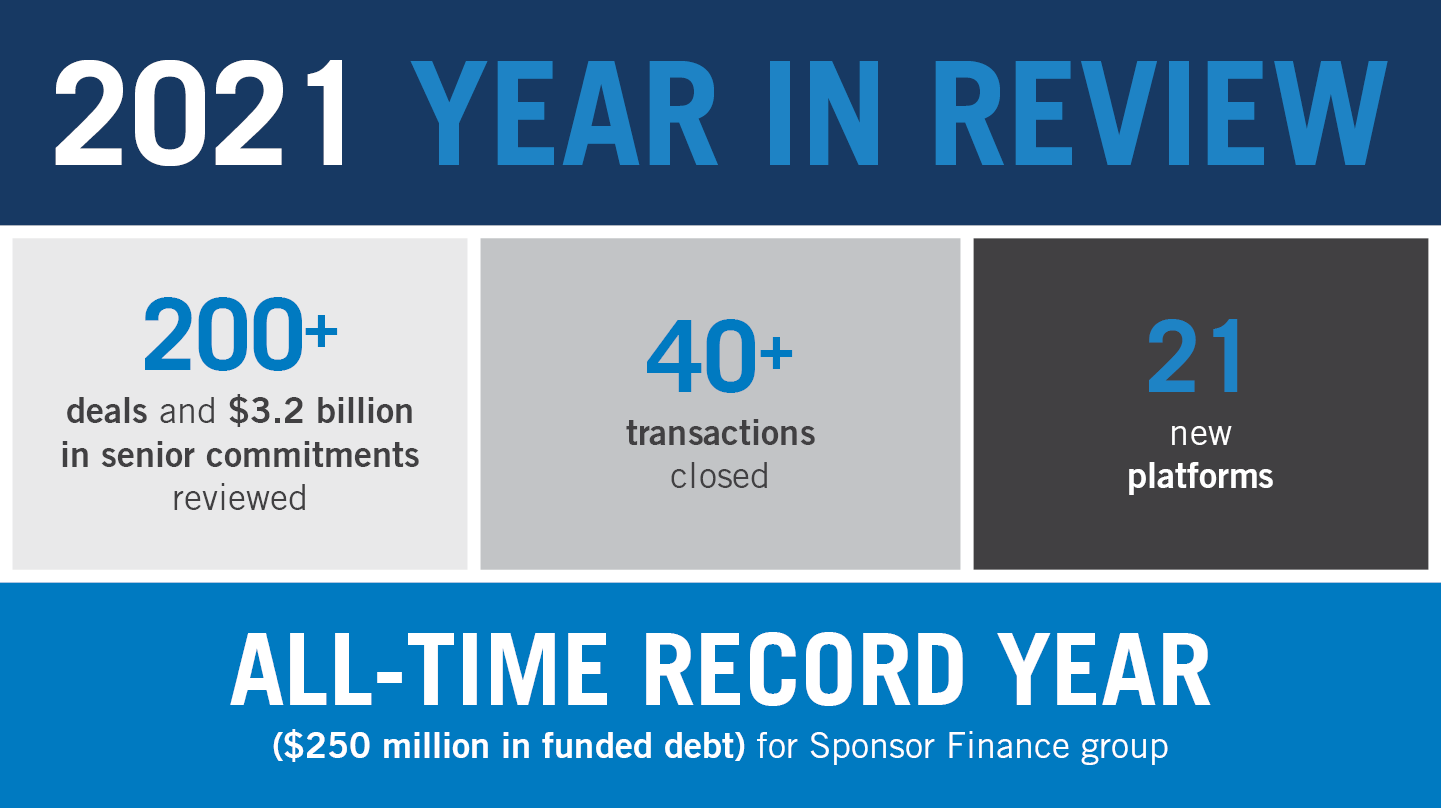

2021 was a wild ride, and we couldn’t be more excited as we finished up with an all-time record year in funded senior debt. As we begin a new year, we would be remiss if we didn’t pause and say THANK YOU to our friends and partners in the lower middle market space. We appreciate our relationships! Thank you for your collaboration and support, and we wish you a safe and happy 2022.

The Lower Middle Market and Sponsor Finance

Based on the deals we reviewed last year, our Sponsor Finance team compiled the following observations and insights for 2021:

- In the lower middle market (EV < $100MM), we saw average valuations increase to an all-time high of 7.6x (ranging from manufacturing and business services at the lower end of the spectrum, to distribution, health care and technology at the upper end).

- Coming out of 2020, we witnessed the re-assertion of the platform acquisition, with new platforms accounting for a material portion of the total deal mix.

- Based on ample liquidity in the credit markets, we saw average funded debt multiples increase across the board; senior leverage range of 2.5-3.25x at closing and total leverage range of 3.5-4.25x.

- We are seeing more deal flow from independent sponsor-sourced transactions, which typically involve transactions that are under LOI at discounted pricing.

- There continues to be a greater emphasis placed on sponsors’ cash equity contribution, with most deals requiring 50% equity capitalization, including at least 30% new cash equity exclusive of seller rollover.

Capital Markets Outlook for 2022

- After slowing in the third quarter of 2021, U.S. economic growth is expected to have accelerated in the fourth quarter. GDP estimates for the full year 2022 are in the 3-4% range, which is above-trend levels, but 2023 is likely to see a sharp deceleration.

- COVID-19 was relatively benign for most of Q4 until the omicron variant surge started to impact travel and other key industries late in the year.

- In reviewing the November employment report, sectors showing the biggest gains included professional and business services, transportation and warehousing, and construction.

- The biggest risk to equities and other risk assets is runaway inflation that leads to a more hawkish Federal Reserve, forcing it to tighten monetary policy more aggressively than expected. Thus far, the Fed will be ending its bond-buying program by March, with three rate hikes forecast in 2022. One potential wildcard is omicron, which could put a dent in economic growth. Any weakness could prompt the Fed to back off a bit to boost and support growth.

Read more about the themes to look out for in 2022 and more in our full Capital Markets Playbook for Q1*.

Recent Transactions

$26,800,000

|

$21,000,000

|

$13,500,000

|

$14,000,000

|

$15,500,000

|

$20,400,000

|

Start a Conversation

Fill out the form and a member of our dedicated team will reach out to you soon.